The Commission Conversation: Should Medicare Agents Recommend What Pays More?

-

April 27, 2026

Medicare Advantage pays more than Medigap. Every licensed agent knows it. The question that splits the industry is what that pay gap does to recommendations, and whether the current regulatory framework is enough to keep it in check.

We pulled answers from hundreds of licensed Medicare agents on three related questions: whether agents push MA over Medigap, whether CMS marketing regulations need to be stricter, and why seniors get bombarded with confusing ads. The responses reveal an industry that largely agrees on the problem but disagrees sharply on the solution.

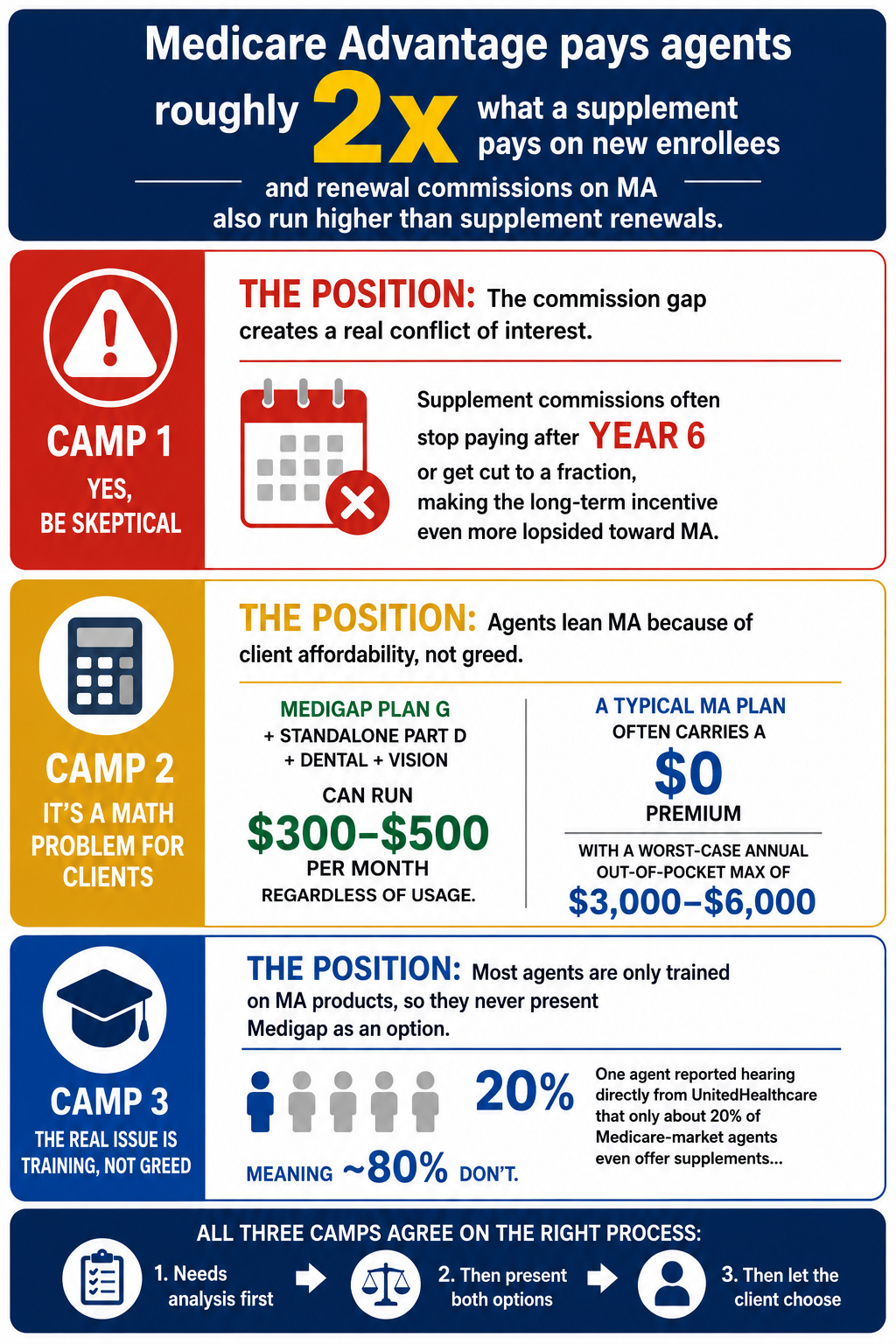

The Pay Gap in Plain Numbers

Agents are remarkably candid about the commission disparity. One veteran broker summed it up without sugarcoating: Medicare Advantage plans pay agents almost two times what a supplement pays, especially for new enrollees turning 65. Even renewal commissions on MA plans run higher than supplement renewals.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

