Are Medigap Insurance Policies Actually Worth It?

-

Last Updated July 20, 2026

Ask ten Medicare agents whether a Medigap plan is worth the money and you will get ten different answers. That is not a figure of speech. Across thousands of responses from licensed professionals, a genuine split has emerged, and the lines are not where most people expect them to be.

The argument is not really about whether Medigap works. Everyone agrees it works. The argument is about whether the math holds up over a 20- or 30-year retirement, and whether the peace of mind is worth the price tag when that price tag keeps climbing.

Is Medigap worth it? Key points at a glance

- Medigap offers predictability. Pay a monthly premium plus the $283 Part B deductible, and the rest of your covered care is paid for.

- Premiums climb with age. A $150/month Plan G at 65 often becomes $350–$500/month by your late 70s.

- The "crossover age" is real. Somewhere between 70 and 80, annual Medigap costs can exceed the worst-case out-of-pocket max on Medicare Advantage.

- The guaranteed issue window at 65 matters. Skip Medigap now, and health conditions later may lock you out of it entirely.

Side A: Medigap Is Worth Every Penny

A large group of agents will tell you, without hesitation, that Medigap remains the gold standard of Medicare coverage. Their reasoning tends to center on three pillars: cost predictability, provider freedom, and protection from catastrophic bills.

With a Plan G, you pay your monthly premium, cover the annual Part B deductible ($283 in 2026), and that is it. No copays at the doctor. No coinsurance after surgery. No surprise bills after a hospital stay. Agents who favor Medigap frequently describe it as "pay upfront, pay less later" coverage. You know exactly what your medical budget will be for the entire year.

The provider access argument is just as strong. Medigap works with Original Medicare, which means any doctor or hospital in the country that accepts Medicare will see you. This is one of the core reasons agents recommend working with a Medicare Supplement specialist who can walk you through the full picture. No networks, no referrals, no prior authorizations. For people who travel, split time between states, or simply want the freedom to choose their own specialists, this flexibility is a major selling point. Several agents pointed out that top facilities like Mayo Clinic, Cleveland Clinic, and Johns Hopkins accept Original Medicare but may not participate in Medicare Advantage networks.

My neighbor says I'm crazy for paying for a Medigap plan when Medicare Advantage is "free." What should I tell him?

You can tell your neighbor that while Medicare Advantage plans may have low or zero premiums, they are not truly free. They often come with copays, deductibles, and network restrictions that can add up over time, especially if you get sick or need specialized care. A Medigap plan may cost more upfront, but it gives you the freedom to see any doctor nationwide who accepts Medicare, fewer out-of-pocket expenses, and more predictable costs overall. It's not about paying more—it's about having better coverage, fewer surprises, and peace of mind.There is also the protection argument. Without a Medigap plan, Original Medicare leaves you responsible for 20% of Part B costs with no annual out-of-pocket maximum. A serious illness, multiple surgeries, or an extended hospital stay could mean tens of thousands of dollars in bills. Medigap eliminates that exposure almost entirely.

One agent framed it bluntly: Medigap is insurance on your insurance. You are paying a known monthly amount to make sure you never face an unknown financial catastrophe.

Side B: The Premium Math Stops Working

Not every agent agrees that Medigap is the clear winner, and the dissent is more substantive than you might expect. The core argument from the skeptics centers on how the real costs of each approach compare over time.

Medigap premiums increase every year, sometimes twice a year. Agents report seeing clients who started at $125 per month eventually paying $400, $500, or even $600 per month as they aged into their late 70s and 80s. Add a standalone Part D prescription drug plan ($25 to $110 per month) and separate dental and vision coverage, and the total monthly outlay for the Medigap route can reach $500 to $700 or more.

Compare that to a Medicare Advantage plan with a $0 monthly premium that includes prescription drug coverage, dental, vision, hearing, and a gym membership. Even if you hit the worst-case scenario and max out your annual out-of-pocket limit ($5,000 to $9,250 depending on the plan), some agents argue the math favors Advantage once premiums climb past a certain threshold.

Is paying for a high-end Medicare Supplement plan really worth it, or is it overkill?

Medicare supplemental plans might become significantly more expensive as you age, especially with an insurance carrier categorizing you into age brackets instead of community or state groupings.As for whether having additional coverage is overkill, it's likely to depend on the type of care you envision needing in the future. Medicare Advantage plans are tied to specific PPO and HMO networks and ZIP codes, which may limit the services available to you unless you secure prior approval. This means your experiences will largely hinge on the community you live in, your zip code, the doctors in your network, not to mention any travel plans you may have. The insurance company controls these types of plans, and Medicare controls Medicare supplement plans.

I currently have a Medicare supplemental plan, but I foresee that I might need to transition to a Medicare Advantage plan as I age and become less active. The beautiful thing is that you can always go to a Medicare Advantage plan anytime, but you must pass underwriting conditions to qualify to go back to a Medicare supplement plan later.

