Medicare and Cancer Treatment: What's Covered for Screenings, Chemo, Radiation, and More

-

March 9, 2026

A cancer diagnosis changes everything — and the last thing you need is confusion about what Medicare will and won't pay for. The good news is that Medicare provides substantial coverage for cancer treatment, from preventive screenings to chemotherapy and radiation. But the details matter enormously, and the choices you've made about your Medicare plan can mean the difference between minimal out-of-pocket costs and thousands of dollars in unexpected bills.

This guide breaks down exactly how Medicare covers cancer-related care, drawing on insights from hundreds of licensed Medicare agents who answer cancer coverage questions every day on our platform. These aren't theoretical talking points. They're the real-world guidance that agents consistently give to beneficiaries facing one of the most important healthcare situations of their lives.

Cancer Screenings Medicare Covers (and the Preventive vs. Diagnostic Trap)

Medicare covers a solid lineup of cancer screenings at no cost to you (no copay, no deductible, no coinsurance) as long as the screening is coded as preventive and your provider accepts Medicare assignment. Here's what's covered under Medicare's preventive services:

-

Mammograms

Annually for women 40 and older. One baseline mammogram is covered between ages 35–39. -

Colonoscopies

Every 10 years for average-risk individuals. Every 24 months if you're considered high risk (family history of colon cancer or personal history of polyps). -

PSA Blood Test (Prostate)

Annually for men 50 and older. -

Low-Dose CT Lung Cancer Screening

Annually for adults ages 50–77 with a 20 pack-year smoking history who currently smoke or quit within the last 15 years. -

Pap Test & Pelvic Exam

Every 24 months. Every 12 months if you're considered high risk.

Which cancer screenings are free under Medicare?

Medicare covers several cancer screenings at no cost to you, as long as you meet the eligibility rules:• Breast cancer: Yearly mammogram

• Colorectal cancer: Colonoscopy, stool tests, and other screenings (frequency depends on type)

• Cervical & vaginal cancer: Pap test and pelvic exam every 2 years (or yearly if high-risk)

• Lung cancer: Annual low-dose CT scan for people who qualify

• Prostate cancer: PSA blood test (free) — the exam may have a small cost

• Skin cancer: Not a routine “screening,” but Medicare covers biopsies when a doctor sees something suspicious

These are all preventive benefits, so the screenings that qualify are $0 out of pocket.

The Coding Trap You Need to Know About

Here's where it gets tricky, and where licensed Medicare agents consistently warn beneficiaries to pay close attention. Every one of those screenings listed above is free only when your provider codes it as preventive. The moment a screening detects something and shifts from "routine check" to "diagnostic," your cost-sharing kicks in: you'll owe the Part B deductible ($283 in 2026) plus 20% coinsurance on whatever comes next.

As one agent on our platform puts it: "Make sure your doctor's office codes it correctly. Ask before the test is done. It's much easier to check codes before than change them after."

This is especially important if you have a prior diagnosis. For example, if you've previously been diagnosed with abnormal breast tissue, your future mammograms may no longer qualify as preventive. They'll be classified as diagnostic, which means cost-sharing applies. The same logic applies across all screenings: once there's a known condition, follow-up tests often fall into the diagnostic bucket.

Bottom line: Before any cancer screening, ask your provider how the procedure will be coded. If you believe a claim was coded incorrectly, you have the right to appeal a denied or incorrectly processed Medicare claim.

Does Medicare cover cancer screenings, and how often can I get them?

1. Colorectal Cancer ScreeningsFecal Occult Blood Test: Once every 12 months (age 50+)

Flexible Sigmoidoscopy: Every 4 years

Colonoscopy:

Every 10 years (or 4 years after a sigmoidoscopy)

Every 2 years if you're at high risk

Stool DNA test (e.g., Cologuard): Every 3 years (age 50–85, average risk)

2. Breast Cancer Screening (Mammogram)

Screening mammogram: Once every 12 months (for women age 40+)

Diagnostic mammogram: Covered as needed, with coinsurance

3. Cervical & Vaginal Cancer Screening

Pap test and pelvic exam: Every 2 years

Every 12 months if high-risk or had an abnormal Pap in the last 3 years

4. Lung Cancer Screening

Low-dose CT scan: Once per year if:

Age 50–77

History of smoking (20 pack-years)

Currently smoke or quit within the past 15 years

5. Prostate Cancer Screening (for men)

PSA (Prostate-Specific Antigen) blood test: Once every 12 months (age 50+)

Digital Rectal Exam: Covered, but you may pay part of the cost

No Cost If:

You meet age/risk criteria

You go to a provider that accepts Medicare assignment

High-Risk Status: More Frequent Screenings

If you have a family history of certain cancers, Medicare may cover more frequent screenings, but only if your provider properly documents your high-risk status. Licensed agents consistently highlight this point because it's where many beneficiaries miss out on coverage they're entitled to.