Most of the time, it’s a math problem. With Medigap, you pay a monthly premium. But, you must also qualify medically for a Medigap Plan. You also continue paying your Part B premium. You don’t get dental and vision, so you pay extra for an outside plan. And you don’t get prescription coverage with Medigap, which you must have or be penalized. Prescription coverage has gone way up in price. What people like is, with Medigap, you can go to any doctor that takes Medicare- no networks. And if you get a good plan (higher premium) you’ll only pay your deductible and Part B premium, and all other medical expenses will be covered at 100%. And you may have some overseas coverage. The bottom line is you will pay between $300-$500 per month to be fully covered with a Medigap Plan, Dental, Vision, and Prescriptions- whether you use it all or not, or you you can have a Medicare Advantage Plan, which covers all of that for usually no premium, (some even give back the Part B Premium!) and pay copays as you go along, with usually a $3,000-$6,000 maximum out of pocket you would ever pay in one year in the worst case scenario! (hmm… that’s $250/$500 per month worst case scenario) And many Medicare Advantage plans give free gym membership, out of hospital meals, and some other benefits. Or, you use very little benefits per year and have very little cost out of your pocket. The Medigap Plan forces you to pay that monthly cost whether you use it or not. See, mainly a math problem.That math is why the conversation exists. When one product essentially sells itself on price and the other requires a monthly premium commitment, the agent's recommendation carries extra weight.

Three Camps on the Commission Question

"Yes, Be Skeptical"

A significant number of agents don't hedge when answering this question. Some are blunt about the conflict of interest baked into the compensation structure.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

There are a few reasons why agents push Medicare Advantage plans over Medigap plans! Yes you should be very skeptical! The reason why they push Advantage Plans is because they actually get a HIGHER COMMISSION when you enroll in an Advantage plan! It's very easy to entice clients to get an Advantage plan when many of them are FREE and have NO premiums! NOTHING IN LIFE IS FREE!!! Medicare insurance is NOT free! There's millions of agents out there pushing Advantage plans but they are hurting seniors because they are not truly informing them of the pros and cons of Advantage Plans vs Supplement Plans. It's a lot easier to tell someone they can get a FREE plan that comes with "extra benefits" like a flex card to pay for bandaids and tylenol but they NEVER tell you that you are REPLACING Medicare as the Primary Payor of the claims so therefore you DO NOT have Medicare when you REPLACE it with a managed-care plan (aka Advantage Plan). The agents don't tell you that Advantage Plans DO NOT cover the 20% of chemotherapy/radiation and the top cancer facilities DO NOT accept Advantage Plans! As a licensed agent, we have been telling people the truth about Advantage Plans, like how you most likely will never get a Supplement Plan later on in life when you realize that he Advantage Plan has failed you once you actually have a health condition that they won't pay for! -Nick ManginiThat level of directness stands out. Most agents soften the message, but a subset of respondents were equally pointed. One broker noted that supplement commissions often stop paying after year six or get cut to a fraction, making the long-term financial incentive even more lopsided toward MA. Another agent went further: most agents look at what's financially better for them instead of what's best for the client.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

There is no doubt, MA plans are often pushed as they will provide the highest commissions for those enrolling into Medicare for the first time.This is a fools errand, and if they are just neglecting the overall needs it will likely backfire, but it is a fact of the industry.

On the other hand, you may also ask, why don't agent/brokers inform consumers about High Deductible G supplements? Simply, money or commission.

So there are bad actors in all arenas.

Shop a few brokers and use your better judgments to see who is really taking your needs into account and solving it as best as possible.

The High Deductible G point is one almost nobody else raised. It suggests the commission bias runs in multiple directions, not just the MA-Medigap divide.

"No, It's a Math Problem for Clients"

The other camp argues the MA lean is about client economics, not agent greed. One agent described it as a straightforward affordability issue: most seniors are on fixed income, and MA plans are simply more accessible up front. A Medigap Plan G with a standalone Part D plan, dental, and vision can run $300 to $500 per month whether the beneficiary uses services or not. An MA plan often carries a $0 premium with a worst-case annual out-of-pocket maximum of $3,000 to $6,000.

One respondent added a detail that complicates the simplistic "agents are greedy" narrative: he has multi-millionaire clients on Medicare Advantage because they just didn't want to pay the supplement premium. But he also makes sure every client knows that supplement premiums go up every year and will most likely double in 10 years.

