10 Real Medicare Frustrations Seniors Face (And How Agents Respond)

")

-

February 16, 2026

If you've ever been hit with an unexpected Medicare bill, had a claim denied, or discovered your plan doesn't cover what you thought it would, you're not alone. These are among the most common complaints seniors bring to licensed Medicare agents, and they happen far more often than most people realize.

Medicare coverage problems rarely stem from bad intentions. They're the byproduct of a system that's genuinely complex: fine print determines what's covered, enrollment windows are unforgiving, and two plans that sound similar on paper can work very differently in practice. From dental coverage that doesn't cover what you need to ambulance bills nobody warned you about, each of these issues has an explanation, and usually a path forward.

We gathered 10 of the most common frustrations that seniors share with licensed agents, then asked those agents to respond directly. No sugarcoating. No corporate deflection. Just honest context about what happened, why it happened, and what you can do next.

1. Medicare Advantage Dental Coverage: “I Picked a Plan for the Dental, and It Barely Covers Anything”

This is one of the most frequent complaints agents hear. A senior enrolls in a Medicare Advantage plan because it advertises dental coverage, only to discover that “dental” means two cleanings a year and maybe an X-ray, not the crown or implant they actually need.

The issue isn't that plans are lying, exactly. It's that dental coverage in Medicare Advantage varies enormously from plan to plan, and the broad marketing language doesn't reflect the limits. Some plans offer comprehensive dental that includes major procedures; many don't. The details are buried in the Evidence of Coverage (EOC) document, not the TV ad or the mailer that showed up in your mailbox.

This is also where the distinction between preventive and comprehensive dental matters. Most plans cover preventive care (cleanings, exams) at little or no cost, but restorative work like crowns, bridges, and dentures often comes with significant copays or annual dollar caps, sometimes as low as $1,000 to $1,500 per year. If you're comparing plans, look specifically at the dental rider details and annual maximums, not just whether “dental” is listed as a benefit.

I picked a Medicare Advantage plan because of the dental and now I found out it only covers cleanings. Why didn't anyone tell me this upfront?

That happens more often than you’d think. Many people assume “dental coverage” means everything, but most Medicare Advantage dental benefits are limited, often just preventive care like cleanings, exams, and X-rays.Agents or plan materials should disclose this, but sometimes the details are easy to miss in brochures or summaries. It’s always a good idea to check the Summary of Benefits or ask specifically about restorative or major services before enrolling.

2. Medicare Prior Authorization: “I Need a Knee Replacement and Suddenly They Want Prior Authorization”

Prior authorization — the requirement that your insurance company pre-approve a procedure before it's done — catches many seniors off guard, especially those who assumed their plan would simply cover what their doctor recommended.

This is standard practice for high-cost procedures like joint replacements, certain imaging tests, and specialty referrals. It exists primarily in Medicare Advantage plans, though some Original Medicare situations involve similar requirements. Prior authorization doesn't necessarily mean your procedure won't be covered; it means the insurer wants to confirm it's medically necessary before committing to pay. But the process can introduce delays, and in some cases, the request is denied.

If a prior authorization is denied, you have the right to appeal. Your doctor's office can often help by submitting additional clinical documentation. Agents recommend asking your provider upfront whether prior authorization is required and how long the process typically takes, so there are no surprises when you're already scheduled for surgery.

I called to ask about a knee replacement and suddenly they said I need prior authorization. I thought my plan was supposed to be good-what's going on?

