What Medicare Agents Would Change About Their Industry — and What CMS Already Changed

-

July 1, 2026

Ask a room full of Medicare agents what they would change about the industry and the compliance-manual answers stop coming pretty quickly. What you get instead is a working policy wishlist: specific rules that agents say hurt the sale, hurt the client, or both. Not the "more oversight" talking points you see in trade press. Real friction points, in the agents' own words.

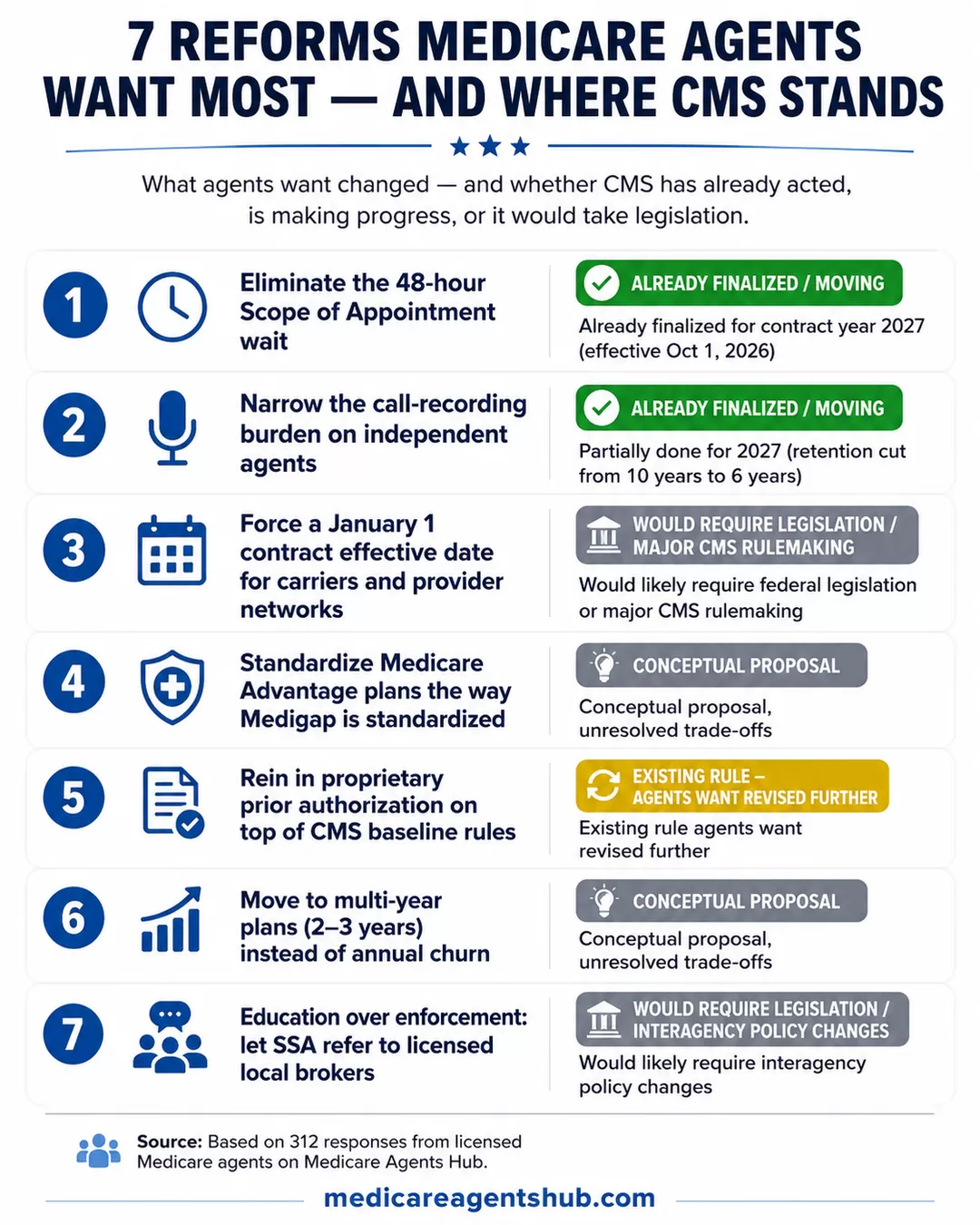

Some of these proposals would require legislation or major structural changes. Others are already moving. CMS's elimination of the 48-hour Scope of Appointment (SoA) wait for contract year 2027 shows that sustained feedback from agents and other stakeholders can influence the annual rulemaking process.

