6 Medicare Myths Debunked: What You Really Need to Know

-

Last Updated July 16, 2026

Written by Edward Smith, ChFC, CRPS, AIF

Medicare Broker Licensed in OH, GA, IN, KY & TN

Navigating Medicare can be tricky, especially with so much misinformation floating around. Whether you’re approaching the age of eligibility or already enrolled, it’s important to separate fact from fiction to make the best decisions for your health and finances. Let’s debunk some of the most common Medicare myths to give you a clearer understanding of what to expect.

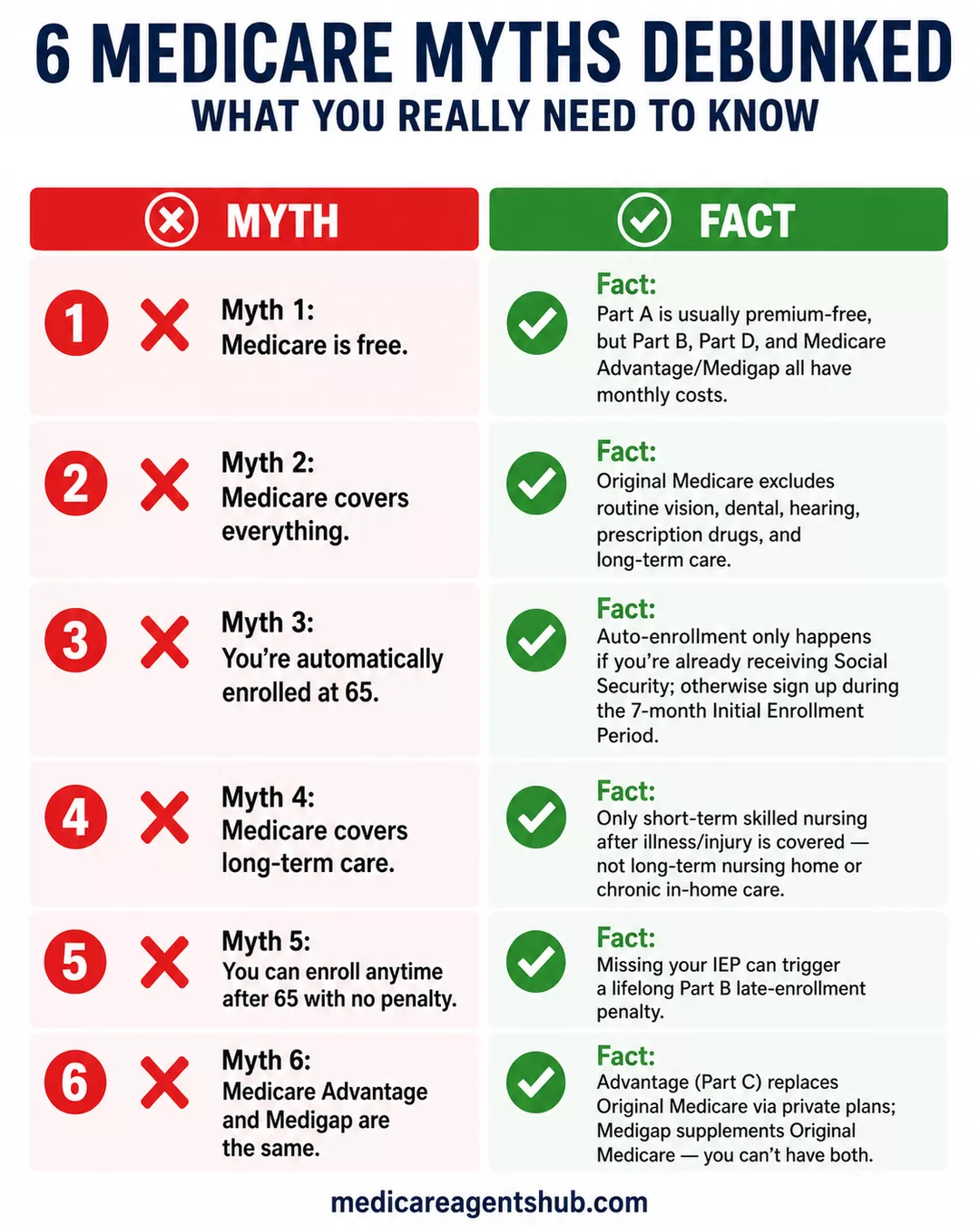

Myth 1: Medicare is Free

One of the most widespread misconceptions is that Medicare is entirely free. While Medicare Part A (hospital coverage) is typically premium-free for most people who have paid Medicare taxes during their working years, there are still costs involved with other parts of Medicare.

- Part B (medical insurance) comes with a monthly premium, which varies based on your income.

- Part D (prescription drug coverage) also requires a monthly cost.

- Medicare Advantage (Part C) plans and Medigap (supplemental insurance) may have additional costs depending on the plan you choose.

It’s important to budget for these expenses when planning for retirement.

Myth 2: Medicare Covers Everything

Another common myth is that Medicare covers all healthcare expenses. While Medicare provides broad coverage, it doesn’t cover everything. Original Medicare (Parts A and B) doesn’t include routine vision, dental, or hearing care, and prescription drug coverage.

