How Medicare Agent Commissions Work: Structures, Rates, and Strategies for 2026

-

April 11, 2026

Medicare agent compensation is one of the most misunderstood aspects of the business, even among agents themselves. Whether you're newly licensed and trying to figure out how the money actually flows, or you're a veteran broker evaluating whether your current FMO relationship is leaving money on the table, understanding commission structures is essential to building a sustainable practice.

This guide breaks down how Medicare commissions work across every major product line in 2026, what factors affect your earnings, and how to make strategic decisions that compound over time.

How Medicare Agent Compensation Works

Medicare agents and brokers are paid commissions by insurance carriers, not by the beneficiary. This is a critical point that builds trust with clients: your services cost them nothing. Carriers pay you because you bring them enrolled members and handle the advisory work that would otherwise require their own sales infrastructure.

Commission payments follow a standard cycle:

- You enroll a client in a Medicare Advantage, Medigap, or Part D plan

- The carrier processes the enrollment and confirms it with CMS

- You receive an initial commission, typically paid within 30–60 days of the effective date

- You receive renewal commissions each subsequent year the client stays on the plan

The renewal piece is what makes Medicare a compelling long-term business. Unlike many insurance verticals where client churn is high, Medicare beneficiaries tend to stay on plans for years, which means your book of business compounds over time into a reliable income stream.

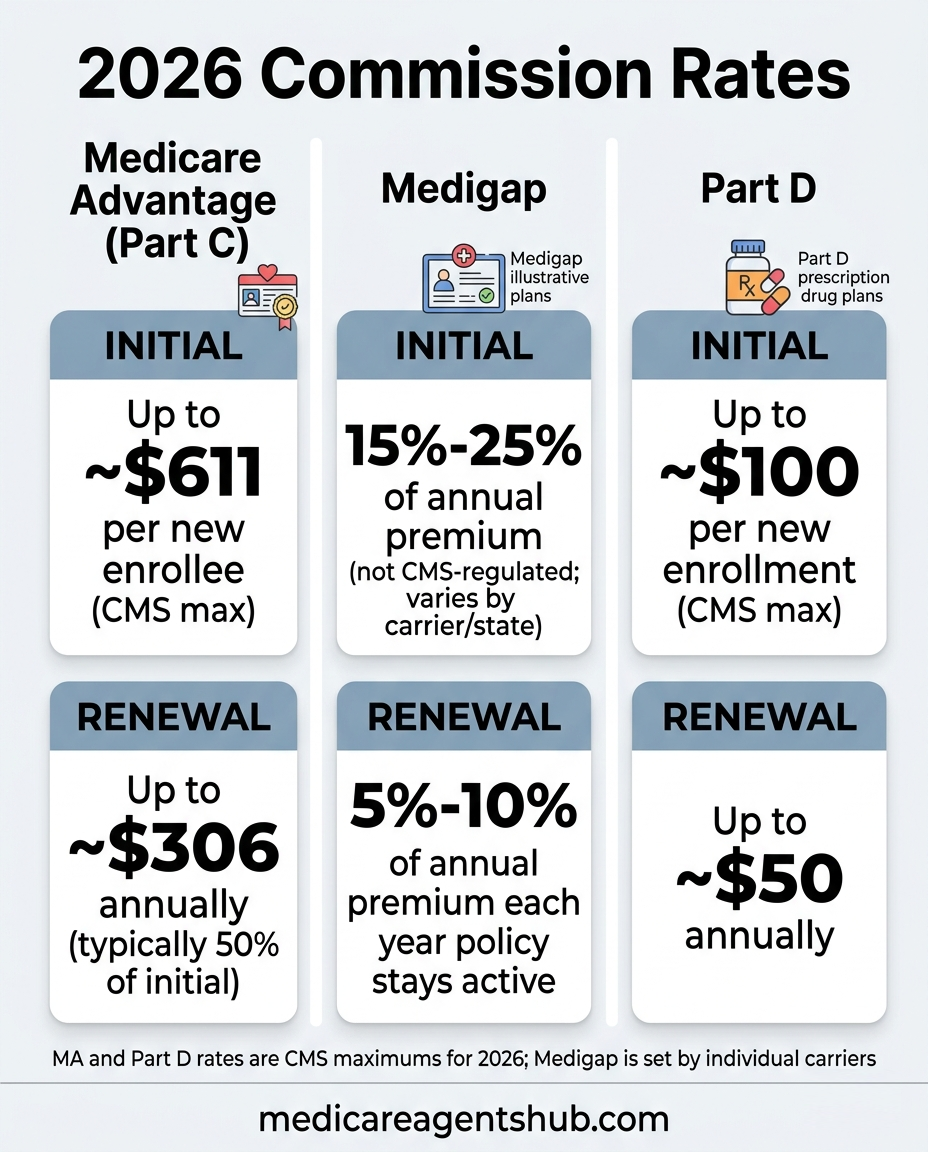

2026 Commission Rates by Product Line

CMS sets maximum broker/agent compensation amounts each year for Medicare Advantage and Part D plans. Carriers can pay up to these limits but not above them. Medigap commissions, by contrast, are not CMS-regulated; they're set by each carrier individually.

