Should Medicare Cover Dental, Vision, and Hearing? Agents Disagree About the Real Cost

-

Last Updated July 21, 2026

Does Medicare Cover Dental, Vision, and Hearing?

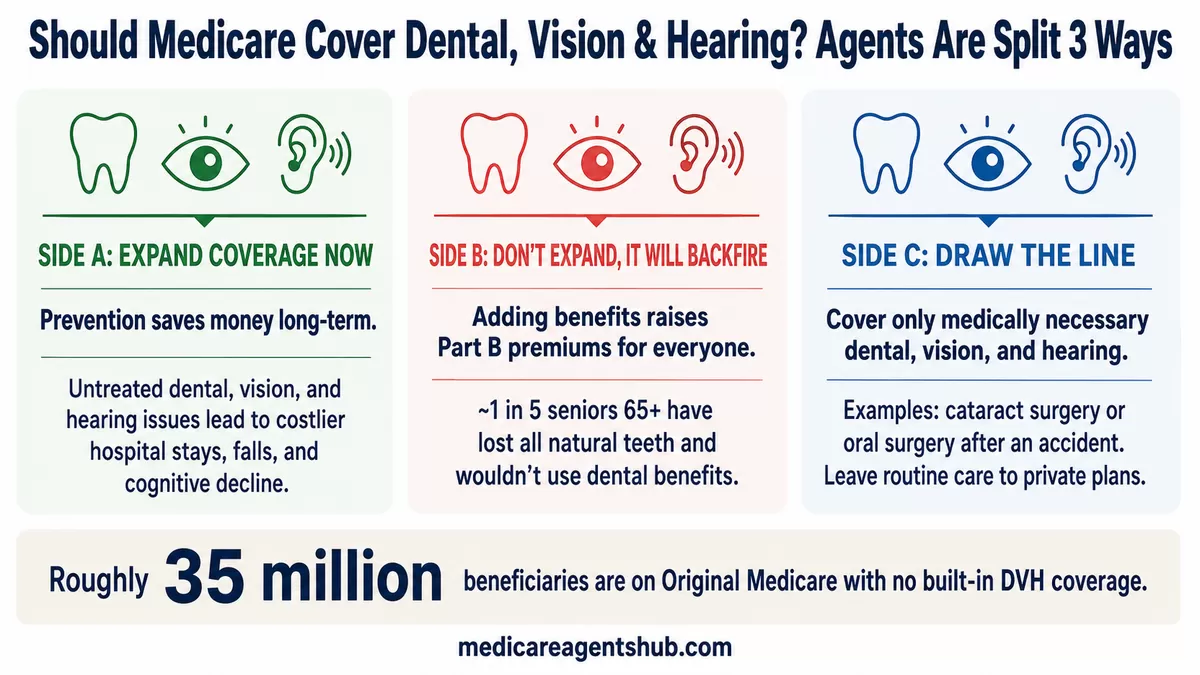

Original Medicare has never covered routine dental, vision, or hearing care. Not in 1965 when the program launched, and not today. That leaves roughly 35 million beneficiaries on Original Medicare without coverage for cleanings, glasses, or hearing aids unless they buy separate policies or switch to Medicare Advantage.

The policy question sounds simple: should Medicare close this gap? But ask the licensed agents who help seniors navigate these decisions every day, and you get a genuine split. Some believe expanding coverage is overdue. Others warn it would raise costs for everyone. And a third group says the real answer lies somewhere in between, distinguishing medically necessary care from routine services.

We pulled answers from hundreds of agents on Medicare Agents Hub to map out the debate.

Side A: Expand Coverage Now

The Preventive Care Argument

Agents who favor expansion consistently point to the same logic: dental disease is a leading indicator of broader health problems. Untreated gum disease is linked to cardiac issues, diabetes complications, and infections that lead to expensive hospital stays. Catching these problems early at the dentist's office is cheaper than treating them in the ER.

