Turning 65 While on Medicare Disability? Here’s What Changes

-

May 7, 2026

If you got Medicare years ago through Social Security Disability and your 65th birthday is on the horizon, you've probably wondered what's about to change. The short answer: your Medicare coverage doesn't disappear or restart, but a few things reset behind the scenes, and one of them is genuinely worth your attention. For many people on disability Medicare, turning 65 is the first real chance to buy a Medigap policy at fair rates, regardless of health history. Most never hear about it.

This guide walks through what actually happens when you age into Medicare at 65 after qualifying through SSDI, what stays the same, what changes, and the steps to take so you don't leave money or coverage on the table.

Reviewed for accuracy by a licensed Medicare insurance agent

The Quick Version: Your Medicare Doesn't Restart

You don't re-enroll. You don't get a new card automatically (unless something else changes). Your Part A and Part B keep going without interruption. The federal government still considers you a Medicare beneficiary; the only thing changing is the reason you qualify, shifting from disability to age.

That said, three things do shift at 65, and one of them is a real opportunity:

- You get a brand-new Medigap Open Enrollment Period: six months of guaranteed-issue rights that effectively wipe the slate clean.

- If you're in a Medicare Advantage plan, you get a Special Enrollment Period to switch plans or move to Original Medicare.

- Some state-specific rules around Medigap pricing for under-65 enrollees stop applying, and your premiums may actually drop.

