Medicare Part D: Common Reasons Generic Drug Prices Increase

-

Last Updated July 22, 2026

Understanding Why Your Generic Drugs Suddenly Cost More

Every year, Medicare beneficiaries across the country are caught off guard when the cost of their familiar generic prescriptions suddenly rises. It’s frustrating — especially when they didn’t change their plan, their medications, or their pharmacy. But often, these price hikes aren’t random.

To better understand what’s happening behind the scenes, Medicare Agents Hub surveyed licensed Medicare brokers and agents nationwide, asking them to explain why generic drug costs can unexpectedly increase under a Medicare Part D plan. Drawing directly from their expert insights, this article explores the key reasons your costs might climb, and what you can do about it.

Changes to Part D plans, shifting formularies, evolving pharmacy networks, and recent legislation like the Inflation Reduction Act all play important roles. By staying informed and proactive, you can handle these changes and avoid unpleasant surprises at the pharmacy counter.

I've been on a Part D plan for a while, and I'm wondering why my generic prescriptions suddenly cost more. Did something change?

Yes — a few things could be behind that sudden jump in your generic prescription costs:Formulary changes: Every year, Part D plans update their drug list. A medication that was once in a lower-cost tier (like Tier 1) might now be moved to a higher tier with a bigger copay.

Preferred pharmacy networks: If you’re no longer using a “preferred” pharmacy, your copays could be higher than before.

Deductible resets: At the start of each year, you may have to meet a new deductible before lower copays kick back in.

Coverage gap: If your total drug costs have reached a certain limit, you may pay more until you move into catastrophic coverage.

The good news is you’re not stuck. A Medicare agent can review your current prescriptions and compare plans to see if there’s a better option that lowers your costs.

Annual Plan and Formulary Changes

One of the biggest reasons generic drug prices can climb under a Medicare Part D plan is simple: plans change every year. Even if you stay enrolled in the same plan, the details behind the scenes (like premiums, copays, deductibles, and covered medications) often shift without much warning.

Several brokers emphasized that beneficiaries receive a "Notice of Change" from their plan each fall. But as one agent pointed out, "plans reset every January, and even if you didn’t switch plans during the Annual Enrollment Period, your plan may have changed on you." Many people overlook these notices, assuming no action is needed, only to be surprised at the pharmacy counter months later.

A common pattern is that formularies — the lists of drugs each plan covers — are updated annually. Medications that were once affordable may be bumped to higher tiers or dropped altogether. Costs tied to premiums, deductibles, and copays also adjust, sometimes dramatically. As one expert noted, "Part D plans update their formularies, premiums, and copays each year, and I’ve seen many people overlook the need to review these changes annually."

Ignoring these changes can quickly lead to higher out-of-pocket costs. Another broker highlighted that "plan formularies can change from year to year, as well as plan deductibles and copays, so it's always best to check your prescription options annually or as your prescriptions change." Simply put: even if your health remains the same, your financial picture under your Part D plan likely won’t.

Action Steps to Stay Ahead:

-

Always review your plan’s "Notice of Change" letter in the fall.

-

During Annual Enrollment (October 15–December 7), recheck your prescriptions against the updated formulary.

-

Ask your broker for a yearly plan review, even if you’re happy with your current coverage.

Tier Reassignments and Medication Shifts

Another key reason generic prescriptions may suddenly cost more is changes to how medications are tiered within your plan’s formulary. Even though a drug remains a "generic," the cost tied to it can shift if the insurance carrier decides to reclassify it into a more expensive tier.

Several brokers pointed out that plans frequently move medications between tiers when they update their formularies each year. One agent explained it clearly: "Carriers can occasionally alter the tier of a medication from 'generic' (Tier 1) to 'preferred generic' (Tier 2). In some cases, a generic medication may even jump up to a Tier 3!"

In the below video, Steve Brauer helps explain the differences in drug tiers on Medicare Part D.

These seemingly small adjustments can make a big difference at the register, with copays rising even though the medication and dosage haven’t changed.

This reshuffling doesn’t always come with a bold announcement. Tier changes are often buried within broader plan updates, making it easy for enrollees to miss the new cost structure until they fill a prescription.