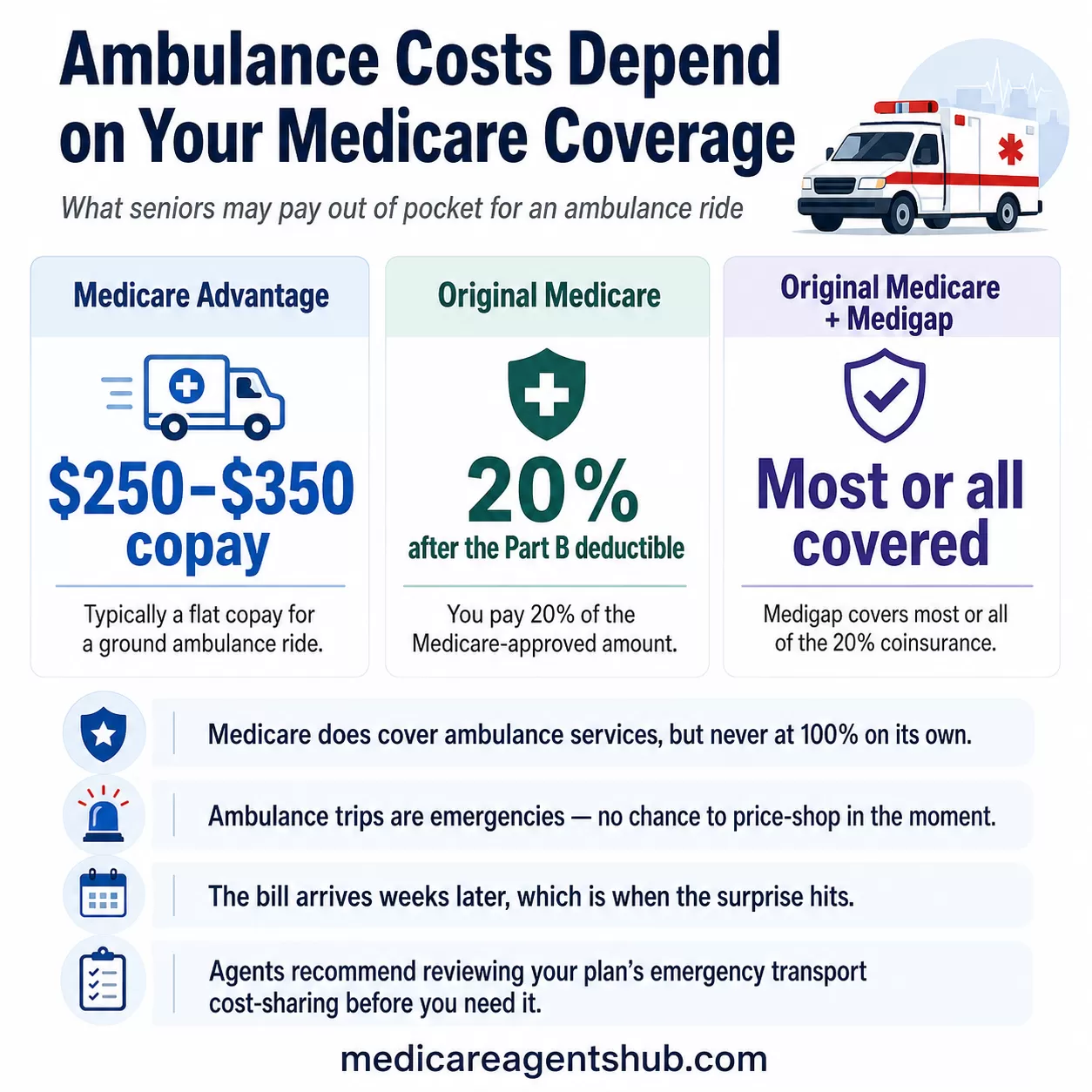

It sounds like your doctor's office is requiring prior authorization for your knee replacement surgery. This is a common procedure, and it essentially means your insurance needs to approve the treatment before it's performed. Prior authorization helps insurance companies determine if the procedure is medically necessary and covered by your plan, ensuring you aren't unexpectedly billed for the cost.3. Unexpected Ambulance Bills: “I Got a $300 Ambulance Bill I Thought Was Covered”

Emergency transport is one of Medicare's most misunderstood benefits. Many seniors assume that if they call an ambulance, Medicare pays the full bill. In reality, your out-of-pocket cost depends entirely on your plan type, and the amount can be a genuine shock.

With Medicare Advantage, you'll typically owe a copay, often in the $250–$350 range for a ground ambulance. With Original Medicare alone (no supplement), you're responsible for 20% of the Medicare-approved amount after your Part B deductible. A Medigap plan would cover most or all of that 20%, which is one reason agents frequently emphasize the importance of supplemental coverage for people on Original Medicare.

What makes this particularly frustrating is that ambulance situations are, by definition, emergencies. Nobody is price-shopping in the moment. The bill arrives weeks later, and that's when the confusion hits. Understanding your plan's emergency transport cost-sharing ahead of time is the best way to avoid the surprise.

I just got a $300 bill for an ambulance ride I thought was covered. Am I the only one who didn't know Medicare doesn't pay for all emergency transport?