The most common example: a family history of colon cancer qualifies you as high risk, which means Medicare covers colonoscopies every 24 months instead of the standard 10-year interval. That's a significant difference in early detection capability.

The catch? Your provider must document the high-risk status in both the medical record and on the claim. If it's not documented, Medicare may apply the average-risk schedule, and you could end up paying out of pocket for a screening that should have been covered. According to agents on our platform, this documentation step is missed more often than you'd think.

I have a family history of colon cancer. Will Medicare cover more frequent colonoscopies for someone in my situation?

Yes — Medicare does consider family history of colon cancer when it comes to how often you can get a screening colonoscopy covered. If you’re at high risk because of a first-degree relative (parent, sibling, or child )with colon cancer, Medicare will cover a screening colonoscopy once every 2 years instead of the standard once every 10 years for average-risk people. However, it’s important that your provider documents the high-risk status in the medical record and on the claim — otherwise Medicare may apply the average-risk schedule. Also, if your doctor orders a colonoscopy because you have symptoms or other medical reasons other than just routine screening, Medicare may cover that as a diagnostic colonoscopy, which is paid differently than routine screening. Always talk with your provider and confirm that the high-risk screening code will be used, so Medicare processes it correctly.How Medicare Covers Chemotherapy and Cancer Treatment

When it comes to active cancer treatment (chemotherapy, radiation, surgery, and related care), Medicare provides strong coverage. But how it's covered depends on where you receive treatment, and that distinction matters for your wallet.

Part A: Inpatient Cancer Treatment

Medicare Part A covers cancer treatment when you're formally admitted as an inpatient to a hospital. This includes:

- Inpatient chemotherapy infusions

- Surgical procedures requiring hospital admission

- Inpatient radiation therapy

- Hospital room, meals, nursing care, and medications administered during your stay

Under Part A, you'll pay the inpatient deductible ($1,676 in 2026) for the first 60 days, with additional daily coinsurance kicking in after that.

Part B: Outpatient Cancer Treatment

Medicare Part B covers cancer treatment received on an outpatient basis: in a doctor's office, clinic, or outpatient infusion center. This is where the majority of chemotherapy is administered today, and it includes:

- IV chemotherapy infusions (specifically covered under Part B when outpatient)

- Radiation therapy

- Doctor visits and consultations

- Lab work and imaging (CT scans, PET scans, MRIs)

- Outpatient surgical procedures

After your Part B deductible ($283 in 2026), Medicare pays 80% and you're responsible for the remaining 20% coinsurance. Licensed agents consistently flag this as the number that catches people off guard — 20% of cancer treatment costs adds up fast.

To put it in perspective: a single round of chemotherapy can cost $10,000–$30,000 or more. At 20% coinsurance, you're looking at $2,000–$6,000 per round out of pocket, and most treatment plans involve multiple rounds over several months.

Does Medicare pay for IV chemotherapy?

Original Medicare covers medically necessary injectable and infusion chemotherapy medication if administered in a hospital setting and ordered by your healthcare provider as long as the drug is FDA approved for the condition you are being treated for. If you have a medicare advantage plan you will have a 20% copay. If you have a medigap supplement plan original medicare will cover the first 80% and your supplement plan will cover the remaining 20% once you have satisfied the annual deductible.Oral Chemotherapy and Part D

Chemotherapy drugs you take by mouth (oral chemo) are typically covered under Medicare Part D, your prescription drug plan. Coverage and costs vary depending on your specific Part D plan's formulary and tier structure. Some oral chemo drugs are classified as specialty medications, which often come with higher cost-sharing.