Some agents recommended using your plan’s online tools to monitor potential shifts. "Most carriers have an online RX lookup tool for members; you may try looking up your medications every so often," one broker advised. These lookup systems allow you to see the current tier placement of your prescriptions before facing unexpected charges at the pharmacy.

Action Steps to Protect Yourself:

-

Use your plan’s online formulary lookup tool annually, especially each fall after plan updates.

-

Pay close attention to any tier changes for your essential medications.

-

If a drug moves to a higher tier, ask your doctor if there are equivalent lower-tier alternatives available.

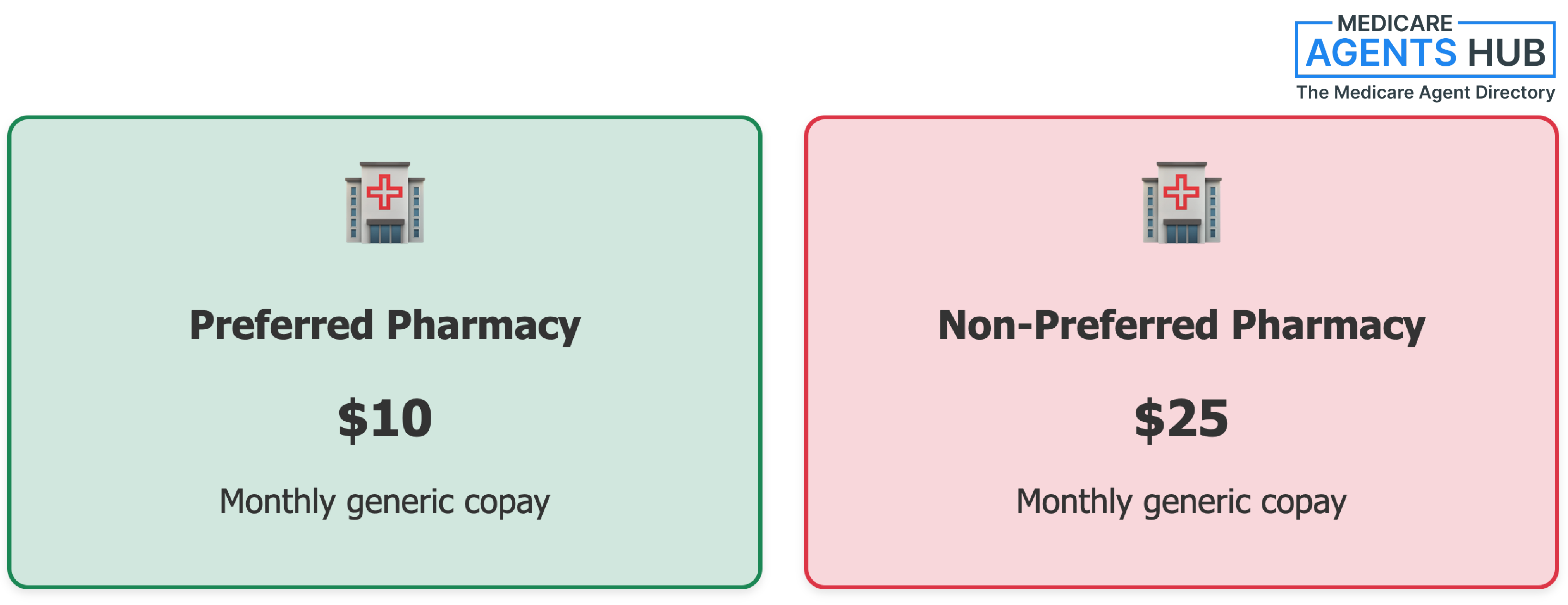

Pharmacy Network Changes

Even when your medications and your plan stay the same, the pharmacy you use can still dramatically affect what you pay. Medicare Part D plans have preferred pharmacy networks that often change from year to year, and if your pharmacy loses its preferred status, your costs can rise even for familiar generic drugs.

Several brokers emphasized that many beneficiaries get caught by surprise because these changes aren’t always obvious. As one agent explained, "If your go-to mom and pop shop isn’t considered a 'preferred' pharmacy anymore, you’ll end up paying more just for sticking with what’s familiar."