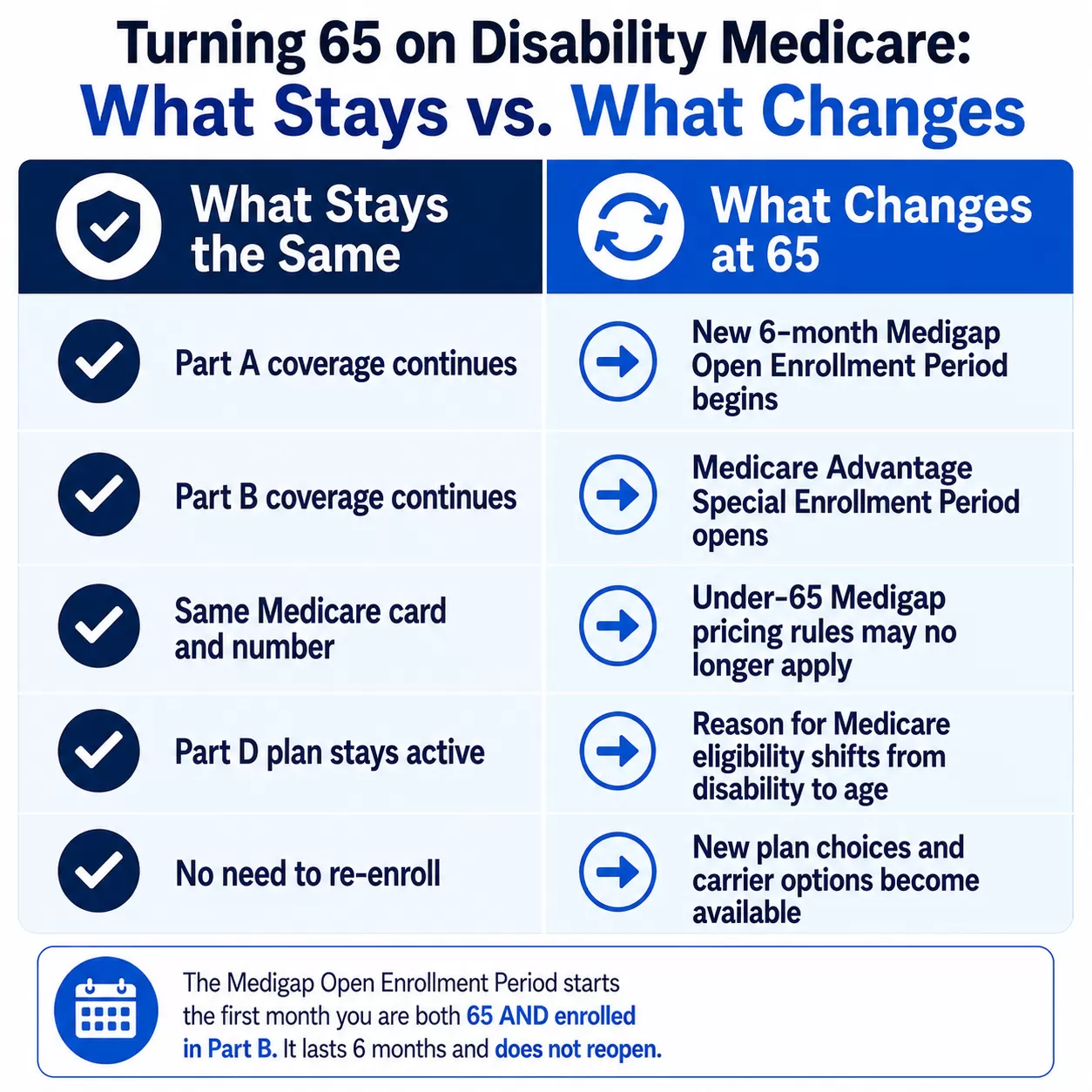

What Stays the Same vs. What Changes at 65

| What Stays the Same | What Changes at 65 |

|---|---|

| Part A coverage continues | New 6-month Medigap Open Enrollment Period begins |

| Part B coverage continues | Medicare Advantage Special Enrollment Period opens |

| Same Medicare card and number | Under-65 Medigap pricing rules may no longer apply |

| Part D plan stays active | Reason for Medicare eligibility shifts from disability to age |

| No need to re-enroll | New plan choices and carrier options become available |

How You Got Here: A Quick Recap

Most people on Medicare under 65 qualified one of three ways:

- SSDI: 24 months of Social Security Disability benefits triggered automatic Medicare enrollment in the 25th month.

- ALS: No waiting period. Medicare started the same month disability benefits did.

- End-Stage Renal Disease (ESRD): Medicare typically started after three months of dialysis.

If any of that sounds unfamiliar, our guide to Medicare eligibility and benefits for disabled individuals under 65 covers the path in more detail. For the broader picture of how Social Security and Medicare interact when disability is involved, see our closer look at Medicare eligibility for those under 65 with disabilities.

How do Social Security and Medicare work together for people with disabilities?

For people with disabilities, Social Security and Medicare are closely connected. If you're under 65 and approved for Social Security Disability Insurance (SSDI), you’ll automatically become eligible for Medicare after receiving disability benefits for 24 months. At that point, you’ll be enrolled in both Part A and Part B. If you have ALS, Medicare starts right away with no waiting period. Your Part B premium will typically be deducted from your Social Security check, just like it is for those 65 and older. From there, you can choose to add a Medicare Advantage or Part D drug plan—or even a supplement, depending on your situation. It's a complex process, but having someone guide you through your options can really make it easier.The Big One: A Fresh Medigap Open Enrollment at 65

This is the part most people on disability Medicare have never been told about, and it can be worth thousands of dollars over the rest of your life.

Federal law guarantees a six-month Medigap Open Enrollment Period the first time you're enrolled in Medicare Part B at age 65 or older. During that window, insurance companies cannot:

- Deny you a Medigap policy

- Charge you more because of pre-existing conditions

- Make you wait for coverage to begin

Here's the kicker: this window is brand-new at 65, even if you've already had a Medigap Open Enrollment Period under 65. Federal rules don't actually require insurers to sell Medigap policies to people under 65 (some states do, often at sky-high premiums). So if you tried to buy a supplement when you got Medicare through disability and were either turned down or quoted a premium that made no sense, the door re-opens cleanly the month your Part B becomes effective at 65.