Medicare Advantage (Part C) Commissions

Medicare Advantage is where the volume is for most agents. With MA enrollment continuing to climb, this product line drives the majority of new business for independent agents.

| Type | Rate | Notes |

|---|---|---|

| Initial (new enrollment) | Up to ~$611 | Paid once per new enrollee; exact amount varies by carrier and market |

| Renewal | Up to ~$306 | Paid annually for each year the client stays enrolled (typically 50% of initial) |

| Like-to-like switch | Renewal rate | If a client switches between plans from the same carrier, you receive the renewal rate, not a new initial |

Important: These are CMS maximums for 2026. Actual rates depend on your carrier contract and FMO arrangement. Most carriers pay at or near these caps, but some regional plans or newer entrants may offer different structures.

Medicare Supplement (Medigap) Commissions

Medigap commissions are not regulated by CMS, which means they vary significantly by carrier, state, and plan type. This is where the payout differences between carriers can be substantial.

| Type | Typical Range | Notes |

|---|---|---|

| Initial (first year) | 15%–25% of annual premium | Some carriers offer flat bonuses on top of percentage-based commissions |

| Renewal | 5%–10% of annual premium | Paid each year the policy remains active; some carriers trail off after year 5–6 |

| High-value plans (Plan G, Plan N) | Higher end of range | Popular plans with higher premiums naturally pay more in dollar terms |

Because Medigap premiums are higher than MA premiums (beneficiaries pay monthly out of pocket), the dollar amounts on Medigap commissions can be significant, especially on Plan G policies in higher-cost states. A single Plan G enrollment at 20% of a $2,400/year premium puts $480 in your pocket on day one, with renewal income for years to come.

Part D (Prescription Drug Plan) Commissions

Standalone Part D commissions are the smallest of the three product lines, but they add up, especially if you're helping clients who stay on Original Medicare and need a drug plan alongside their Medigap policy.

| Type | Rate | Notes |

|---|---|---|

| Initial | Up to ~$100 | Varies by carrier and market |

| Renewal | Up to ~$50 | Annual, as long as the client stays enrolled |

Part D commissions alone won't build a practice, but they're a meaningful addition when paired with Medigap sales, and they reinforce the full-service value you provide to clients.

Initial vs. Renewal Commissions: Why Retention Matters

The math of Medicare commissions heavily rewards retention over acquisition. Here's a simplified example:

Scenario: You enroll 100 MA clients in Year 1 at $600 initial commission each.

- Year 1 income: $60,000 (all initial commissions)

- Year 2 income (assuming 90% retention + 100 new enrollments): $27,000 renewals + $60,000 new = $87,000

- Year 3 income (same pace, compounding retention): $24,300 + $27,000 + $60,000 = $111,300

- Year 5 income: Renewals alone could exceed $90,000 — before you write a single new policy

This is why the best agents treat every client interaction as a retention event. A quick check-in call during the off-season, a birthday card, a proactive ANOC review. These small touches keep clients from wandering during AEP. What you do between enrollment periods directly impacts your commission income.

The FMO Factor: How Your Upline Affects Your Pay

Most independent Medicare agents don't contract directly with carriers. Instead, they work through a Field Marketing Organization (FMO), also called a National Marketing Organization (NMO) or Independent Marketing Organization (IMO). Your FMO relationship has a direct impact on your commission rates.

What FMOs Do

- Carrier access: FMOs hold master contracts with carriers and extend appointments to their downline agents

- Commission processing: Carriers pay the FMO, who distributes to agents (some carriers pay agents directly)

- Support and training: Many FMOs offer quoting tools, CRM access, lead programs, and compliance support

- Override structure: FMOs receive an override (a percentage above what they pay you) from the carrier; this is how they make money

What to Watch For

Not all FMOs are created equal. Here's what to evaluate:

- Street-level commissions: The best FMOs pay "street level," meaning you get the full CMS maximum with no haircut. If an FMO is taking a cut of your commission (rather than earning only overrides from the carrier), that's a red flag.

- Release policies: Some FMOs make it difficult to leave by holding your book of business. Before you sign, understand whether you can take your clients with you.

- Production requirements: Some FMOs require minimum production volumes. Make sure these are realistic for your practice size.

