Does Medicare Cover Dementia Care, Memory Care, or Assisted Living?

-

October 15, 2025

When a loved one is diagnosed with dementia, families often face a difficult mix of emotions; concern for their safety, uncertainty about what comes next, and confusion about how to afford the care they’ll need. Medicare plays a crucial role in helping seniors access healthcare, but when it comes to dementia, coverage can be complicated. Understanding what Medicare does and doesn’t pay for (including memory care, assisted living, and nursing home stays) can help families make informed decisions and plan ahead with confidence.

Understanding Dementia and the Need for Ongoing Care

Dementia is not a single disease, but a general term for conditions that affect memory, thinking, and behavior. Alzheimer’s disease is the most common form, but other types (such as vascular dementia, Lewy body dementia, and frontotemporal dementia) also affect millions of older adults.

As dementia progresses, individuals often require more than just medical treatment. They need supervision, help with daily activities, and emotional support. These needs typically grow over time, which is why families begin to explore in-home care or long-term care services. However, this is where many families first encounter confusion: Medicare does not usually cover long-term or custodial care, even if it’s needed due to dementia.

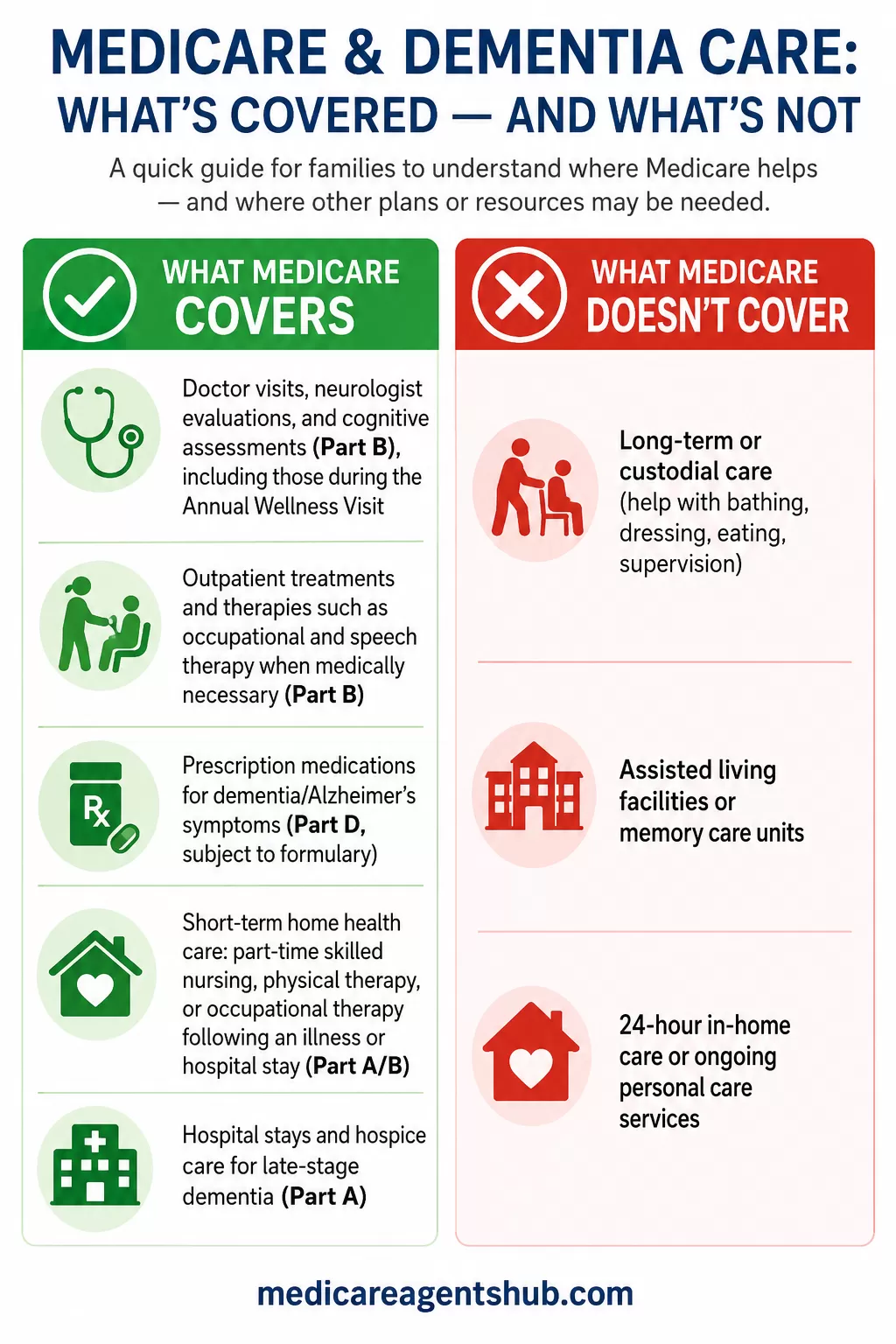

What Medicare Does Cover

Medicare’s coverage for dementia-related care depends on the type of service. While it doesn’t cover full-time caregiving or assisted living, it does provide several important benefits that can ease some of the financial burden.

1. Doctor Visits and Diagnosis

Medicare Part B covers visits to doctors, neurologists, and specialists who evaluate and diagnose dementia. It also covers the cognitive assessments used to detect memory problems, including those performed during the Annual Wellness Visit. This makes it possible for families to get an early diagnosis and begin planning appropriate care.

2. Outpatient Treatments and Therapies

If a doctor recommends occupational therapy, speech therapy, or other outpatient treatments to help manage dementia symptoms, these services may be covered under Part B as long as they are deemed medically necessary.

3. Prescription Medications

Many dementia and Alzheimer’s medications, including those used to manage symptoms and slow disease progression, are covered under Medicare Part D (the prescription drug plan). Coverage varies depending on the specific plan, so families should review the formulary to confirm that the prescribed drugs are included.

4. Home Health Care (Short-Term)

If a person with dementia is homebound and requires skilled nursing care or therapy, Medicare may cover limited in-home health services under Part A or Part B. A prior hospital stay is not required, but a doctor must certify a skilled need and the person must meet Medicare’s homebound criteria. Coverage is intermittent and time-limited. It does not include ongoing personal care or companionship.