You’re definitely not alone — this surprises many people. Medicare Part B covers ambulance services only when they’re medically necessary, and even then it generally pays 80% of the approved amount. The remaining 20% coinsurance, plus any deductible, is your responsibility unless you have supplemental coverage. Bills can also happen if the ambulance provider is out of network under a Medicare Advantage plan. This is a common reason people choose a Medigap plan to help avoid these unexpected costs.4. Provider Network Problems: “My Plan Listed My Doctor as In-Network, but Now They Say He's Not”

Provider directories aren't always accurate, and that's a legitimate, widespread problem. Doctors can leave a Medicare Advantage plan's network at any time during the year, and the plan's online directory may not reflect the change for weeks or even months.

This can happen because of contract disputes, changes in reimbursement rates, or a provider joining or leaving a medical group. The frustrating part is that you may have chosen the plan specifically because your doctor was listed. In some cases, you may be entitled to transitional coverage that allows you to continue seeing your doctor for a limited period, but this depends on your plan's specific policies.

Agents recommend a two-step verification: check the plan's directory and call the doctor's office directly to confirm they're currently accepting your plan. Do this before enrolling, and again at the start of each plan year, since networks can change during the Annual Election Period. If your doctor does leave the network mid-year, contact your plan immediately to understand your options, including whether you qualify for a Special Enrollment Period to switch plans.

My Medicare Advantage plan listed my doctor, but now they say he's out of network. How is that even allowed?

Plans and doctors and clinics are allowed to leave for a variety of reasons usually related to administrative and financial burdens. Sometimes doctors leave because of slow Medicare and insurance reimbursements rates. It is always a good idea to review your Medicare advantage plan each year during annual enrollment period to make sure the plan is meeting your needs and that your doctor is still in that plan.5. Medigap Enrollment Mistakes: “I Missed My Medigap Window by a Few Months and Now Nobody Will Cover Me”

This is one of the most consequential rules in Medicare, and one of the most common mistakes seniors make. Your Medigap Open Enrollment Period starts the month you turn 65 and enroll in Part B, and it lasts exactly six months. During that window, insurers cannot deny you coverage or charge more due to health conditions.

After the window closes, you're subject to medical underwriting in most states. That means an insurer can deny your application, charge higher premiums, or exclude pre-existing conditions. There's no federal requirement for them to accept you. A few states have their own protections, like guaranteed-issue rules during certain periods, but in most of the country, missing this window can permanently affect your coverage options.

This is why agents push so hard to educate clients about this deadline early. It's also why understanding all of Medicare's enrollment periods is so critical: each window has different rules, different consequences, and different deadlines that don't wait for anyone.

I missed my Medigap window by a few months and now no one will cover me without underwriting. Why isn't this rule more well known?

Medigap open enrollment period is the 6 months after you first enroll in Part B. It is hidden in the fine print unfortunately. However, you may qualify for a Special enrollment period where you might not need to undergo underwriting. To best determine this you would need to speak with a licensed agent in your area for assistance.I would contact a local agent to inquire about your specific circumstances and see if there are options for you.

6. Medicare Part D and Insulin Costs: “My Insulin Shot Up in Price — Didn't the Inflation Reduction Act Fix This?”

The Inflation Reduction Act capped insulin copays at $35 per month for Medicare Part D enrollees, and that's been a genuine win for millions of beneficiaries. But the details matter, and not every senior has seen the savings they expected.

The $35 cap applies to covered insulin products under your specific plan's formulary. If your plan changed its formulary or your insulin isn't on the preferred tier, you could still face higher costs or need to switch to a different brand. Formularies are not static: plans can and do change which drugs they cover, what tier they're placed on, and what prior authorization requirements apply from one year to the next.

Agents say the most common issue is that seniors stay on the same Part D plan year after year without reviewing their Annual Notice of Change (ANOC), which outlines formulary and cost changes for the coming year. A drug that was on the preferred tier last year may not be covered the same way this year.

I've had the same Part D plan for years, but this year my insulin shot up in price. Did the Inflation Reduction Act not fix this yet?