Several agents framed it as a pay-now-or-pay-more-later problem. Preventive care for vision, dental, and hearing catches issues before they become chronic, and the cost of early treatment is a fraction of what the system spends on emergency or late-stage intervention.

Others pointed to the downstream effects beyond dental. Untreated hearing loss can lead to isolation and depression, and neglected vision problems raise fall risk. All of these eventually land back on Medicare's tab as hospital admissions and specialist referrals. Research backs this up: untreated hearing loss has been linked to cognitive decline and dementia risk, and missed vision problems can lead to falls, which are a leading cause of injury-related hospitalization among seniors.

Should Medicare cover dental, vision, and hearing, or would that just make it more expensive for everyone?

Adding dental, vision, and hearing coverage to traditional Medicare would likely increase costs for some beneficiaries, but it could also improve overall health outcomes and potentially reduce healthcare spending in the long run by addressing preventative issues early. Currently, Original Medicare doesn't cover routine dental, vision, or hearing care, leading to high out-of-pocket costs for many beneficiaries and potentially delaying or forgoing necessary care.The Equity Problem

Another angle pro-expansion agents raise: the current system creates a two-tier structure. Medicare Advantage plans frequently include dental, vision, and hearing benefits at no additional premium. But beneficiaries who stay on Original Medicare with a Medigap supplement get nothing for these services and must purchase standalone policies.

Multiple agents highlighted the affordability gap this creates. Items like dentures, glasses, and hearing aids are expensive, and without routine coverage under Original Medicare, many beneficiaries face steep out-of-pocket costs that lead them to delay or skip care entirely.

Agents who work with dental coverage in Medicare Advantage know the benefit has limitations. Many MA dental plans cap at $1,000 to $3,000 per year, impose network restrictions, and limit what procedures they will cover. The argument is that a universal Medicare benefit could standardize coverage rather than leaving it to individual plan design.

Should Medicare cover dental, vision, and hearing, or would that just make it more expensive for everyone?

Currently Medicare cannot afford to cover expenses such as Long Term Care. Dental and Hearing are extremely cost prohibited for "full coverage". Nearly all current Dental plans only cover 50-65%, on average, with a $800 - $3000 maximum benefit (restrictions apply). Leaving the patient to have co-pays and in some cases limited network restrictions.Side B: Don't Expand, It Will Backfire

The Premium Inflation Problem

The most common objection among agents is straightforward: adding benefits raises costs for everyone. Part B premiums already increase annually. Layering dental, vision, and hearing on top would accelerate that trend.

Agent after agent pointed to the same pattern: Part B premiums climb every year as costs rise, and adding new categories of coverage would only compound that trajectory. Some went further, arguing that Medicare was designed for medically necessary care and was never intended to be a comprehensive benefits program. In their view, the funding simply is not there to absorb routine dental, vision, and hearing services on top of existing obligations.

The concern is not hypothetical. When Part D prescription drug coverage was added to Medicare in 2006, it came with its own premiums, deductibles, and a complicated coverage gap. Agents who remember that rollout are wary of repeating the pattern. Understanding how Part B costs really work helps explain why this concern resonates with so many beneficiaries.

How can I get dental and vision coverage with Medicare?

If you have a Medicare Supplement (like, plan G, plan, F, etc.) then you can purchase a Dental/Vision/Hearing plan. It's important to know that D/V/H plans have waiting periods. You must have (be premium-paying) for typically 12 months before you get complete coverage.With a Medicare Advantage plan you need one that has a lot of dental benefits. A qualified Medicare Specialist can help with this. Many plans are cutting way back on dental benefits - or - they're charging more to have more dental benefits. And you want to make sure you use an In-Network dentist to keep your out-of-pocket expenses as low as possible.

Not Everyone Wants or Needs It

Several agents raised a practical point that policy discussions often overlook: not every beneficiary would use these benefits, and some actively don't want them.