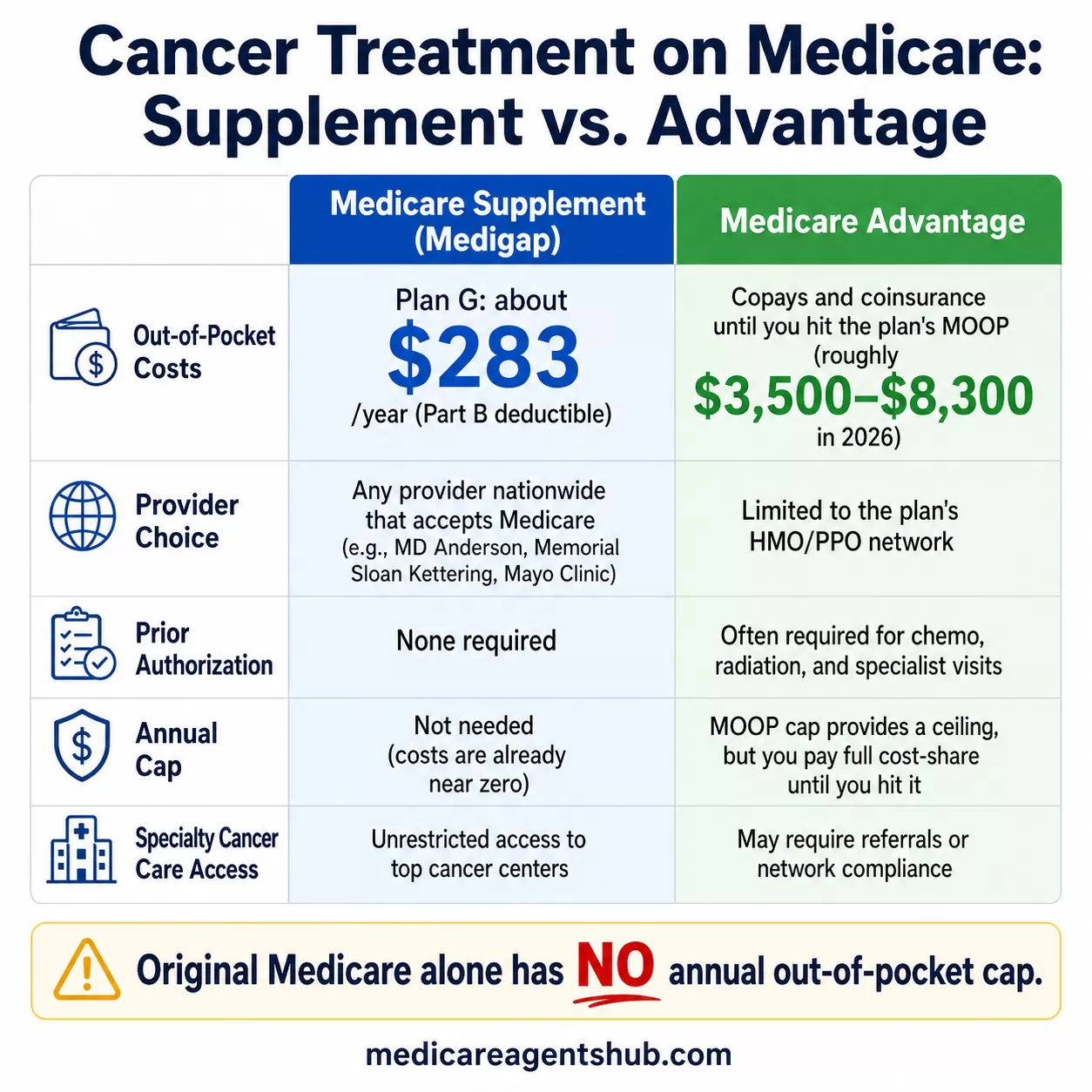

Supplement vs. Advantage: Why Your Plan Choice Matters Hugely for Cancer

This is arguably the most important section of this article, and it's the question licensed Medicare agents answer more than almost anything else when cancer enters the picture. The type of Medicare plan you have can fundamentally change your financial and logistical experience during cancer treatment.

Medicare Supplement (Medigap) Plans

With a Medigap/Supplement plan, you stay on Original Medicare. Medicare pays its 80%, and your supplement covers most or all of the remaining 20% (depending on your plan letter). The result:

- Minimal out-of-pocket costs: Plans like Plan G leave you responsible for only the Part B deductible ($283 in 2026). After that, your costs are essentially zero for Medicare-approved services.

- No network restrictions: You can go to any hospital, oncologist, or cancer center in the country that accepts Medicare. MD Anderson, Memorial Sloan Kettering, Mayo Clinic. Your choice.

- No prior authorizations: Your doctor orders treatment, and it's covered. No waiting for plan approval.

- No referral requirements: You can see any specialist without a gatekeeper.

As agents on our platform consistently advise: supplement plans give you the most flexibility when you need it most. When you're dealing with a cancer diagnosis, the ability to walk into any cancer center in the country without worrying about networks or authorizations is a major advantage.

Medicare Advantage Plans

With a Medicare Advantage plan, your costs work differently:

- Copays and coinsurance apply for each service (office visits, infusions, scans, hospital stays), and they vary by plan.

- Network restrictions: Most Advantage plans use HMO or PPO networks. Going out-of-network (if even allowed) usually means higher costs.