In addition to these gaps in coverage, Medicare doesn’t pay for long-term care, such as nursing home stays, which many people don’t realize until they need it. To fill some of these gaps, many beneficiaries opt for a Medigap policy.

I just enrolled in Medicare, and I've got my Part A and B, but I'm hearing there are gaps in coverage. What are these gaps exactly?

For 2026 here are your responsibilities (out of pocket cost).Part A deductible: There is a $1,736 deductible for inpatient hospital care.

Then Medicare part A pays 80% and you are responsible for 20% for 60 days. If you are still hospitalized on the 61st day, you start paying a $434.00 per day coinsurance. If you get out of the hospital a then get re-admitted after a 60-day gap of not being hospitalized, these charges can start over.

Part B Deductible: The annual deductible for part B services is $283. Then Medicare pays 80% ad you are responsible for 20%.

There is not an out-of-pocket maximum. You are responsible for 20% of Whatever unless you have a Medicare Advantage plan which caps the maximum or a Medicare supplement which pays all medical expenses except the $283 part B deductible.

Myth 3: You’re Automatically Enrolled at 65

Many people believe that they’ll automatically be enrolled in Medicare when they turn 65, but that’s not always the case. You are only automatically enrolled if you’re already receiving Social Security benefits. If you’re not, you’ll need to sign up during your Initial Enrollment Period, which starts three months before your 65th birthday and ends three months after.

Missing this enrollment window could lead to late penalties, so it’s essential to mark your calendar and ensure you sign up on time.

Myth 4: Medicare Covers Long-Term Care

Medicare will cover a short-term stay in a skilled nursing facility for rehabilitation after an illness or injury, but it doesn’t cover the cost of long-term care, such as a nursing home or in-home care for chronic conditions. If long-term care is a concern, it’s important to look into additional insurance options, such as long-term care insurance, to protect yourself financially.

Does Medicare fully cover nursing home care, and are there alternatives?

Most nursing home care is custodial care, which helps you with activities of daily living (like bathing, dressing, using the bathroom, and eating) or personal needs that could be done safely and reasonably without professional skills or training. Medicare does not cover this type of care.Medicare Part A (Hospital Insurance) may cover skilled nursing care in a nursing home. It must be medically necessary for you to get skilled nursing care (like if you need help changing sterile dressings). There are limitations.

If you're in a Medicare Advantage Plan (Part C) (like an HMO or PPO) or other Medicare health plan, check with your plan to see if it covers nursing home care. Usually, plans don't help pay for this care unless the nursing home has a contract with the plan. Ask your plan about nursing home coverage and check the facility’s quality ratings before you make any arrangements to enter a nursing home.

Myth 5: You Can Enroll in Medicare Anytime After 65

Another misconception is that you can enroll in Medicare at any time after age 65 without penalty. While you can technically enroll during the General Enrollment Period (January 1 to March 31 each year), if you miss your Initial Enrollment Period, you could face a late enrollment penalty. For example, if you delay signing up for Medicare Part B without having other creditable coverage, you could be hit with a penalty that lasts for the entire time you’re enrolled in Medicare.

Myth 6: Medicare Advantage and Medigap are the Same

Medicare Advantage and Medigap are often confused, but they’re two very different types of coverage. Medicare Advantage (Part C) is an alternative to Original Medicare that provides your Part A and Part B benefits through private insurance companies and often includes Part D prescription coverage.

Medigap, on the other hand, is supplemental insurance that helps cover out-of-pocket costs such as copays, deductibles, and coinsurance for those enrolled in Original Medicare. You can’t have both a Medicare Advantage plan and Medigap, so it’s important to know the differences when selecting the right coverage for you.

What is the biggest disadvantage of the Medicare Advantage plans?

I think some people would say, it's the fact that you have to use a doctor in Network. Where with a Medicare Supplement policy you can go to any doctor that accepts original Medicare. I believe it is simply the higher out of pocket maximum medical cost in a plan year. With a Medicare supplement you only have your premium plus the Medicare part B deductible ($283.00) in 2026 to be responsible for. With a Medicare Advantage plan, you could have a potential $5,000 or more maximum of pocket in any plan year.Furthermore, a lot of agents do not explain the potential benefits of a High-Deductible Plan G. In 2026 the deductible is $2,950. But that is the maximum out of pocket you will pay plus the part B deductible. The difference in the monthly premium for a 65-year-old could be as low as around $40 per month.

Don’t Let Myths Affect Your Healthcare Decisions

Understanding the facts about Medicare can save you from costly mistakes and ensure you get the coverage you need. And beyond myths, there are important questions most seniors never think to ask about Medicare that can make just as big a difference in your coverage. If you have questions or need more information about Medicare eligibility, coverage options, or costs, reach out to us and speak with a licensed insurance agent. We can help clarify your options and guide you through the enrollment process, ensuring you have the best plan for your needs.

Edward Smith, ChFC, CRPS, AIF is a local, licensed agent, certified with many top Medicare Advantage, Prescription Drug and Medicare Supplement insurance plan carriers. I represent most major companies with a Medicare contract and am qualified to answer any questions you may have.