One common example: agents noted they work with many Medicare-eligible beneficiaries who have lost all their natural teeth and would prefer other benefits instead. This is not a fringe case. According to the CDC's Oral Health Surveillance Report, roughly 1 in 5 adults aged 65 and older have lost all their natural teeth. Mandating dental coverage for these beneficiaries means they are subsidizing a benefit they cannot use.

Should Medicare cover dental, vision, and hearing, or would that just make it more expensive for everyone?

We have many Medicare-eligible beneficiaries who don't have any teeth and would prefer other benefits instead. Some options include dental, vision, and hearing coverage, such as Medicare Advantage plans.The broader point several agents made is that coverage should be optional, not mandatory. Some suggested modeling it after Part D, where beneficiaries can choose whether to enroll based on their individual needs rather than having the cost baked into everyone's premiums.

The Provider Reimbursement Question

Even agents who like the idea of expanded coverage worry about how dentists would respond. Medicare reimbursement rates for physicians are already a sore point. Would dentists accept what Medicare pays?

Several agents predicted it would become harder to find providers willing to accept Medicare-level reimbursement for dental services. They argued that private insurance companies currently offer superior coverage options, and a government-run dental benefit would likely pay less and deliver less. One agent noted that dentists are not required to accept any insurance at all, and making the economics work would require either mandating participation or paying rates high enough to attract providers voluntarily.

Should Medicare cover dental, vision, and hearing, or would that just make it more expensive for everyone?

Personally, I think Medicare coverage of these services would increase the cost of Medicare for everyone. In addition, I think it would make it tougher for people to find providers that would accept the minimal amount Medicare would pay for these. Lastly, I feel the coverage options that are available from private insurance companies are vastly superior to the coverage Medicare would be able to provide.Side C: Draw the Line Between Medical and Routine

A Middle Ground Approach

A meaningful number of agents land between the two camps. Their position: Medicare should cover medically necessary dental, vision, and hearing services, but not routine care like cleanings and eyeglass prescriptions.

This distinction already exists in fragments. Medicare Part B covers cataract surgery, diagnostic hearing exams ordered by a physician, and dental procedures tied to medical conditions (like oral surgery following an accident). What it does not cover is the routine preventive work: cleanings, fillings, hearing aid fittings, prescription eyeglasses.

Agents in this camp pointed out that Medicare already pays for eye exams and hearing exams because they screen for conditions like cataracts and glaucoma, but it draws the line at the corrective devices. Adding glasses and hearing aids to the program would almost certainly raise costs, while the diagnostic exams that catch serious conditions are already covered.

This middle ground appeals to agents who recognize the health link between dental problems and systemic disease but don't want to see premiums jump for routine care. The idea is to expand coverage for procedures with clear medical necessity while leaving routine maintenance to private plans.

Does Medicare cover hearing aids, or do I have to pay out of pocket?

No! Original Medicare (Part A & Part B) does not generally cover hearing aids or exams for fitting of them. You are responsible for 100% of the cost for routine hearing aids.Medicare Part B, however, may cover the cost of diagnostic hearing exams if ordered by a doctor to treat a specific medical condition.

Which Medicare Plans Cover Dental, Vision, and Hearing?

Regardless of where they stand on policy, agents are practical. They have clients who need dental, vision, and hearing coverage today. Here is what they typically recommend.

Medicare Advantage Dental, Vision, and Hearing Coverage

The most common recommendation by far. Most Medicare Advantage plans bundle dental, vision, and hearing into their benefits package, often with a $0 monthly premium. But agents are quick to point out the tradeoffs: network restrictions, annual benefit caps (often $1,000 to $3,000 for dental), and the requirement to use in-network dental providers.

Agents who favor the MA route see it as the simplest way to pick up these benefits without a separate policy. But others caution that many plans have been scaling back their dental coverage or increasing cost-sharing for more comprehensive benefits. The advice across the board: check what the plan actually covers before assuming dental, vision, and hearing are robust.