- Prior authorizations: Many Advantage plans require pre-approval for certain treatments, which can introduce delays.

- Maximum Out-of-Pocket (MOOP) cap: This is the silver lining. Once you hit your plan's annual MOOP limit, the plan covers 100% for the rest of the year. Several brokers note that active cancer treatment is "the quickest way to hit your MOOP."

The MOOP cap is a genuine advantage. For 2026, in-network MOOPs can range from roughly $3,500 to $8,300 depending on the plan. Once you hit that ceiling, you're done paying for the year. With Original Medicare alone (no supplement), there is no annual out-of-pocket cap, so costs can theoretically keep climbing.

However, agents consistently point out the trade-offs: network restrictions can limit your choice of oncologists and cancer centers. Prior authorization requirements can delay the start of treatment. And if you're on a plan with a $7,500 MOOP, you're paying that full amount before the cap kicks in, which is significantly more than the $283 a Plan G supplement holder pays all year.

- Out-of-Pocket Costs: Supplement: minimal (Plan G = $283/year). Advantage: copays/coinsurance up to the MOOP cap.

- Provider Choice: Supplement: any provider that accepts Medicare, nationwide. Advantage: plan network (HMO/PPO), with out-of-network penalties or restrictions.

- Prior Authorization: Supplement: none required. Advantage: often required for chemo, radiation, and specialist visits.

- Annual Cap: Supplement: no cap needed (costs are already near-zero). Advantage: MOOP cap provides a ceiling.

- Flexibility for Specialty Care: Supplement: unrestricted access to top cancer centers. Advantage: may require referrals or network compliance.

For more on managing Medicare with chronic or serious health conditions, including how plan choice affects ongoing treatment, we have a dedicated guide.

Clinical Trial Coverage Under Medicare

If your oncologist recommends a clinical trial, understanding what Medicare will and won't cover is critical. The good news: Medicare has a specific policy for clinical trial coverage, and it's more generous than many people realize.

What Medicare covers ("routine costs"):

- Doctor visits and consultations related to the trial

- Lab work and blood tests

- Imaging and scans (CT, PET, MRI)

- Hospital stays related to the trial

- Standard-of-care treatments that would be covered regardless of the trial

- Monitoring for side effects and complications

What Medicare does NOT cover:

- The experimental drug or treatment itself (typically covered by the trial's sponsor, the pharmaceutical company or research institution running the study)

- Items or services provided solely for data collection purposes

- The investigational device or item being studied

An important note for supplement holders: Medigap policies are required to cover the same routine clinical trial costs that Medicare covers. This means your supplement continues working the way it always does, covering your coinsurance and deductibles for all those routine costs. Combined with the freedom to go to any clinical trial site nationwide, this gives supplement holders the most flexibility when pursuing cutting-edge treatments.

Medicare Advantage plans must also cover clinical trial routine costs, but you may face network restrictions or different cost-sharing structures depending on where the trial is being conducted. Clinical trials are just one of many advanced technologies and treatments Medicare may already cover.

I'm participating in a clinical trial for a new cancer treatment that uses personalized medicine based on my genetic profile. How does Medicare coverage work in this situation?

Medicare actually does cover many clinical trials, and it’s important to understand how the coverage works. In many qualifying trials, Medicare will pay for the routine care costs you would normally receive, things like doctor visits, hospital services, labs, and imaging. The experimental treatment itself is usually covered by the sponsor of the study.Before you sign up, you'll want to make sure your specific trial is Medicare approved, and know which parts Medicare covers versus which parts the study covers. You'll also want other make sure that your Medicare plan gives you access to the doctors and facilities running the trial, since certain plans have networks that might limit you.

Beneficiaries with a Medicare Supplement plan will have the most flexibility, since they can typically see any doctor who accepts Medicare or go to any hospital.

Genetic Testing for Cancer Risk: What Medicare Covers (and Doesn't)

Genetic testing has become an increasingly important tool in cancer prevention and treatment planning. But Medicare's coverage for genetic testing is more limited than many people expect, and licensed agents regularly warn beneficiaries to understand the rules before assuming they're covered.

The key principle: Medicare does not cover genetic testing done out of curiosity, for general wellness screening, or "just because." Coverage requires medical necessity, typically a personal history of cancer or strong clinical indicators.

BRCA1/BRCA2 Testing (Breast/Ovarian Cancer Genes)

Medicare may cover BRCA testing when specific criteria are met:

- Personal history of breast cancer diagnosed before age 60

- Personal history of ovarian cancer

- Strong family history pattern (multiple first-degree relatives with breast/ovarian cancer)

- Ashkenazi Jewish descent with a family history of breast or ovarian cancer

Family history alone is usually not enough. This is a common misconception. Having a mother or sister with breast cancer doesn't automatically qualify you for BRCA testing under Medicare. There typically needs to be either a personal cancer history or a very specific pattern of family history that meets clinical guidelines.