The Inflation Reduction Act did lower insulin costs, but there are a few reasons you might still see a higher price. The law only caps your cost at $35 a month for insulin that your Part D plan actually covers, so if your plan changed its formulary, pharmacy network, or the specific insulin brand you use, your price could go up even though the cap is in place.7. Out-of-Network Costs With Medicare PPOs: “I Picked a PPO for Flexibility, but Out-of-Network Bills Are Outrageous”

A Medicare Advantage PPO does give you the flexibility to see out-of-network providers, but “flexibility” doesn't mean “affordable.” When you go out of network, the plan covers a smaller percentage of the cost, and you're responsible for the difference. In some cases, that difference can be substantial.

Many seniors choose PPOs specifically for the freedom to see any provider, then discover that the out-of-network cost-sharing makes that freedom impractical for anything beyond occasional use. Out-of-network copays and coinsurance rates are typically much higher, and there's often a separate (and higher) out-of-pocket maximum for out-of-network care. Some providers may also bill you for amounts above what the plan considers “reasonable,” leaving you with an even larger balance.

Agents say it's critical to understand the plan's out-of-network copays, coinsurance rates, and maximum out-of-pocket limits before enrolling, not just that out-of-network care is “allowed.” If you regularly see specialists or anticipate needing care outside your local area, compare the in-network and out-of-network cost structures side by side. The trade-offs that come with Medicare Advantage are real, and network flexibility is one of the biggest areas where expectations and reality diverge. A knowledgeable Medicare Advantage agent can help you compare these cost structures before you enroll, not after.

I picked a PPO for the flexibility, but now every time I go out of network the bills are outrageous. What's the point of even having a PPO?

A PPO gives you permission, not price protection, to go out of network. When you do, the insurer only pays a “reasonable” amount, and the provider can bill you the rest—so costs can explode fast. The real value of a PPO is access to specific doctors, travel flexibility, or second opinions, not routine care outside the network. If you use out-of-network providers often, a PPO usually ends up being an expensive illusion of flexibility.8. IRMAA and Losing a Spouse: “My Husband Passed Away and Now My Medicare Premiums Went Up”

Losing a spouse is devastating enough without a surprise increase in your Medicare costs. But it happens, and there's a specific, often overlooked reason why. When your spouse passes away, your tax filing status changes from “married filing jointly” to “single,” which can push your income into a higher bracket for IRMAA (the Income-Related Monthly Adjustment Amount).

IRMAA is a surcharge added to your Part B and Part D premiums when your income exceeds certain thresholds. The problem after losing a spouse is that the filing status thresholds for single filers are roughly half those for joint filers. So the same household income that kept you below the surcharge as a couple can put you well above it as an individual, even though nothing about your actual financial situation changed.

Making matters worse, IRMAA is based on your tax return from two years prior, which means the surcharge may not appear immediately; it can hit a year or two after the loss, when you're no longer expecting it. Many seniors don't realize this is happening until they see the higher premium on their Social Security statement.

The good news is that you can file a life-changing event appeal with Social Security (Form SSA-44) to request a premium adjustment. The death of a spouse is one of the qualifying life-changing events, and agents say this is one of the first things they walk clients through after a loss.

My husband passed away and now my Medicare premiums went up. Why does losing someone raise your costs?

Medicare premiums often rise after a spouse passes away due to the "widow’s penalty," where your tax filing status changes from "married filing jointly" to "single," making it easier to exceed income thresholds. Additionally, IRMAA (Income-Related Monthly Adjustment Amount) uses income from two years prior, meaning past joint income may trigger higher premiums now.9. Coverage Gaps for Snowbirds: “I Thought I Was Covered During My Snowbird Months in Florida”

If you spend winters in Florida (or Arizona, Texas, or anywhere outside your home state), your coverage depends entirely on your plan type. Original Medicare works nationwide: any doctor who accepts Medicare will see you in any state. But many Medicare Advantage plans are regional, meaning your coverage may be limited or nonexistent outside your plan's service area.

Agents say this is one of the most common surprises for snowbirds, and it often surfaces at the worst possible time, when someone needs care while away from home. Emergency care is generally covered regardless of where you are, but routine visits, specialist appointments, and prescriptions can all be affected if you're outside your network's geography.

The typical fix is switching to either Original Medicare with a Medigap supplement (which provides nationwide coverage with no network restrictions) or finding a Medicare Advantage PPO with a nationwide network. But that switch can only happen during specific enrollment periods, so planning ahead is essential. For a detailed breakdown of what snowbirds need to consider, see our full guide on how Medicare works when you live in two states. If you already know you'll be splitting time between states, bring that up with your agent before you enroll, not after you've already discovered a gap.

