Screening vs. Diagnostic Medicare Billing: Why a $0 Mammogram Can Become a Surprise Bill

-

March 11, 2026

- Screening tests are coded as preventive and often cost $0 when the provider accepts assignment

- Diagnostic tests are ordered because of symptoms, abnormal results, or follow-up monitoring

- Diagnostic cost-sharing: the $283 annual deductible (2026) plus 20% of the Medicare-approved amount

- The difference between a $0 bill and a $300+ bill is often a single billing code

You scheduled a mammogram. Medicare covered it at $0. A year later you went back for the same test at the same facility, and this time you got a bill for over $300. Nothing about the procedure changed. What changed was a single billing code.

This is one of the most common and least understood billing surprises in Medicare. Preventive screenings are covered at no cost under Medicare Part B, but only when they're coded as screening procedures. The moment a doctor flags a prior abnormality or orders the test to investigate a symptom, that same procedure gets recoded as diagnostic, and the entire cost structure shifts.

What "Screening" vs. "Diagnostic" Actually Means on a Claim

| Test Type | Why It Is Ordered | Typical Medicare Cost |

|---|---|---|

| Screening | Routine check before symptoms appear | Often $0 if frequency rules are met and the provider accepts assignment |

| Diagnostic | Follow-up, symptoms, abnormal result, or monitoring | Part B deductible ($283 in 2026) plus 20% coinsurance may apply |

Every medical procedure submitted to Medicare carries a billing code. For common tests like mammograms, colonoscopies, and blood panels, there are separate codes for screening (preventive) and diagnostic (investigative) versions of the same procedure.

When a test is coded as a screening, Medicare treats it as preventive care. You pay nothing, as long as your provider accepts Medicare assignment and you meet the frequency rules (for example, one screening mammogram every 12 months for women 40 and older).

When that same test is coded as diagnostic, it falls under standard Part B cost-sharing. In 2026, that means you're responsible for the $283 annual Part B deductible plus 20% of the Medicare-approved amount.

On a mammogram that Medicare approves at $250, that's $50 in coinsurance on top of the deductible if you haven't met it yet.

How does Medicare Part B handle coverage for preventative screenings like mammograms?

Medicare Part B covers preventive screenings like mammograms as part of its focus on early detection and health maintenance, with specific rules on frequency, cost, and eligibility. Here’s how it works:Screening Mammograms: These are covered for women aged 40 and older to detect breast cancer early, before symptoms appear.

Frequency: Part B fully covers one screening mammogram every 12 months (anytime after 11 months from your last one). If you’re new to Medicare, you also get a baseline mammogram covered between ages 35–39.

Cost: There’s no out-of-pocket cost—no coinsurance, copayment, or Part B deductible—as long as the provider accepts Medicare assignment (agrees to Medicare’s payment rates). This applies to 2D and 3D (tomosynthesis) screenings, though 3D coverage was clarified in updates around 2018 to match evolving standards.

Diagnostic Mammograms: If a screening finds something abnormal or you have symptoms (like a lump), Part B covers diagnostic mammograms to investigate further.

Frequency: No strict limit—covered as medically necessary, which could mean multiple in a year if your doctor orders them.

Cost: After meeting the Part B deductible ($240 in 2025), you pay 20% of the Medicare-approved amount. There’s no cap on how many are covered, but each one triggers that 20% coinsurance unless you have a Medigap plan to offset it.

Key Details: The mammogram must be done at a Medicare-approved facility (like a radiology center or hospital outpatient department). If it’s bundled with other services (e.g., a biopsy), additional costs might apply under Part B’s standard rules. Preventive coverage assumes you’re symptom-free—once it’s diagnostic, it shifts to a treatment framework.

This setup reflects Part B’s broader approach to preventive care: full coverage for annual screenings to catch issues early, with cost-sharing kicking in when it’s about diagnosis or follow-up. It’s a balance between encouraging checkups and managing expenses when care escalates.

Editor's note: The Part B deductible changes each year. For 2026, the Part B deductible is $283.

The A1c Trap: How One Reading Can Change Future Tests

The screening-to-diagnostic switch doesn't just apply to the test that finds something wrong. In many cases, it reclassifies future tests for that condition as diagnostic rather than preventive.

Barbara Barnes, a Certified Medicare Insurance Planner in Pennsylvania, sees this play out with her clients regularly: "As long as your A1c is normal, future tests to make sure that you haven't developed diabetes should be coded as 'preventative.' But as soon as you have a reading that indicates diabetes or even pre-diabetes, future tests will be diagnostic."

That's the part most people miss. A single borderline A1c reading doesn't just cost you money on that visit. In many cases, future monitoring for that same condition may be coded as diagnostic rather than preventive.