It's a one-shot deal. Miss the six-month window and insurers can underwrite you again, which means medical questions, possible denials, and higher rates based on your health history.

What is Guaranteed Issue for Medicare Supplement plans, and when does it apply?

Guaranteed Issue means you can buy a Medicare Supplement plan without medical underwriting, so the insurance company can’t deny you or charge more because of health conditions. It mainly applies when you first enroll in Medicare at 65, or if you lose certain coverage (like an employer plan or Medicare Advantage) through no fault of your own. During these windows, you get a Medigap plan at the standard rate. Outside of Guaranteed Issue, you usually have to answer health questions to switch plans.Editor's note: The Medigap Open Enrollment Period generally begins the first month you are both 65 or older and enrolled in Medicare Part B, and lasts six months. This is separate from the Initial Enrollment Period for Part A and Part B.

What Actually Happens with Your Existing Coverage

Here's what you should expect by coverage type:

Original Medicare (Part A & Part B)

No action needed. Your coverage continues with the same card and the same premiums (the standard Part B premium for 2026 is $202.90 unless you owe IRMAA based on income). Your Part A premium status (premium-free for most people) doesn't change.

Medicare Advantage Plan

Your plan keeps working. But turning 65 triggers a Special Enrollment Period that lets you switch to a different Medicare Advantage plan, drop back to Original Medicare, or pair Original Medicare with a Medigap plan and a standalone Part D drug plan.

This SEP is separate from your Medigap Open Enrollment Period, which runs on its own clock from the month your Part B is effective at 65.

Medigap (If You Were Able to Get One Under 65)

Some states required insurers to offer Medigap to under-65 enrollees, often at significantly higher premiums than 65+ rates. In many states, people who had access to Medigap under 65 may find that turning 65 opens up more plan choices and often more favorable pricing. Because rules and rates vary by state and carrier, it's worth requesting a fresh quote rather than assuming your current premium will automatically adjust. A pricing review at this milestone is one of the smartest things you can do.

Part D Prescription Drug Plan

Continues without interruption. You can switch Part D plans during the Annual Enrollment Period (October 15 – December 7) like any other Medicare beneficiary. Our Part D plan-selection guide walks through how to compare options.

Medicare rules and Medigap availability can vary by state. This article is general educational information, not personal insurance advice.

The 65-Birthday Decision: Stay, Switch, or Add Medigap

You essentially have three paths once you hit 65:

1. Keep Medicare Advantage

If your current Medicare Advantage plan is working, with your doctors in network, your prescriptions covered, and your out-of-pocket costs feeling reasonable, you don't have to change anything. Just review the plan's Annual Notice of Change each fall to make sure your priorities still match the plan's terms.

2. Move to Original Medicare + Medigap + Part D

This is where the 65 milestone matters most. If you've been frustrated by network restrictions, prior authorizations, or out-of-pocket surprises in your Medicare Advantage plan, your guaranteed-issue Medigap window is the cleanest opportunity you'll ever have to switch. Pair a Medigap plan with a standalone Part D plan and you'll have predictable costs and the freedom to see any provider that accepts Medicare.

For a fuller side-by-side, see how Medicare Supplements and Medicare Advantage plans actually differ.

3. Switch to a Different Medicare Advantage Plan

Maybe Medicare Advantage still fits, but the specific plan doesn't. Your turning-65 SEP gives you a clean shot at switching to a better-fitting plan without waiting for the fall enrollment window.

What's the process for signing up for Medicare if I'm already on disability benefits?

If you’re already receiving disability benefits, the Medicare enrollment process is much simpler because most of it happens automatically. After you’ve received disability benefits for 24 months, Medicare enrolls you in Part A and Part B without you needing to apply, and your card arrives in the mail about three months before your coverage starts.From there, your only real decisions involve whether to keep Part B, whether to add a Part D drug plan, and whether you want a Medigap or Medicare Advantage plan to round out your coverage. So instead of “signing up” from scratch, you’re mainly choosing how to structure your benefits once Medicare becomes active.