Lynch Syndrome Testing

Testing for Lynch syndrome (hereditary colorectal cancer predisposition) may be covered when clinical criteria are met, such as a personal history of colorectal cancer with specific tumor characteristics.

A Warning from Agents: Health Fair Genetic Testing

Multiple agents on our platform specifically warn about companies that offer genetic testing at health fairs, community events, or through unsolicited phone calls. As one agent puts it: "Beware of offers to run these types of tests at health fairs." These often result in surprise bills, unnecessary testing, or even fraud. If genetic testing is medically appropriate for you, it should be ordered by your doctor as part of a clinical evaluation — not pitched to you at a folding table in a convention center.

I'm considering genetic testing to assess my cancer risk based on family history. Will Medicare cover this preventive approach in my situation?

Generally, Medicare does not cover this type of testing for people without a personal history of cancer or signs of a genetic mutation, as it considers it a preventive service rather than a diagnostic one in that context.To be covered, the test must be ordered by a physician, and the specific requirements can vary depending on your region and the type of test.

Medicare may cover genetic testing when you have a personal history of cancer or, Medicare may cover testing if you have been diagnosed with cancer and meet certain personal or family history criteria.

Medicare may cover this if there is a known mutation in the family: It may cover testing for an individual with signs or symptoms of an inheritable cancer who has a family history of a known mutation.

A healthcare provider must determine the test is medically necessary for your situation.

Specific types of tests: Some tests, like those for BRCA1/2 genes, have specific criteria for coverage, often requiring a personal history of certain cancers or specific family history details,

Radiation Therapy Coverage

Radiation therapy, including external beam radiation, brachytherapy, and proton beam therapy, is covered under Medicare. Like chemotherapy, the coverage breakdown depends on the setting:

- Outpatient radiation (the most common setting): Covered under Part B. After your $283 deductible, Medicare pays 80%, you pay 20% coinsurance.

- Inpatient radiation (administered during a hospital stay): Covered under Part A with the inpatient deductible and coinsurance schedule.

The same supplement vs. advantage dynamics apply here. With a supplement, your 20% coinsurance is largely or entirely covered. With an Advantage plan, you'll pay plan-specific copays or coinsurance up to your MOOP.

Medical Marijuana and Cancer: Not Covered

This comes up frequently, especially from beneficiaries dealing with cancer-related pain, nausea, or appetite loss. The short answer: no part of Medicare covers medical marijuana, regardless of your state's laws. Marijuana remains classified as a federal Schedule I substance, and Medicare is a federal program.

However, there's a narrow exception worth knowing: FDA-approved cannabinoid-based medications (such as certain anti-nausea drugs prescribed during chemotherapy) may be covered under your Part D prescription drug plan. These are pharmaceutical products that have gone through the FDA approval process, not dispensary marijuana.

Putting It All Together: Action Steps for Medicare Beneficiaries

Whether you're dealing with a current diagnosis or thinking ahead about how your Medicare coverage handles cancer, here's what licensed agents consistently recommend:

- Stay current on your preventive screenings. They're free when coded correctly, and early detection saves lives and money.

- Ask about coding before any screening. Confirm with your provider's office that the procedure will be coded as preventive. It's a 30-second conversation that can save you hundreds of dollars.

- Document your risk factors. If you have a family history of cancer, make sure it's in your medical records and that your provider references it on claims for more frequent screenings.

- Understand your plan's cancer cost exposure. If you're on a supplement, your costs are predictable and minimal. If you're on an Advantage plan, know your MOOP and understand what prior authorizations might be required.

- Review your plan annually. If your health situation has changed, especially with a cancer diagnosis, it may be worth reassessing whether your current plan type is the best fit. Talk to a licensed Medicare agent about your specific situation.

- Be cautious with genetic testing offers. Only pursue genetic testing through your doctor when there's a clinical reason, not through unsolicited offers or health fair booths.

- Know your clinical trial rights. If a clinical trial is recommended, Medicare covers the routine costs. Don't let cost fears alone keep you from considering cutting-edge treatment options.

Cancer is one of those situations where your Medicare choices are put to the ultimate test. The agents on our platform, hundreds of whom have walked beneficiaries through this exact scenario, overwhelmingly agree on one thing: understanding your coverage before you need it is the single best thing you can do. Whether you're on a supplement or an Advantage plan, knowing what to expect means fewer surprises and more time to focus on what actually matters — your health and recovery.