I thought I was covered during my snowbird months in Florida, but apparently not. What kind of plan do I actually need for that?

The plans can vary. A Medicare Supplement plan is good anywhere in the U.S., you can see any doctor that accepts Medicare. For Medicare Advantage plans, either an HMO or a PPO, some plans are set up to allow you to travel and still be able to access providers who participate in the network. You would need to check with your broker or directly with the carrier to verify which plans allow this.10. Medicare Scam Calls: “I Almost Fell for a Call Promising Free Groceries if I Switched Plans”

Scam calls targeting Medicare beneficiaries are a growing problem, and “free groceries” is one of the most common hooks. These callers aren't licensed agents; they're telemarketers or outright scammers trying to get you to switch plans so they can earn a commission, collect your personal information, or both. In some cases, they'll enroll you in a plan without your informed consent, and you won't realize what happened until your coverage changes.

Real Medicare agents are bound by strict CMS marketing guidelines. They cannot promise benefits you don't qualify for, they cannot cold-call you without your prior written consent, and they cannot use high-pressure tactics to force a decision. If someone calls out of the blue offering free groceries, gift cards, cash, or “upgraded benefits” to switch plans, that's a red flag for Medicare fraud.

Some of these operations are sophisticated: they'll reference your current plan by name, quote your Medicare number, or claim to be calling “from Medicare.” Medicare itself does not make unsolicited phone calls, full stop. If you receive a suspicious call, hang up and report it to 1-800-MEDICARE (1-800-633-4227). You can also file a complaint with the FTC or your State Health Insurance Assistance Program (SHIP). Agents say the best defense is simple: if you didn't initiate the conversation, don't share any personal or plan information.

I got a call from a "Medicare agent" promising me free groceries and I almost fell for it. Why is this kind of marketing allowed?

This is generally a fraudulent scam where the caller is trying to get your personal information. Medicare agents can not call people without their permission. There are some Dual Special Needs Medicare Advantage plans that offer funds for healthy groceries, but you have to qualify for those by income and assets. People should not talk with cold callers who use this bait and switch tactic.Why These Frustrations Keep Happening

Every one of these frustrations comes from a real person dealing with a real gap between what they expected and what they got. That gap isn't usually the result of bad plans or bad agents; it's the result of a system where critical details are spread across multiple documents, enrollment windows are strict, and the consequences of small oversights can be lasting and expensive.

The patterns are remarkably consistent. On Medicare Agents Hub, we see the same issues surface year after year across thousands of agent-client conversations: seniors who didn't review their plan's formulary before renewal, who missed a critical enrollment window by weeks, who assumed “covered” meant “fully covered,” or who chose a plan based on a TV ad without reading the Evidence of Coverage. Each section of this article reflects a frustration that agents deal with regularly — not once, but dozens or hundreds of times across their careers.

That's also what makes the agent perspective here so valuable. These aren't hypothetical scenarios or editorial guesses. They're drawn from the real, recurring conversations that happen between beneficiaries and licensed professionals on our platform every day.

What You Can Do Next

If any of these frustrations sound familiar, or if you want to make sure they don't happen to you, here's where to start:

- Review your current plan. Pull out your Evidence of Coverage and check for common Medicare mistakes that could be costing you money or limiting your care. Pay particular attention to formulary changes, network updates, and cost-sharing details.

- Talk to a licensed, independent agent. A local Medicare agent can walk you through your options: what's covered, what's not, and what changes make sense for your specific situation. Their guidance is free, and a good agent will help you understand the fine print before enrollment, not after a surprise bill.

- Keep learning. The more you understand about how Medicare actually works, the better positioned you are to avoid surprises. Every section of this article links to deeper guides on the specific topics covered, from enrollment periods and Medigap to IRMAA appeals and prescription drug savings.

Editor's Note: This article is part of Medicare Agents Hub's ongoing commitment to honest, expert-backed Medicare education. Every frustration featured here reflects patterns we see repeatedly across our platform, where more than 20,000 licensed agents help seniors with coverage decisions in communities nationwide. Our editorial team works directly with these agents to surface the issues that matter most, and to make sure the guidance you find here is grounded in real experience, not marketing copy.