Why Medicare Supplement Rates Increase and How Beneficiaries Can Reduce Costs

Medicare Supplement (Medigap) premiums are increasing across the country, and many beneficiaries, especially in states like Florida, are seeing noticeable jumps in their monthly costs.

If your Medicare Supplement premium has gone up recently, you're not alone. The key is understanding why rates increase and what options are available to help reduce those costs.

Why Medicare Supplement Rates Are Increasing

Medicare Supplement plans help cover out-of-pocket costs left by Original Medicare, including deductibles, coinsurance, and excess charges. Over time, several factors contribute to rising premiums:

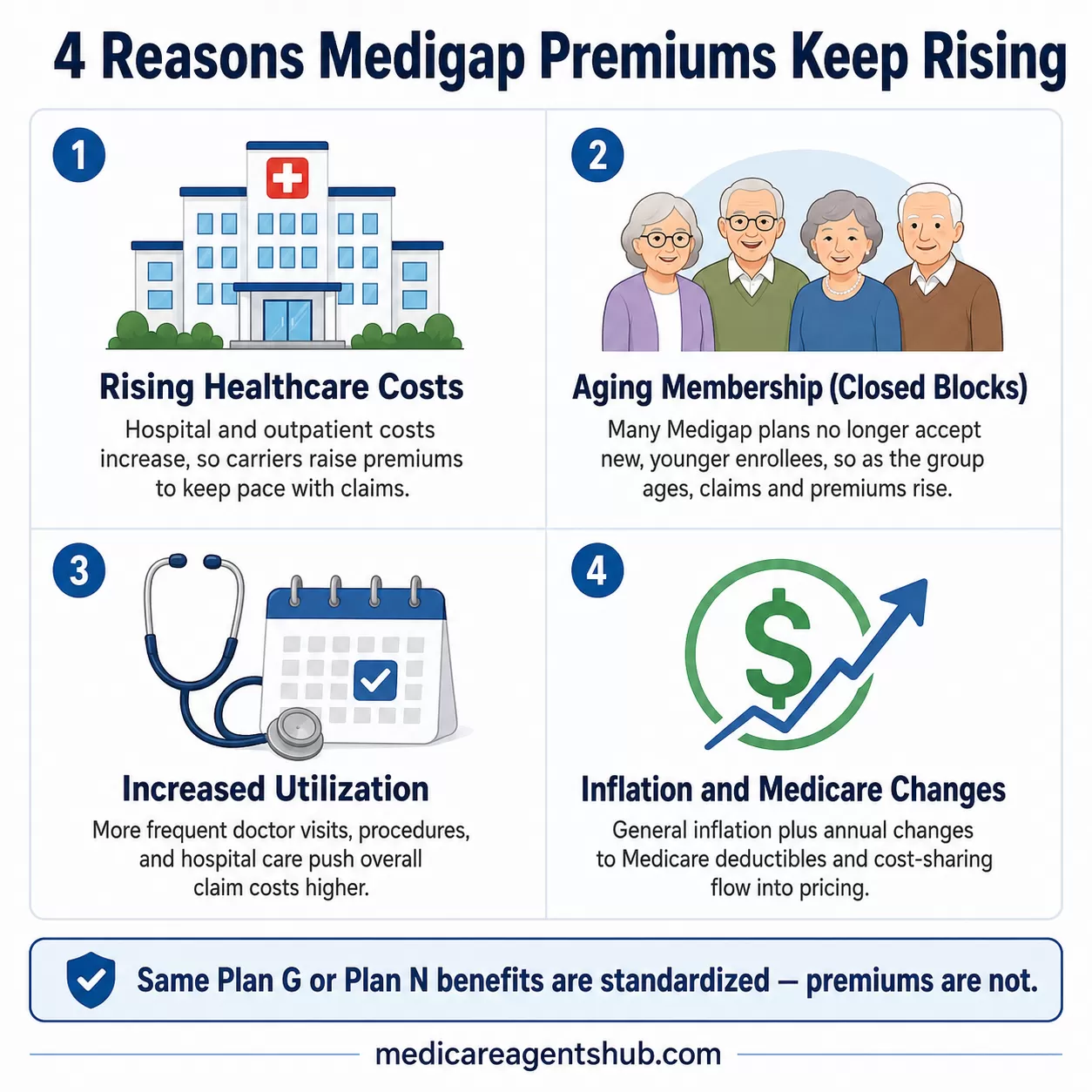

Rising Healthcare Costs

As hospital and outpatient costs increase, insurance carriers adjust premiums to keep pace with claims.