One agent in a high-cost area was direct about this: once someone hits their mid-70s, annual Medigap premiums in his region exceed the maximum out-of-pocket on a Medicare Advantage plan. At that point, you are paying more in premiums for Medigap than you would ever spend, even in a bad health year, on an Advantage plan.

Another agent, who personally started on a Medigap Plan G at 65, switched to Medicare Advantage by age 68 because his supplement premium had already crossed $215 per month plus $52 for a Part D plan. He said the switch saved him thousands.

The counterargument from this camp is not that Medigap is bad coverage. It is that the true cost structure of both options looks very different at 75 than it does at 65.

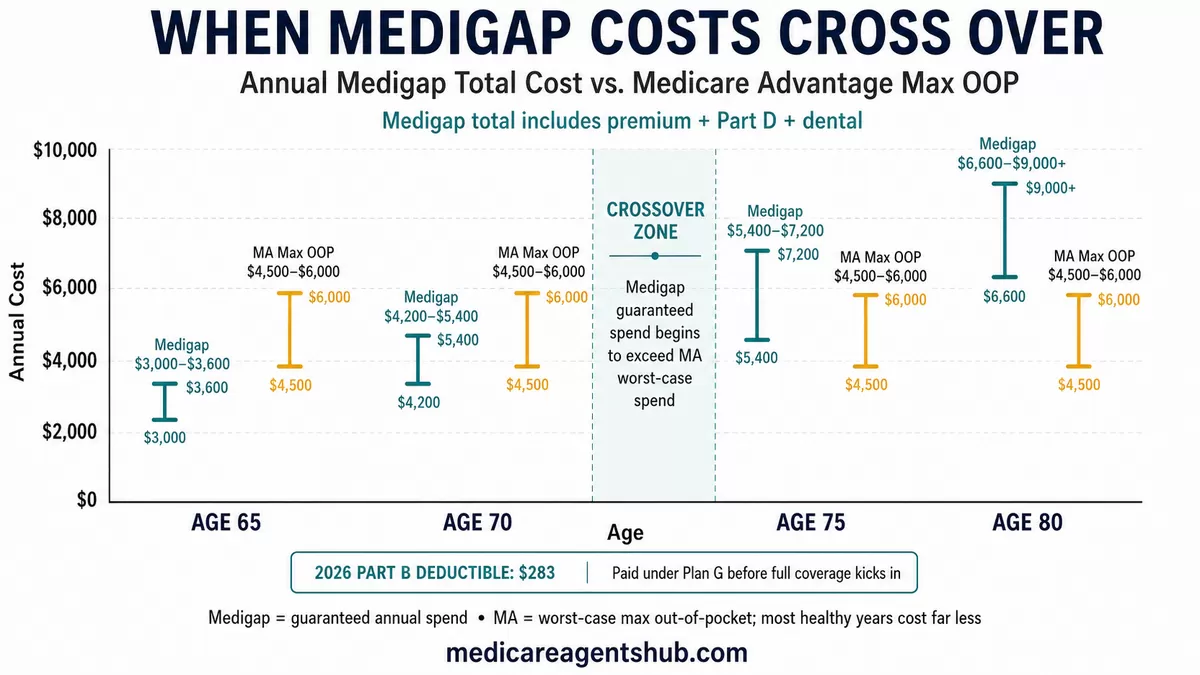

The Crossover Age: When the Numbers Flip

This is where the debate gets specific and where agents disagree the most. Multiple agents referenced a "crossover point" where annual Medigap premiums surpass the maximum out-of-pocket on competitive Medicare Advantage plans in the same area.

Here is a simplified illustration of how the math can shift:

| Age | Est. Annual Medigap Cost (Premium + Part D + Dental) | MA Max Out-of-Pocket (Typical Plan) |

|---|---|---|

| 65 | $3,000 - $3,600 | $4,500 - $6,000 |

| 70 | $4,200 - $5,400 | $4,500 - $6,000 |

| 75 | $5,400 - $7,200 | $4,500 - $6,000 |

| 80 | $6,600 - $9,000+ | $4,500 - $6,000 |

Note: These ranges are illustrative based on agent-reported figures. Actual costs vary significantly by state, county, carrier, and health status. The MA column represents the worst-case annual spending, while the Medigap column represents guaranteed annual spending regardless of health.

At 65, Medigap is often cheaper than a bad health year on Medicare Advantage. By 75 or 80, the premium alone can exceed what you would spend even in the worst year on an Advantage plan. That is the crossover, and it is the reason some agents stop recommending Medigap to older clients.

But here is the catch the pro-Medigap agents are quick to point out: that table only tells half the story. The MA column shows the maximum you could spend. Most healthy years on Advantage, you spend far less. But the Medigap column shows what you will spend, every single year, healthy or not. Predictability versus probability.

Side C: It Depends on When You Get In

The third camp is arguably the most nuanced, and many experienced agents land here. Their position: Medigap is the right choice when you are healthy enough to get it and young enough to lock in reasonable rates. But you need to go in with your eyes open about what happens in 15 years.

This matters because of underwriting. When you first become eligible for Medicare at 65, you have a guaranteed issue period where any Medigap insurer must accept you regardless of health conditions, at their standard rate. Miss that window, and you may need to answer health questions. Develop a serious condition along the way, and you could be denied or charged significantly more.