The same principle applies to mammograms: Barnes notes that "if you've had a prior diagnosis of abnormal breast tissue, future mammograms that are performed to keep an eye on that issue will no longer be 'preventative' but rather 'diagnostic' in nature."

This creates a compounding cost problem. A screening mammogram every 12 months costs $0. A diagnostic mammogram every 12 months, after the Part B deductible, costs roughly $50 each year. Over a decade, that's $500 in coinsurance alone on a test that used to be free.

While cost is important, please do not skip a medically necessary diagnostic test because of the potential bill. Early detection remains your best path to long-term health. A licensed Medicare agent can help you find supplemental coverage that reduces or eliminates these out-of-pocket costs.

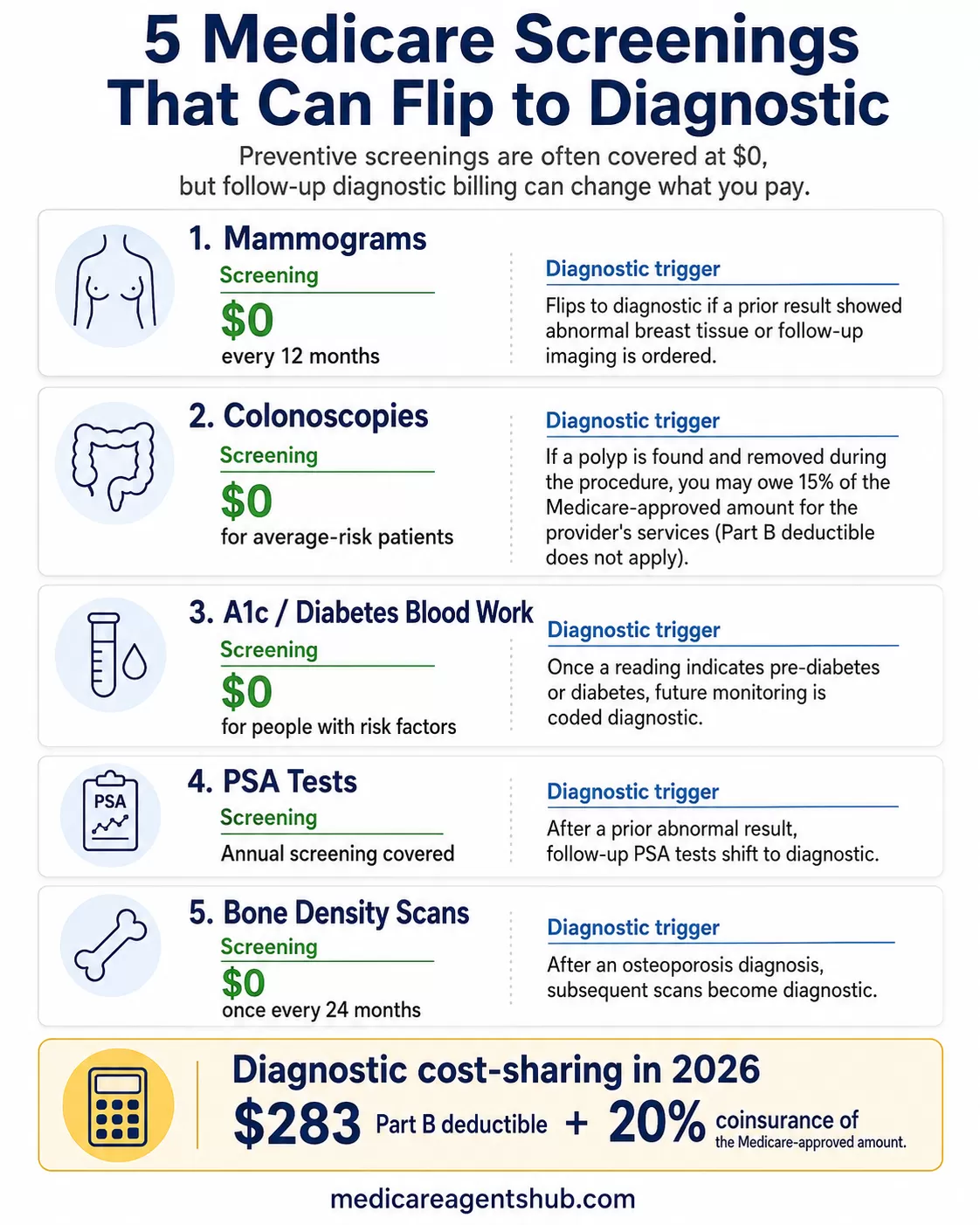

Common Tests That Can Flip From Free to Billable

The screening-to-diagnostic reclassification can happen with nearly any preventive service Medicare covers. But some tests are more common triggers than others:

- Mammograms: A screening mammogram is free once every 12 months. If it finds something, the follow-up mammogram (even if it's the exact same imaging) is diagnostic. If prior results showed abnormal tissue, future mammograms may be coded diagnostic from the start.