1. CMS Has Already Eliminated the 48-Hour SoA Wait for 2027

Status: Already finalized for contract year 2027

Agents identified the 48-hour Scope of Appointment waiting period as one of their most persistent compliance frustrations, and CMS has now acted on it. Beneficiary-initiated walk-ins were already exempt from the previous waiting period. Beginning October 1, 2026, CMS will eliminate the 48-hour delay for all personal marketing appointments. Agents must still document the agreed-upon scope before the appointment, and an in-person SoA must be in writing.

Agents describe the same scenario over and over: a senior calls, or shows up, ready to enroll. Under the outgoing rule, the agent had to explain that federal marketing rules required a two-day waiting period on the very meeting the senior just asked for. Some walked out. Some went home and took a phone call from a TV-ad call center that hour. The rule that was written to protect them was, in agents' view, pushing them toward less accountable channels.

What's a Medicare rule or regulation that's outdated or unfair to seniors?

I think it’s outdated and unfair to seniors that they have to do a Scope of Appointment at least 48 hours before a meeting they are requesting. What difference does it make?This was the most frequently cited compliance frustration in the answer set. No respondent defended the 48-hour window as effective consumer protection. The fact that CMS moved to eliminate it validates what agents have been saying for years: the delay created friction without meaningfully reducing pressure tactics.

2. Narrow the Call-Recording Burden on Independent Agents

Status: Existing rule agents want revised further (CMS has already narrowed scope for 2027)

CMS does not require recording of in-person interactions. The recording requirement applies to telephone and virtual calls that touch Medicare Advantage or Part D marketing. But agents say the rule, written for high-volume outbound telemarketing operations, lands disproportionately on small local practices where the client has known the agent for a decade.

CMS has already narrowed the requirement for contract year 2027. Beginning October 1, 2026, recording applies specifically to marketing and sales calls, including the audio portion of web-based calls, with a minimum retention period of six years (down from the previous ten-year requirement).

What's a Medicare rule or regulation that's outdated or unfair to seniors?

The 3-day hospital stay to have skilled nursing covered by Medicare and your Medicare Supplement. If you have Medicare Advantage, there's no 3-day rule thankfully.The silly marketing rules for agents... like the Scope of Appointment and call recorded line. Both are childish and don't stop the bad agents. They only make it harder and less efficient for the good agents and Medicare beneficiaries.

I hope that helps.

Chris

Several answers pointed out the enforcement gap directly. The agents who are cutting corners are not the ones getting caught by the recording requirement; they simply don't record. The compliant agents record everything and absorb the cost. Agents put this in the same "compliance theater" category as some of the transparency rules that get headline attention but change little at the point of sale.

3. Force a January 1 Contract Effective Date for Carriers and Provider Networks

Status: Would likely require federal legislation or major CMS rulemaking

This one is not about repealing a rule. It is about writing one that does not exist yet. Right now a Medicare Advantage carrier and a hospital system can renegotiate their network contract in the middle of the plan year. If they fail to agree, the hospital drops out of network in April. The beneficiary picked the plan in October based on a network that no longer exists in the spring.

Agents want CMS to require that carrier-provider contracts be locked in for a full calendar year alongside the plan year. Same effective date. Same expiration. If a hospital wants out, it exits at year end, not in the middle of treatment.

What's a Medicare rule or regulation that's outdated or unfair to seniors?

I wouldn't call it a rule or regulation that is outdated. I would call it one that does not exist. Medicare needs to REQUIRE the insurance companies and doctors/facilities to sign network contracts with a January 1 effective date. This way the beneficiary would be certain that they will not lose their doctor part way through the year. It is not fair to seniors to pick a plan in the Fall, have plan start on January 1, only to be told part way through the year that their doctors or local hospital will no longer be in network. This does not open a special election period to change plans and forces the patient to find care from a different in-network provider.Editor's note: A provider departure does not automatically create a Special Enrollment Period (SEP). However, CMS may grant one when it determines that a network change is significant, and it may also make case-by-case determinations. Some circumstances can also bring Medigap guaranteed-issue rights.

This is one of the few reforms in the answer set that would help clients without touching commission or plan design at all. It is also directly related to the ongoing MA disenrollment wave agents have been watching build. Every mid-year hospital drop generates the same phone call: my doctor just went out of network, what do I do? Agents want the structural fix, not another script.

4. Standardize Medicare Advantage Plans the Way Medigap Is Standardized

Status: Conceptual proposal with unresolved trade-offs

Medigap plans are standardized by letter. A Plan G in Ohio pays for the same things a Plan G in Arizona pays for. (Massachusetts, Minnesota, and Wisconsin standardize Medigap differently under state-specific frameworks.) That standardization is the reason a senior can shop by price and rating and be confident the coverage will hold up.