What used to be the cheapest and most convenient pharmacy may now charge higher copays simply because the plan's internal contracts shifted behind the scenes.

Another expert insight reinforced this: "Sometimes plans update their formularies at the start of the year... it’s also possible that your pharmacy is no longer a preferred one with your plan, which can raise the cost."

Failing to check your pharmacy's status within your plan’s network could lead to paying significantly more for the exact same medication. It’s a hidden driver of cost increases that many people only notice after they've already spent extra money.

Action Steps to Stay Ahead:

-

Each year, verify that your preferred pharmacy remains "in-network" and "preferred" with your Part D plan.

-

Consider comparing prices across several nearby pharmacies, even within the same chain.

-

If your pharmacy is no longer preferred, switching locations could lower your copays without changing your medication.

Impact of the Inflation Reduction Act

Another factor influencing rising generic drug costs is the ongoing rollout of the Inflation Reduction Act, which is reshaping how Medicare Part D plans manage pricing.

While the Act is designed to cap out-of-pocket costs and improve affordability in the long run, the early phases of its implementation have led to some unexpected shifts in how plans and manufacturers share expenses. Those changes can ripple down to the prices you pay.

Several brokers noted that the Inflation Reduction Act made a major impact on Medicare drug plans starting in 2024. One expert put it simply: "In 2024 the Inflation Reduction Act had a major impact on the Medicare space, specifically Part D and drug plans."

Among the most significant reforms is the upcoming $2,000 out-of-pocket cap on prescription drug spending, which took full effect in 2025.

While this cap is good news for beneficiaries overall, it has led some insurance carriers to adjust the internal cost structures of their plans. As a result, certain generics that once benefited from lower negotiated prices may now see higher out-of-pocket costs for members depending on how each plan redistributed expenses.

One agent explained it this way: "The Act introduced a $2,000 out-of-pocket cap for 2025, but it also altered how plans and manufacturers share costs, which can increase generic prices depending on your specific plan’s structure."

These aren’t government-mandated price hikes. The law caps what you can spend out-of-pocket, but insurers still decide how to rebalance tiers and copays inside their own plans, which is where the pinch on certain generics comes from.

For many Medicare recipients, this means you could feel the effects at the pharmacy counter even before reaching that $2,000 cap. Changes in how costs are divided between insurers, pharmacies, and drug makers can result in smaller but noticeable price increases on generic medications, even for people who didn’t switch plans or medications.

Action Steps to Stay Ahead:

-

Keep an eye out for notices about how your plan is implementing Inflation Reduction Act changes.

-

If your monthly drug bill is spiking, look into the official Medicare Prescription Payment Plan, which lets you spread your Part D costs across the year instead of paying big amounts at the counter.

-

During Annual Enrollment, ask your broker how upcoming legislative shifts might impact your personal drug costs. For free, unbiased help, you can also contact your local State Health Insurance Assistance Program (SHIP) or call 1-800-MEDICARE.

-

Don’t assume "generic = cheap." Costs could temporarily rise depending on your plan’s new pricing structure.

How will the new 2025 Medicare Part D out-of-pocket cap impact seniors and prescription drug costs?

The new $2,000 out-of-pocket limit in 2025 will help those individuals who have high drug costs. The deductible and copays count towards the $2,000 limit. Once that limit is reached, the member will pay $0 for drugs until the end of the year. If you think you will reach the $2,000 limit before the end of the year, you can ask the Drug plan to set up a payment plan that allows you to spread your payments out over the remainder of the year.Individual Medication Factors

Sometimes the real reason your generic drugs are costing more isn’t just about your plan. it’s about your specific medications. Even inside the same Part D plan, different prescriptions can be impacted in different ways, depending on how they're classified, tiered, or priced year over year.

Many brokers emphasized the importance of personalized medication reviews. As one explained, "I would need to know what medications you’re on. That way I can work on that answer by looking at the different formularies from different companies."

Without that level of detail, it’s difficult to know exactly why your costs jumped, because changes can vary from one medication to another, even within the same plan.

It’s not just about whether your drug is still covered.

It’s about how it's covered. Some generics might move into a higher-cost tier, others might stay where they were, and a few might even be dropped from the formulary altogether. One broker recommended, "Let's check which medication you are on with the plan tiers, and compare it to last year so we can see what has changed."