- Colonoscopies: A screening colonoscopy is free for average-risk patients. But if a polyp or other tissue is found and removed during the procedure, Medicare may still leave you with cost-sharing. According to Medicare's 2026 benefits guide, you may pay 15% of the Medicare-approved amount for the provider's services in this situation, and the Part B deductible does not apply. That's different from the standard 20% coinsurance on most diagnostic services, but it can still result in an unexpected bill if you weren't prepared for it.

- A1c and diabetes blood work: Free as a screening for people with risk factors. Once a reading comes back elevated, future monitoring is diagnostic.

- PSA tests: Annual screening is covered. If a prior result was abnormal, follow-up PSA tests shift to diagnostic.

- Bone density scans: Covered once every 24 months as a screening. After an osteoporosis diagnosis, subsequent scans become diagnostic.

The pattern is the same every time: Medicare pays 100% for the test that finds nothing, and shifts cost-sharing to you the moment results indicate a problem worth monitoring. For a full list of what's covered, see Medicare's preventive and screening services page.

How does Medicare Part B handle coverage for preventative screenings like mammograms?

Screening & Baseline Mammograms: Covered as preventive services. If you use a provider or facility that accepts Medicare assignment, you pay $0.Diagnostic Mammograms: Covered when medically necessary. After you meet your Part B deductible, you pay 20% of the Medicare-approved amount.

A baseline Mammogram is covered once in your lifetime, usually between the ages of 35-39. Screenings are covered once annually. Diagnostic mammograms can be covered more than once a year if medically neccessary.

Your doctor may recommend other services like 3-D imaging that Medicare does not cover. This could end up in additional costs for you. Make sure to ask your doctor about the reasons for these recommendations and what Medicare will actually cover.

The "Talk to the Coder" Script: What to Say Before Your Appointment

Medicare billing depends on the provider, facility, diagnosis, CPT/HCPCS codes, plan type, and whether the provider accepts assignment. This article is educational and should not replace advice from Medicare, your provider's billing office, or your plan.

Barnes offers a piece of advice that most Medicare beneficiaries never think of: "It's much easier to check the codes before the test is done than it is to have them changed afterwards. Busy doctors can easily make errors in this type of order, so asking them before they write the order is a good idea."

Here's what that looks like in practice. Before your appointment, call the doctor's office and ask:

- "Is this being ordered as a screening or a diagnostic procedure?" If you're going in for a routine mammogram and have no current symptoms, it should be a screening. If the office is coding it diagnostic based on something from years ago, ask whether a screening code is appropriate.

- "What billing code will be submitted to Medicare?" You don't need to memorize CPT codes, but knowing whether a code starts with a preventive or diagnostic classification gives you something concrete to reference if a surprise bill shows up later.

- "If something is found during the screening, will the coding change for this visit?" This is especially important for colonoscopies, where a polyp removal mid-procedure can retroactively reclassify the entire visit.

Pro tip: If the front desk staff can't answer your billing questions, ask to speak with the office's Insurance Coordinator or Billing Specialist. These are the people who actually work with procedure codes and Medicare claims daily, and they'll be able to give you a clear answer about how your test will be coded.

This isn't about arguing with your doctor. It's about catching coding errors before they become billing problems. Medical coders handle hundreds of claims, and a test that should be preventive can easily get flagged as diagnostic if the patient's chart shows a prior finding.

What You Actually Owe When a Test Flips to Diagnostic

"Screenings are covered at no cost under Medicare Part B," says Charles Calvin, a licensed Medicare agent in Missouri. "Further diagnostics, such as if results are abnormal and require additional testing, are then billed at the current deductible rate ($283/yr for '26) and/or 20% of contracted cost."

Under Original Medicare Part B, diagnostic tests follow standard cost-sharing rules:

- Part B deductible: $283 in 2026. You pay this once per year before Medicare starts covering its share of outpatient services.

- Coinsurance: After the deductible, you pay 20% of the Medicare-approved amount. Medicare pays the other 80%.

- No annual cap: Original Medicare has no out-of-pocket maximum, so the 20% coinsurance applies to every diagnostic service with no ceiling.

For a single diagnostic mammogram, the math might look like this:

- Deductible not yet met: Medicare-approved amount of $250, minus $283 deductible = Medicare pays $0, you pay $250 out of the approved amount.