Aging Membership (Closed Blocks)

Many Medigap plans are part of "closed blocks," meaning no younger, healthier enrollees are entering the plan. As the group ages, claims increase, which drives up premiums.

Increased Utilization

More frequent use of medical services, including doctor visits, procedures, and hospital care, leads to higher overall claim costs.

Inflation and Medicare Changes

General inflation and annual changes in Medicare deductibles and cost-sharing also impact pricing. For a closer look at where your Medicare dollars go, see our breakdown of what determines your Medicare costs and how to reduce them.

Why Reviewing Your Plan Matters

One of the most common misconceptions is that staying with the same Medicare Supplement plan is the safest or most cost-effective choice.

In reality, beneficiaries often find that:

- The same plan type (such as Plan G or Plan N) may be available at a lower premium with another carrier

- Newer plans may be priced more competitively

- Long-held plans can become more expensive over time due to rate increases

Taking time each year to review your Medicare plan is one of the simplest ways to stay ahead of unnecessary costs.

I went with Medigap because I travel a lot, but now I'm paying a fortune in premiums. Did I make a mistake?

Not necessarily—you made the best decision you could with the information you had at the time.Medigap is still one of the best options for people who travel a lot. It gives you the freedom to see doctors pretty much anywhere without worrying about networks, and that’s a big deal.

What’s changed for a lot of people is the cost. Premiums have gone up, and after a few years it can start to feel like a lot.

So the real question isn’t “did I make a mistake,” it’s “does this still fit my situation today?”

If you’re still traveling and value that flexibility, it may still be the right plan. If things have slowed down or your priorities have changed, it might be worth taking a look at other options.

That’s something we do all the time—just a simple review to see if what you have still makes sense or if there’s a better way to go.

Strategies to Minimize Medicare Supplement Rate Increases

Beneficiaries are not locked into their current plan. Here are several ways to potentially reduce costs:

1. Compare Plans Annually

Reviewing your Medicare Supplement coverage each year can help identify lower-cost options with similar benefits.

Can I change my Supplemental/Medigap plan at any time?

You can apply to change your Medicare Supplement plan at any time during the year—but that doesn’t always mean you’ll be approved.In most cases, switching plans requires answering health questions (underwriting). If you’re in good health, it can be a great way to lower your premium or improve your coverage. But if you have certain conditions, you could be declined.

There are some situations where you can switch without underwriting—like when you first turn 65, lose other coverage, or qualify for certain guaranteed issue rights—but those are specific windows.

This is one of those areas where timing really matters, so it’s worth reviewing your options before making a move to see what’s actually available to you.

2. Consider Alternative Plan Options

Depending on your needs, switching plans may reduce premiums:

- Plan G: Comprehensive coverage with predictable costs. Learn more about the best way to apply for Medicare with a Plan G Supplement.

- Plan N: Lower premium with some cost-sharing

- High Deductible Plan G: Significantly lower premium with a higher deductible

3. Understand Underwriting Requirements

In most states, changing Medicare Supplement plans requires answering health questions. Beneficiaries in good health may qualify for lower rates. Be aware that certain medications can create underwriting surprises, so it's worth understanding how this works before applying.

4. Evaluate Long-Term Rate Stability

Not all carriers price their plans the same way. Reviewing a company's history of rate increases can be just as important as the current premium.

5. Work with an Independent Medicare Agent

An independent agent can compare multiple carriers, explain differences between plans, and help determine whether switching makes sense based on both cost and coverage. If you're unsure where to start, read about why working with a local independent agent can make all the difference.

Do I have to pay extra to use a local Medicare Licensed Insurance agent?

No—you don’t pay anything extra to work with a local Medicare agent.The insurance companies pay agents, whether you go through an agent or enroll directly yourself. So you’re getting guidance, help comparing plans, and ongoing support at no additional cost.

That’s why I always tell people—take advantage of it. It’s a lot easier to have someone walk you through your options and be there if questions come up later.

Important Considerations

- Benefits for each Medicare Supplement plan type are standardized by Medicare. A Plan G from one carrier covers the exact same things as a Plan G from another.

- Premiums can vary significantly between carriers for the same coverage

- Switching plans may not be appropriate for everyone, especially if underwriting is a concern

Final Thoughts

Medicare Supplement rate increases are a normal part of the program, but overpaying doesn't have to be.

Taking time to review your plan and compare options can help ensure you're getting the best value for your coverage, both now and in the future.

About the Author: Michael McGarrigle is an independent Medicare agent based in Melbourne, Florida, serving clients throughout Brevard County and beyond since 1997. He specializes in helping Medicare beneficiaries compare Medicare Supplement and Medicare Advantage plans to find the best fit for their needs.