- Carrier breadth: You want access to the major carriers in your market. If your FMO only contracts with a few carriers, your clients — and your commissions — are limited.

Independent vs. Captive: How Your Model Affects Earnings

Your business model fundamentally shapes your commission potential:

Independent Agent/Broker

- Contracts with multiple carriers through an FMO

- Earns commissions from whichever carrier you place business with

- Higher earning ceiling: you can cross-sell MA, Medigap, and PDP across carriers

- More flexibility to match clients with the best plan (which builds retention)

Captive Agent

- Works exclusively for one carrier (e.g., UnitedHealthcare, Humana)

- May receive a salary, benefits, or guaranteed leads in addition to commissions

- Lower commission rates per sale in many cases

- Limited to that carrier's product portfolio

Most agents who reach the highest income levels in Medicare are independent. The ability to offer every major plan in a market gives you more enrollment opportunities, higher close rates, and stronger retention, all of which drive commission income. If you're considering building a team, the independent model also gives you more flexibility in structuring compensation for junior agents.

Chargebacks and Rapid Disenrollment

Commissions aren't always permanent. If a client disenrolls from a plan within the first 90 days (sometimes longer, depending on the carrier contract), you may face a chargeback — the carrier claws back part or all of the initial commission.

Common chargeback scenarios:

- Rapid disenrollment: Client switches plans during OEP or uses a Special Enrollment Period shortly after enrolling

- Enrollment errors: If a plan is submitted incorrectly and gets canceled

- CMS compliance issues: If the enrollment doesn't meet CMS guidelines, the carrier may reverse it

The best defense against chargebacks is proper plan matching from the start. When clients are genuinely satisfied with their coverage: when their doctors are in-network, their prescriptions are covered, and their costs are predictable, they don't switch. This is where taking the time to uncover hidden client needs pays off in both client satisfaction and commission protection.

5 Strategies to Maximize Your Medicare Commission Income

1. Diversify Across Product Lines

Don't be an MA-only or Medigap-only agent. The highest earners sell across all Medicare product lines. A client on Original Medicare needs both a Medigap policy and a standalone Part D plan. That's two commission streams from one relationship. An MA client who's unhappy with their plan might be a great Medigap candidate. Versatility equals revenue.

2. Build a Consistent Lead Pipeline

Commissions require enrollments, and enrollments require leads. Agents who rely solely on AEP walk-ins or purchased lead lists hit a ceiling fast. Building a year-round lead engine, through directory listings, referral networks, community events, and digital presence, creates the steady flow of prospects that drives consistent commission income.

3. Prioritize Retention Over Acquisition

As the math above shows, renewal commissions compound. Every client you retain is worth $300+/year in MA renewals alone, with zero acquisition cost. Invest in a systematic retention program: annual plan reviews, proactive ANOC outreach, birthday and holiday touchpoints, and quick response when clients have questions.

4. Negotiate Your FMO Relationship

If you're producing consistently, you have leverage. Don't accept below-street commissions. Ask for bonuses, marketing support, or lead programs. If your current FMO isn't delivering value proportional to their override, explore alternatives, just make sure to understand your release terms first.

5. Cross-Sell Ancillary Products

Many Medicare agents leave money on the table by ignoring ancillary products. Dental, vision, hearing, hospital indemnity, and final expense policies all generate additional commissions from the same client base. These products often have higher initial commission percentages than core Medicare products, and they deepen your client relationship, which further strengthens retention on the Medicare side.

Common Commission Mistakes to Avoid

- Chasing the highest initial commission over the best client fit. Placing a client in the wrong plan to earn a higher initial payout leads to chargebacks and lost renewals. Always recommend the best plan for the client. The long-term math favors it every time.

- Ignoring Medigap because MA is "easier." Medigap commissions are percentage-based and can exceed MA commissions in dollar terms. Clients who prefer Original Medicare are often the most loyal (and highest-value) in your book.

- Not tracking your commissions. Carriers make mistakes. If you're not reconciling your commission statements against your enrollment records, you're probably leaving money on the table. Set up a simple tracking system and audit quarterly.

- Signing with the wrong FMO. An FMO that charges sub-street commissions, locks your book, or lacks carrier breadth in your market can cost you tens of thousands over a career. Do your due diligence before committing.

The Bottom Line

Medicare commissions are designed to reward agents who do the job well: who match clients with the right plans, keep them happy, and build a book that lasts. The agents earning six figures and beyond aren't necessarily the ones writing the most new business. They're the ones whose clients stay.

Understand the structures, negotiate fairly, diversify your product mix, and invest in the relationships that generate renewal income year after year. That's the formula for turning Medicare commissions into a career that compounds.