The key takeaway is that blanket advice isn’t enough. What’s happening with your neighbor’s plan or prescriptions might be completely different from what’s happening with yours.

Another broker made it simple: "More information would be needed in order to respond to this question properly."

Technology can help too. Some brokers suggested using your carrier’s online RX lookup tool, a resource that allows you to check real-time formulary status and tier placement for each of your prescriptions.

Action Steps to Stay Ahead:

-

Review your personal medication list with a broker every year during Annual Enrollment.

-

Use your plan’s online drug lookup tools to monitor how your specific medications are classified.

-

If a favorite generic jumps tiers or costs more, ask about alternative options that could save you money.

Other Contributing Factors

Even if your plan stays mostly the same, there are other forces that can quietly drive up the cost of your generic medications, and many aren’t immediately obvious.

Several brokers pointed out that the price of the generic drug itself can increase due to factors like supply chain disruptions, manufacturer pricing changes, or broader market shifts.

In other cases, insurance rules can evolve, changing how drugs are covered or reimbursed even if the formulary technically stays the same.

As one expert summarized neatly: "Generic drug costs might be higher because: your plan changed its preferred drug list, different pharmacies charge different amounts, the price of the generic drug itself went up, you've moved to a different phase of your plan's coverage, and insurance rules are shifting slightly."

Another subtle factor? Moving into a different phase of your Part D plan, such as hitting the deductible, entering the initial coverage period, or moving into the coverage gap (the "donut hole"). Each phase affects your out-of-pocket costs differently, and that can make prescriptions suddenly feel much more expensive, even mid-year.

All of these moving parts make it important to stay proactive, not just with your plan review, but with monitoring how your personal coverage phase or pharmacy costs might be shifting throughout the year.

Action Steps to Stay Ahead:

-

Track your spending to know when you move between drug coverage phases.

-

If prices spike unexpectedly, ask your plan or broker if it’s related to phase changes or supply issues.

-

Shop around pharmacies even mid-year. Small differences in pharmacy pricing can add up over time.

Smart Steps to Protect Your Prescription Budget

If you’ve noticed your generic prescriptions costing more under Medicare Part D, you’re not alone, and you’re not imagining things.

Changes to formularies, plan structures, pharmacy networks, drug tiers, and even broader legislative shifts are creating new pricing realities every year.

Thanks to insights from brokers and Medicare Agents across Medicare Agents Hub, it’s clear that annual plan reviews are no longer optional — they’re essential. Plans change. Pharmacies move in and out of networks. Drugs shift tiers. And as professional guidance on Part D becomes harder to find, staying on top of these shifts yourself is more important than ever. Even broader market forces and legislation like the Inflation Reduction Act can nudge costs upward in ways that catch many people off guard.

And if you’re using a discount card to bridge the gap, be careful: GoodRx and similar tools can sometimes cost Medicare beneficiaries more than they save.

The good news? By staying proactive (reviewing your plan annually, double-checking your pharmacy’s preferred status, using RX lookup tools, and comparing your medication options) you can avoid nasty surprises at the pharmacy counter.

Generic medications still offer incredible value. But to keep maximizing your savings, you need to stay one step ahead of the annual changes baked into the Medicare Part D system.

What are some ways to save on prescription drug costs?

1. Extra Help (Low Income Subsidy). If you qualify, it can significantly lower premiums, deductibles, and copays.2. Ask for Generics (or Therapeutic Alternatives). They usually cost much less than brand-name drugs.

3. Compare Part D plans yearly: Costs and formularies change annually.

4. Manufacturer Assistance Programs. Ask about patient and manufacturer assistance programs: Some drug manufacturers offer discounts or free meds.

5. Use Preferred or Mail-Order Pharmacies. Get medications with preferred pharmacies or mail order: Costs may be lower.

6. Enroll in the Medicare Prescription Payment Plan to spread out the costs evenly every month.

7. Use Discount Programs (Even With Insurance Sometimes). Discount cards can beat your insurance copay in some cases.

8. Talk to a medicare broker to see if you could change to a plan that would cover medication at a lower cost.

9. State & Nonprofit Assistance Programs