Medicare Advantage is the opposite. Every carrier designs its own benefits, its own network, its own drug tiering, its own out-of-pocket structure. Two "$0 premium HMO" plans on the same city block can pay drastically different amounts for the same knee replacement. Agents in the answer set say this is not competition but confusion, and they want CMS to standardize the benefit shells the same way Medigap is standardized.

If you could change one thing about the Medicare system, what would it be and why?

Medicare advantage. I would require all Medicare, advantage plans to be standardized, just like Medicare, supplements are standardized. It makes it very difficult for these seniors to figure out which plan is going to be best when all the plans get to be different. Based on whatever the company wants to choose.Nobody in the answer set was under the illusion that carriers would welcome this. The MA product line lives on differentiation. But the agents pushing for it argue that the shopping experience is currently unworkable for a self-directed senior, and that a standardized shell would push the competition to premium, network, and service, which is where they say it belongs.

5. Rein In Proprietary Prior Authorization

Status: Existing rule agents want revised (CMS has placed guardrails; agents want more)

CMS has prior authorization guidelines. Current rules require Medicare Advantage plans to follow fully established Traditional Medicare criteria found in statutes, regulations, National Coverage Determinations (NCDs), and Local Coverage Determinations (LCDs). Plans may develop internal criteria only when Medicare's coverage criteria are not fully established, and those internal criteria must be publicly accessible and supported by current evidence.

CMS also permits algorithms to assist with coverage decisions, but an algorithm or AI tool cannot be the sole basis for denying an inpatient admission or terminating post-acute care without consideration of the individual patient's circumstances.

What agents say is happening in practice is different from what CMS permits on paper. Agents describe a second layer of proprietary prior authorization criteria that generates denials, delays, and appeals fights beyond what baseline CMS rules would produce.

Two specific asks show up repeatedly. First, prohibit carriers from adding proprietary auth requirements on top of CMS baseline rules for services CMS has already cleared. Second, put stronger guardrails on the use of AI in the auth-approval process itself, which some agents flag as a source of unreviewed batch denials.

If you could change one thing about the Medicare system, what would it be and why?

I would like to see an open enrollment period for Medicare Supplements in all states. I would prohibit Medicare Advantage plans from using PROPRIETARY prior authorization. They use this in addition to Medicare's prior authorization guidelines. Why? I would prohibit the use of AI in the prior authorization process that some Medicare Advantage plans use. I would like to see some coverage for custodial long-term care.This is where agent frustration overlaps most directly with client harm. A senior who was told at enrollment their surgery would be covered gets a denial three months in because the carrier's internal criteria did not match the CMS coverage determination. The agent then spends unpaid hours running the appeal. Agents want the second layer of friction removed, not made more transparent.

6. Move to Multi-Year Plans Instead of Annual Churn

Status: Conceptual proposal with unresolved trade-offs

Not every reform in the answer set is about compliance. Some are about product design. One of the more interesting ones is the push to end the annual plan cycle entirely and move to a 2-year or 3-year commitment structure.

The reasoning: by the time a senior actually understands the plan they enrolled in last October, it is already October again and everything has changed. The Annual Notice of Change (ANOC) lands, the formulary shifts, the network drops a system, the maximum out-of-pocket (MOOP) moves. The client has never once experienced a stable plan year long enough to know if it worked.

If you could change one thing about the Medicare system, what would it be and why?

To not change plans annually and instead maybe do 2-3 years. The annual changes occur too quickly and just when beneficiaries grasp an understanding the plan changes or can change.Multi-year plans would slow the annual churn, cut down on the Annual Enrollment Period (AEP) marketing blitz, and give agents a real book of business to service instead of a rebuild every fall. It would also reduce the Open Enrollment Period (OEP) switch activity that has grown up around plans that were mis-sold in the first place. The trade-off agents openly acknowledge: locking clients in for multiple years cuts against the very re-shop windows that exist to protect them. That tension is real and unresolved in the answer set.

7. Education Over Enforcement: Let SSA Refer, and Fund Real Consumer Education

Status: Would likely require interagency policy changes

The final theme is less a rule change and more an operating philosophy shift. Agents want CMS and the Social Security Administration (SSA) to spend less on enforcement and more on genuine consumer education. That includes letting Social Security field offices refer beneficiaries to licensed local brokers. SSA officially directs people to Medicare.gov for Part C and Part D plan comparisons, while Medicare.gov prominently offers State Health Insurance Assistance Program (SHIP) counseling. Agents say the practical result is that beneficiaries leave SSA offices without a clear next step.

If you could change one thing about the Medicare system, what would it be and why?