If Medicare Supplement (Medigap) plans are better for long-term coverage, why don't more people choose them?

In short, money. We are paid commission and the commission on an Medicare Advantage plan is double that of a Supplement.Several agents described a pattern they see repeatedly: someone skips Medigap at 65 because they feel healthy and do not want to pay the premium. By 72 or 75, health conditions have developed, and now they cannot qualify for a supplement even if they want one. They are locked into the trade-offs that come with Medicare Advantage whether they like it or not.

The advice from this camp is practical: if you can afford it at 65, get Medigap while you can. Lock in your access. Then reassess every few years. You can always switch from Medigap to Medicare Advantage with no health questions, but going the other direction requires underwriting in most states. The door only swings one way easily.

One agent put it this way: getting Medigap when you are healthy is smart. Keeping Medigap when you are sick is essential. The gray middle, where you are healthy enough to switch but the premiums are eating into your retirement budget, is where regret lives.

Plan G's $283 Deductible: The Predictability Premium

Plan G is the most popular Medigap plan sold today, and understanding why tells you a lot about what people are actually buying. With Plan G, after you pay the $283 annual Part B deductible, everything else is covered. Every doctor visit, every specialist, every hospital stay, every outpatient procedure. Your total predictable medical cost for the year is your monthly premium times twelve, plus $283.

Compare that to a $0-premium Medicare Advantage plan where a primary care visit might be $0, but a specialist could be $40, an MRI could be $250, and a three-day hospital stay could run $1,000 or more in copays. Most healthy people on MA spend very little out of pocket in a given year. But one bad year, one cancer diagnosis, one hip replacement, and you could be looking at $5,000 to $8,000 in costs.

Agents who recommend Plan G frequently say their clients are not paying for coverage. They are paying for certainty. The $283 deductible is a small price for knowing exactly what your healthcare will cost, no matter what happens. That certainty has real psychological value for retirees on fixed incomes who cannot absorb a $7,000 surprise.

Which is better: a Medicare Advantage Plan or a Medigap policy?

It all depends on your particular scenario. When I started specializing on Medicare plans, I worked for an insurance company writing Medicare Supplements only and ran into people with Medicare Advantage plans and paying no premium. With a Medicare Supplement, you have to pay that premium and then take out a Prescription Drug plan and pay for it, you have no maximum out of pocket and don't have dental, vision and hearing benefits along with a free gym membership and other benefits, and premiums keep going up and up as you age. I quit writing for that carrier, and I've been writing Medicare Advantage plans, and I've been on Medicare Advantage plans for over 12 years myself paying no premium or low premium with prescription drug coverage imbedded and am way ahead money and benefit wise and have gone through breast cancer and many other health problems and a lot of dental work. I highly recommend Medicare Advantage plans.But agents in the other camp counter that certainty comes at an escalating price. A 65-year-old paying $150 per month for Plan G is paying $1,800 a year for that certainty. A 78-year-old paying $350 per month is paying $4,200. At some point, the premium for certainty exceeds the uncertainty itself.

What Agents Agree On

Despite the disagreement on value, there are several points where nearly every agent converges:

- Medicare Advantage is not "free." A $0 premium does not mean $0 cost. Copays, coinsurance, and annual out-of-pocket maximums mean you are still paying for healthcare, just in a different structure.

- No plan is right for everyone. Health status, budget, location, travel habits, and risk tolerance all factor into the decision. Anyone who tells you one type is always better is not giving you the full picture.

- The guaranteed issue window at 65 matters enormously. Whatever you decide, understanding which Medigap plan offers the best value during your initial enrollment is critical, because that is when you have the most options and the lowest rates.

- Medigap premiums will increase. This is not a possibility. It is a certainty. Plan for it.

- Switching from Medigap to MA is easy. Switching back is not. If you drop your Medigap plan and later want to return, you will face medical underwriting in most states. Some states have birthday rule or annual open enrollment protections, but most do not.

Making Your Own Decision

The reason agents disagree about Medigap is the same reason it is a genuinely hard decision: the right answer depends on variables nobody can fully predict. Your future health, how fast premiums rise, whether your Advantage plan changes networks, whether the long-term savings from Medicare Advantage materialize or evaporate in a bad health year.

What you can control is the process. Work with a licensed, independent broker who sells both Medigap and Medicare Advantage plans. You can find a licensed Medicare agent near you to get personalized quotes.

If you're leaning toward Medigap, comparing which carriers brokers actually recommend is a smart next step. Pricing, rate stability, and claims handling vary more than most people realize. Ask them to run the numbers for your specific situation. Look at what your total annual cost would be under each option, not just the monthly premium. Factor in prescription drugs, dental, and vision. And think about what happens not just this year, but five and ten years from now.

The agents who answered these questions are not trying to sell you on one option. They are trying to make sure you understand what you are choosing and what you are giving up. That is the kind of guidance that matters, especially for a decision you will live with for the rest of your retirement.