How can I get dental and vision coverage with Medicare?

There are typically Medicare Advantage plans in your area that include some level of dental and vision coverage. Medicare.gov, or an agent, can help you find one that gives you the most benefit. Medigap plans (and original Medicare by itself) do NOT cover most dental and vision issues.Note that as costs rise, many Medicare Advantage carriers are pulling back on some of these benefits. In my local area there are several that only cover preventive dental (cleanings and X-rays) and any comprehensive work is paid out of pocket.

As a result more seniors are choosing to add a standalone dental and/or vision plan. These plans operate separately from Medicare and changes to medicare coverage do not affect them.

Before you make any changes to your coverage, it’s a good idea to consult with a broker (or medicare.gov) to assess what will meet your needs.

Standalone Dental, Vision, and Hearing Plans

For beneficiaries on Original Medicare with a Medigap supplement, agents recommend standalone dental, vision, and hearing (DVH) plans. These typically cost between $35 and $75 per month and can be purchased year-round. Carriers may bundle all three, or sell dental, vision, and hearing separately.

Agents consistently note that while these plans fill the gap, they come with their own limitations. Not every beneficiary wants to pay the extra premium, and the coverage often includes waiting periods and annual maximums that shape what you actually get for the money.

How can I get dental and vision coverage with Medicare?

Most Medicare Advantage plans offer some dental/vision coverage. They may require you to see a limited list of Network providers, or they may reimburse you regardless of the dentist you use. It depends on the particular plan.If you are on original Medicare or Medicare with a Medigap plan you will need to purchase an additional Dental / Vision policy. These plans range from $35/mo to $85/mo depending on where you live and the coverage they provide.

Agents who help clients find dental and vision coverage know that standalone plans often come with waiting periods (commonly 12 months for major work) and annual benefit maximums that can leave patients paying a significant share out of pocket.

Discount Programs and Other Options

Some agents mention discount dental plans (not insurance, but membership programs with reduced rates), dental schools, community clinics, and VA benefits for eligible veterans. These are gap-fillers, not comprehensive solutions, but they matter for beneficiaries on tight budgets.

The Real Question Behind the Debate

One agent framed the tension at its core: expanding coverage will increase costs, but especially with dental, it can also prevent serious and expensive health problems down the line. The real question is how much value we place on overall health when weighing it against higher premiums.

That is the crux of it. The agents who favor expansion are betting on long-term savings through prevention. The agents who oppose it are protecting beneficiaries from short-term premium increases. And the agents in the middle are trying to split the difference with a medical necessity standard.

None of these positions is wrong. They reflect different priorities and different client populations. An agent in a rural area where the nearest in-network MA dentist is 90 miles away will see this differently than an agent in a metro area with robust plan options. An agent whose clients are mostly low-income will weight the equity argument differently than one whose clients are higher earners comfortable purchasing standalone plans.

What to Do Right Now

The policy debate could take years. Your dental, vision, and hearing needs are here today. A few practical next steps if you are trying to close the gap in your own coverage:

- Compare a Medicare Advantage plan's built-in DVH benefits against Original Medicare plus a standalone DVH policy for your zip code.

- Confirm your current dentist, eye doctor, or audiologist is in-network before enrolling in any MA plan that bundles these benefits.

- Ask a licensed agent to price out standalone dental, vision, and hearing plans side by side so you can see the real annual cost.

- Check the official coverage rules on Medicare.gov or call 1-800-MEDICARE for federal guidance.

What every agent agrees on: the current system leaves gaps, and beneficiaries need to plan for dental, vision, and hearing costs regardless of what Washington decides. If you are not sure where you stand, comparing Medicare Advantage and Medigap side by side is a good starting point. And if you want to understand what Medicare actually covers for vision or explore hearing plan options through an agent, those resources can help you make a decision based on your situation, not the debate.