- Deductible already met: You pay $50 (20% of $250) and Medicare pays $200.

This is one of the hidden costs that catch first-time enrollees off guard.

How Medigap and Medicare Advantage Handle the Gap Differently

This is where your choice of supplemental coverage makes a real difference.

Medigap (Medicare Supplement): If you have a Medigap plan like Plan G, the diagnostic reclassification barely matters financially. Plan G covers the 20% Part B coinsurance and the Part B excess charges.

You'd still owe the Part B deductible ($283 in 2026), but after that, your diagnostic mammogram, blood work, and follow-up tests cost you nothing out of pocket. That deductible is a known, fixed annual cost rather than an unpredictable bill.

Medicare Advantage: MA plans handle diagnostic tests through copays and coinsurance defined in each plan's benefit structure. A diagnostic mammogram might cost a $0-$50 copay on one plan and $75 on another.

The key difference from Original Medicare is the out-of-pocket maximum. In 2026, MA plans are capped at $9,350 nationally, though most plans set their limit between $3,000 and $5,000. That ceiling means diagnostic costs can't spiral indefinitely.

The tradeoff: Medigap premiums are higher month to month, but you'll never see a surprise diagnostic bill beyond the annual deductible. MA premiums are often lower (sometimes $0), but each diagnostic test carries a copay that can add up if you're managing multiple conditions. Understanding how these two paths compare is essential when diagnostic costs are part of the equation.

What to Do If You Get a Surprise Diagnostic Bill

If you receive a bill for a test you expected to be free, don't pay it without checking these three things first:

- Review the Explanation of Benefits (EOB). Medicare sends an EOB after every claim is processed. Look at the procedure code and the "type of service" description. If it says diagnostic and you believe the test was routine/preventive, that's your starting point for a correction.

- Call the provider's billing office. Ask whether the test was coded correctly. Coding errors are common, especially when a patient has a history of a condition but the current test was genuinely routine. The billing office can submit a corrected claim to Medicare with an updated code.

- File an appeal if needed. If the provider insists the coding is correct but you believe the test was preventive, you have the right to appeal the coverage decision. Medicare's appeals process has five levels, and many coding disputes are resolved at the first level (a redetermination by the Medicare Administrative Contractor).

Time matters. You have 120 days from the date you receive the Medicare Summary Notice to file a redetermination request. Don't sit on a bill you think is wrong.

If you already received a bill: Gather your Medicare Summary Notice, the provider bill, and the procedure code before calling the billing office. Having these documents ready makes the conversation faster and gives you specific details to reference.

Frequently Asked Questions

Why was my Medicare mammogram not free?

Your mammogram was likely coded as diagnostic rather than screening. This happens when a doctor orders the test because of symptoms, a prior abnormal result, or follow-up monitoring. Diagnostic mammograms fall under standard Part B cost-sharing: the $283 deductible (2026) plus 20% coinsurance.

What is the difference between a screening and diagnostic mammogram?

A screening mammogram is a routine check for women with no current symptoms or concerns. A diagnostic mammogram is ordered to investigate something specific, such as a lump, pain, or a prior abnormal finding. The imaging may be identical, but the billing code and your out-of-pocket cost are different.

Does Medicare cover diagnostic mammograms?

Yes. Medicare Part B covers diagnostic mammograms when they are medically necessary. However, unlike screening mammograms (which are $0), diagnostic mammograms are subject to the Part B deductible and 20% coinsurance.

Can a provider change a diagnostic code to a screening code?

If the test was genuinely preventive and was miscoded, yes. Contact the provider's billing office and ask them to review the claim. They can submit a corrected claim to Medicare with an updated procedure code. This is more common than most people realize.

What should I ask before a Medicare screening test?

Ask three things: (1) Is this being ordered as screening or diagnostic? (2) What billing code will be submitted? (3) If something is found during the test, will the code change for this visit? Getting answers upfront is much easier than disputing a bill after the fact.

The Bigger Picture: Why This Billing Split Exists

Medicare's logic is straightforward, even if the results feel unfair. Preventive screenings are designed to catch problems before they start. Once a problem is identified, monitoring it is considered treatment, and treatment has cost-sharing.

The system incentivizes early detection by making the first look free, then shifts financial responsibility to the patient (and their supplemental coverage) once care moves from prevention to management.

Understanding that logic won't make a surprise bill less frustrating. But it does give you the information to plan ahead: ask about codes before tests, choose supplemental coverage that accounts for diagnostic costs, and challenge bills that don't match what actually happened in the exam room. A local Medicare agent can help you evaluate whether your current coverage adequately protects you from diagnostic cost-sharing, or whether a different plan structure would save you money in the long run.