I believe Medicare could improve their engagement with the Senior Market by first of all making sure that Social Security Offices refrain from giving advise about Medicare other than "You should talk to a licensed and certified Medicare agent in your area about the options you have.Then they could also regulate the call centers to insure their compliance with non-pressured, non-biased presentations that simply allow the educational process to allow the senior market to make an informed decision about their Medicare Options.

The agents pushing this angle argue that consumer confusion is the root cause of most of the enforcement problems CMS is trying to solve. If the beneficiary understood the difference between Original Medicare, Medigap, and Medicare Advantage before they picked up a call from a TV ad, the bad-actor problem shrinks. As long as SSA can only vaguely gesture toward "go find help," the vacuum will get filled by whoever markets loudest.

What's one piece of advice you wish every senior knew before picking a Medicare plan?

Seniors! You should begin planning and getting educated on Medicare six months in advance of your 65th birthday. All seniors need to understand the difference between Medicare Advantage Plans and Medicare Supplement plans. Getting educated about Original Medicare (Part A, B and D), Medicare Advantage Plans (Part C) and Medicare Supplements will ensure each senior makes the best decision for them- this is a very individual decision that is dependent on the area you live in, and your financial and physical health. Additionally, all seniors need to know that they need to be eligible and enrolled in Original Medicare Part A and B in order to enroll in a Medicare Advantage or Medicare Supplement Plan. This needs to be completed timely through the Social Security Administration to avoid penalties on premiums or a gap in coverage. This is something that several seniors I work with are not aware of, since a growing number of seniors are working beyond their 65th birthday. Seniors working beyond 65 are generally covered by an Employer Group Health Plan and may not understand how their EGHP interacts with Medicare once they reach 65, when to enroll in Original Medicare, or what documentation to show to avoid unnecessary penalties on premiums.This ties directly back to the ongoing conversation about compensation and disclosure. Agents in the answer set repeatedly circle back to the same point: enforce against the fraud that actually harms seniors, and get out of the way of the licensed brokers who are already doing the education CMS says it wants done.

Other Reforms That Kept Coming Up

Several other reforms appeared often enough to be worth naming, even if they didn't get their own section:

- End the lifetime Part B and Part D late enrollment penalties. The most frequently mentioned single rule in the full answer set. Agents overwhelmingly want the penalty capped in years, capped in amount, or eliminated entirely for seniors who had no way to know. (Status: Would require federal legislation.)

- Repeal the 3-day inpatient stay rule for skilled nursing coverage. Cited more than any other clinical rule. Under observation status, seniors get charged for care they thought Medicare would cover. Someone in a Medicare Advantage plan might not need the three-day inpatient stay, and Original Medicare has limited waivers through qualifying ACO arrangements, but the general rule remains a persistent frustration. (Status: Would require federal legislation.)

- Add an annual out-of-pocket maximum to Original Medicare. Right now there isn't one, which is why agents call Original Medicare without a supplement a serious financial exposure. A statutory MOOP would reduce the need for many Medigap purchases as pure catastrophic protection. (Status: Would require federal legislation.)

- Guaranteed-issue Medigap in every state, every year. Currently only a handful of states offer this. Agents say the underwriting cliff after the six-month federal Medigap Open Enrollment Period is a trap for seniors who chose MA for a good reason and now can't switch back to Medigap when their health changes. (Status: Primarily regulated at the state level.)

- Reform the annual AHIP and carrier re-certification cycle. Multi-hour America's Health Insurance Plans (AHIP) tests every year for career agents who have been selling the same products for a decade. Agents want the frequency dropped to every 3-5 years, with abbreviated update modules in between. (Status: Primarily controlled by carriers and Field Marketing Organizations [FMOs].)

What This Wishlist Says About the Industry

Read together, the reforms in the answer set share a pattern. Almost none of them are about paying agents more. Most of them are about removing friction that agents believe is currently being paid for by the beneficiary, either in confusion, in trapped enrollment status, or in denied care.

A few of them (standardizing MA, moving to multi-year plans) would materially compress the commission cycle. Agents proposed them anyway. That is worth noting when the industry gets accused of shaping every regulatory conversation around its own paycheck.

Some of these proposals would require legislation or major structural changes. Others are already moving. CMS's elimination of the 48-hour SoA wait for contract year 2027, beginning October 1, 2026, shows that sustained feedback from agents and other stakeholders can influence the annual rulemaking process. The narrowed recording requirements and shortened retention period are further evidence that CMS is listening to at least some of what the field is saying.

The shape of the wishlist, less compliance friction, more structural fairness, more real education, is a useful north star for any agent thinking about what to advocate for at the state association level, at the FMO level, or in the comment periods on the annual rulemaking. The people in the field have a clear read on what is broken. On at least one front, the people with rulemaking authority were listening.