5. Hospital Care and Hospice Services

Medicare Part A covers hospital stays when medically necessary, as well as hospice care for those in the late stages of dementia. To qualify for Medicare hospice, a doctor must certify a life expectancy of six months or less if the illness runs its normal course, and the patient must elect comfort care rather than curative treatment. Hospice coverage can include nursing care, medications, and emotional support for both the patient and their family.

My mom has dementia and needs in-home dementia care. What Medicare plan will cover this?

Medicare can cover some in-home care for dementia, like skilled nursing, therapy, or cognitive assessments, if your mom is homebound and a doctor certifies the need. However, it does not pay for long-term custodial or 24-hour in-home care. Some Medicare Advantage Special Needs Plans (SNPs) or dual-eligible plans may offer extra dementia-related support and coordination. Because every situation is unique, it’s best to speak with a trusted Medicare agent who can match her care needs with the right plan and benefits.Does Medicare Cover Memory Care, Assisted Living, or Nursing Home Care for Dementia?

This is the question most families really want answered, and the answer is nuanced. Original Medicare treats these settings based on what kind of care is being delivered, not the label on the building.

Memory Care Units

Medicare does not pay the room-and-board cost of a memory care unit, whether it’s a standalone facility or a wing inside an assisted living community. Memory care is considered custodial (help with daily living, supervision, structured activities), and custodial care falls outside Medicare’s scope. Medicare will still pay for medically necessary services a resident receives while living there, like doctor visits, therapy, or short-term skilled nursing, but the housing and 24-hour supervision are private-pay.

Assisted Living for Dementia

Assisted living is treated the same way. Medicare does not cover the monthly cost, meals, or personal care assistance provided in an assisted living facility, even when the resident is there because of dementia. Families typically fund this through private savings, long-term care insurance, veterans’ benefits, or Medicaid waivers that vary state by state.

Nursing Home Care for Dementia

Nursing homes are where the rules trip families up most often. Medicare Part A will cover up to 100 days in a skilled nursing facility, but only after a qualifying 3-day inpatient hospital stay and only when the patient needs daily skilled care (such as rehab after a hip fracture). After the first 20 days there’s a daily coinsurance, and coverage ends entirely once skilled needs stop. A long-term nursing home stay driven purely by dementia (needing help with bathing, eating, or wandering supervision) is considered custodial and is not covered.