Common Mistakes People Make at This Transition

The same handful of issues come up over and over with people aging into Medicare from disability:

- Assuming nothing has changed. Coverage continues, but the Medigap door has just opened in a way it never has before. Treating 65 as a non-event can cost you the only clean shot you'll ever get at a guaranteed-issue supplement.

- Letting the six-month window slip. The Medigap Open Enrollment Period starts the first month you're 65 and enrolled in Part B. Miss it, and insurers can underwrite, deny, or surcharge you based on health history.

- Not asking about a rate review. If you held a Medigap policy under 65 at "disability rates," your premium should drop at 65, but only if your insurer applies the new pricing. Ask.

- Forgetting Part D coordination. If you move from Medicare Advantage (which usually includes drug coverage) to Original Medicare + Medigap, you have to add a standalone Part D plan or face a late-enrollment penalty later.

What to Do in the 90 Days Before Your 65th Birthday

- Confirm your Part B effective date. Your Medigap Open Enrollment Period runs six months from the first day of the month you turn 65 and have Part B. Get this date in writing from Social Security or Medicare.

- Pull your prescription list. Make sure you have an accurate list (drug names, dosages, frequencies) for plan comparisons.

- List your providers. If you might move to Medicare Advantage or switch MA plans, you need a current provider list to check networks.

- Review the math on Medigap. Get quotes on Plan G and Plan N at minimum. The premium difference between Medigap and Medicare Advantage is real, but so is the predictability, so run the numbers for your situation.

- Talk to a local independent agent. An independent Medicare broker (or one in your state) can pull quotes from multiple carriers and walk you through the trade-offs without pushing one company. Here's how to find a good one.

Frequently Asked Questions

Do I need to re-enroll in Medicare when I turn 65 if I'm already on disability Medicare?

No. Your Part A and Part B coverage continues without interruption. You don't need to fill out new applications or contact Medicare to keep your existing coverage. The transition from disability-based Medicare to age-based Medicare happens automatically behind the scenes.

Do I get a new Medigap Open Enrollment Period when I turn 65?

Yes. Federal law gives you a fresh six-month Medigap Open Enrollment Period beginning the first month you are both 65 and enrolled in Part B. During this window, insurers must sell you any Medigap plan they offer at the standard rate, with no health questions or denials. This applies even if you already had a Medigap OEP when you first got Medicare under 65.

Can I switch from Medicare Advantage to Medigap when I turn 65?

Yes. Turning 65 triggers a Special Enrollment Period that lets you leave your Medicare Advantage plan and return to Original Medicare. You can then use your Medigap Open Enrollment Period to buy a supplement with guaranteed-issue protections. Just make sure you also pick up a standalone Part D drug plan if your Medicare Advantage plan was covering prescriptions.

Will my Medicare card change when I turn 65?

In most cases, your existing Medicare card stays the same. Your Medicare number, Part A effective date, and Part B effective date don't change just because you turned 65. If anything else changes (like a name change), you'd get an updated card, but the birthday itself doesn't trigger a new one.

Does my Part D plan change when I turn 65?

No. Your Part D prescription drug plan continues as-is. You can review and switch Part D plans during the Annual Enrollment Period each fall (October 15 through December 7), but turning 65 doesn't require any action on Part D specifically.

One Window, One Decision

Aging into Medicare at 65 from disability isn't a restart, but it isn't a non-event either. The Part A and Part B coverage you've already had keeps going. What changes is the playing field around it. Specifically, the Medigap market opens up to you in a way it likely never has before, and any Medicare Advantage decisions you've been living with become reversible for a short window.

Use the six months. Get quotes. Compare against what you have. If the math works, switch. If it doesn't, at least you'll have made the decision with eyes open instead of finding out about the window after it closed. Either way, talking through your options with a licensed Medicare agent who knows your state's rules is time well spent, and that's exactly the kind of decision a local independent broker is built to help with.