Medicaid, not Medicare, is the primary payer for extended nursing home care in the U.S. Families whose loved one may need this level of care long-term should look into Medicaid eligibility rules in their state early. Waiting until funds are nearly gone often means fewer options.

What Medicare Does Not Cover

To summarize the gaps, Medicare does not cover:

-

Long-term or custodial care (help with bathing, dressing, eating, or supervision).

-

Assisted living facilities or memory care units.

-

24-hour in-home care or ongoing personal care services.

-

Long-term nursing home stays beyond the 100-day skilled benefit.

Families who need this type of support often turn to private pay options, long-term care insurance, or Medicaid (for those who qualify) to help cover costs.

What do seniors often misunderstand about Medicare's coverage for long-term care?

The biggest misunderstanding, by far, is that seniors think Medicare will cover their long-term care in a nursing home (SNF) or assisted living.The truth is, Medicare only covers skilled care (SNF), and only for a short time after a qualifying hospital stay and maximizes out at 100 days. It does not cover CUSTODIAL CARE (think along the lines of an Assisted Living Facility - NOT a nursing home! —which is the everyday help people need with things like bathing and dressing. Since custodial care makes up the vast majority of long-term care needs, many people are caught off guard by the massive costs. It's why long-term care insurance and Medicare planning is so crucial!

Exploring Options Beyond Original Medicare

When Medicare’s coverage ends, families often wonder how to fill the gap. A few approaches can help manage the transition:

-

Medicare Advantage Plans (Part C): Some Advantage plans (including special needs plans, or SNPs, built for people with chronic conditions like dementia) offer additional support such as care coordination, transportation, adult day services, or limited in-home help not included in Original Medicare. These benefits vary by plan and by market, so it’s worth reviewing options carefully each year during open enrollment.

-

Medicaid: For those with limited income or assets, Medicaid may cover long-term care services that Medicare does not, including nursing home stays and personal care assistance.

-

Supplemental Insurance (Medigap): Medigap helps pay out-of-pocket costs for Medicare-approved services, but it does not expand coverage to long-term or custodial care.

-

Community Resources: Local organizations and programs (such as the Alzheimer’s Association and adult day centers) often provide respite and caregiver support at little or no cost.

What happens to my Medicare coverage if I enter a skilled nursing facility for rehab but then need long-term care?

Medicare will cover skilled nursing care for a limited time as long as you are improving and still require skilled services, but once your care becomes custodial or long-term, Medicare will no longer cover those costs.At that point, you would be responsible for paying privately, or you may qualify for Medicaid or long-term care insurance if you have it to help cover the extended stay.

The Importance of Planning Ahead

Dementia care needs evolve over time, and families who plan early are often better prepared to manage both emotional and financial challenges. If you’re stepping into a caregiving role, knowing the right questions to ask a Medicare agent can help you advocate effectively for your loved one. It’s wise to start exploring in-home care options, care management programs, and community resources soon after diagnosis. These services can help loved ones remain in a familiar environment longer and reduce caregiver stress.

I'm caring for my spouse with dementia and experiencing caregiver burnout. Will Medicare cover any mental health support for me?

Yes — Medicare covers mental health services like therapy or counseling if you’re diagnosed with conditions such as stress, anxiety, or depression related to caregiving. You can see a Medicare-approved therapist or social worker for support — contact me for help finding covered options and local resources.For many families, combining short-term Medicare benefits with private or community-based services offers the best balance of affordability and quality of life. For example, families might use Medicare-covered therapy and nursing care alongside non-medical in-home assistance. This layered approach can provide both safety and comfort for the individual while keeping costs manageable.

Helping Families Navigate Dementia Care

Caring for a loved one with dementia can feel overwhelming, but meeting with a reliable Medicare advisor and understanding Medicare coverage is an important first step. While Medicare won’t pay for long-term custodial care, memory care, or assisted living, it does offer valuable benefits for diagnosis, treatment, and short-term support. Families who take the time to learn about these benefits, and plan for what’s not covered, are in a stronger position to provide compassionate, consistent care.

With the right mix of Medicare services, community support, and personal planning, families can ensure their loved ones receive the care and dignity they deserve, every step of the way.

Ready for expert help? Use our directory to find a local Medicare agent who understands dementia care needs and can walk your family through the options.