"The Real Issue Is Training, Not Greed"

The largest group of respondents pointed to a structural problem that gets less attention than the commission debate: most agents are only trained on MA products.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

Yes you should be skeptical. Recently, while I was in a meeting with united healthcare, I learned only twenty percent of agents who help individuals in the medicare market offer both medicare, supplements and medicare advantage plans. In my opinion, this is due to two reasons. The first reason being individuals answer a help wanted ad to find out that it's insurance. They know nothing about insurance and the agency helps them get their license. Those individuals are taught only medicare advantage. I can confidently say that because when I went into medicare from property and casualty in the year 2005 that's exactly what the agency did to me. It wasn't until I realized what these plans actually were and talk to different company that I learned about medicare supplement. So if an agent doesn't know anything about medicare supplement, and they've only been taught medicare advantage, they're only going to offer medicare advantage. Now, to answer, the second reason is the agent is financially incentivized to only offer you medicare advantage. Think about it this way, you go to a job interview and the hiring individual tells you they can pay you a $100 a day to do the job or $200 a day to do the job and it's the same job. Which pay would you choose? Anyone in their right mind would choose double the pay. That is, the incentive to selling medicare advantage over a medicare, supplement. As an agent, I am incentivized to sell you only a Medicare advantage plan because they will pay me twice as much. If not more, then what the insurance company will pay me for a medicare, supplement.That 20% figure, from an agent who heard it directly in a meeting with UnitedHealthcare, reframes the entire discussion. If 80% of agents in the Medicare market don't even offer supplements, the commission incentive is almost secondary to a basic knowledge gap.

Another agent's career arc illustrates the same problem from the inside.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

When I first got started in the Medicare world, I was a captive agent. In other words, I worked for a large national agency that only sold Medicare Advantage Prescription Drug Plan (MAPD). Back then, I thought MAPDs were the best thing since sliced bread because the plans typically had a $0 monthly premium.As an independent broker I have the ability to better serve my clients with Medigap (a.k.a. Medicare Supplement Plans).

Doing the proper Health Needs Assessment shows me which plan is best for my client. If they have any health issues or simply enjoy traveling out of state, I always recommend a Medicare Supplement. That said, if they still insist on a MA or MAPD because of the $0 monthly premium, I strongly advise them to protect themselves from the unexpected expenses associated with high deductibles and out-of-pocket maximums by adding either a Hospital Indemnity plan or Out-of-Pocket protector plan.

That journey from captive to independent, from thinking MAPDs were "the best thing since sliced bread" to running proper Health Needs Assessments, is one several agents described. The pattern is consistent: agents who start captive and later go independent almost universally say their recommendations changed once they could see the full picture.

How Compensation Actually Works

Before going further, it helps to understand the mechanics. We asked agents directly: how do you get paid, and does it affect what you recommend?

For Medicare Advantage and Part D plans, CMS sets a maximum broker compensation that creates a level playing field across carriers. Medigap commissions are set by individual insurance companies and vary more widely. In both cases, the insurance company pays the agent, not the client. Premiums are the same whether you enroll through an agent or directly.

One agency owner took a structural approach to eliminate the bias entirely.

How do you get paid, and does it affect the plan you recommend?

My office has everyone set up on a salary, BECAUSE I NEVER wanted them to look at commissions & sell a plan based off that! BUT most agents are paid based on commissions, so be careful, it would not hurt if you visited 2 agents to get recommendations from more than one. Getting referrals from your Doctor, friends, church members is also a great way to be sure you are in with the right agentThat's an unusual model. Most agencies pay commission-based, which means the commission structure directly shapes what gets recommended. Another agency described capping and leveling compensation to be the same across all carriers, removing the financial reason to favor one plan over another.

Where Agents Agree: Call Centers Are the Problem

If there's one thing that unites nearly every agent who responded, it's frustration with call centers and third-party marketing organizations (TPMOs). The comments are fierce.

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

When it comes to marketing my answer is yes. These days there are way too many people / companies blowing up people phones with fake numbers and hiring some guy from India or Bangladesh try to sell Medicare. I'm not a senior but I've been getting blown up with those phone calls also. One day during this last AEP I counted 63 scam calls in just one day. More regulation please. Seniors' phones don't need to be blown up every 5-10 minutes with scam, robo telephone numbers. They shouldn't have to deal with the hassle.63 scam calls in a single day. And that's from an agent, not a senior. The agents on the receiving end of these calls, who are also supposed to be following the same rules, are often the angriest about what's happening.

Why does Medicare allow insurance companies to bombard seniors with confusing mail and TV ads?

It's a great question. I would go one even further. Not only why does Medicare allow insurance companies to bombard seniors with confusing mail, tv and radios, but why does Medicare allow insurance companies to blow up seniors phones.In most cases, it's not the insurance carriers themselves actually doing any of it. It's lead vendors that are responsible for almost all of it. The lead vendors get seniors to give them their information through what is often false or misleading advertising. Then they sell that information to insurance brokerages and agencies. It's the vendors who make the ads, buy tv and radio air time and internet and social media ads, send out the mailers, run the call centers, etc. The agents, the agencies and the brokerages often don't know what is being promised in these ads or by the operators in the lead vendor call centers.

Medicare has taken steps to crack down on the lead vendors, but they need to do more. Seniors need to call their Congressmen and Senators.

That distinction matters: it's not always the insurance carriers doing the bombarding. It's lead vendors operating between the carriers and the agents, creating ads, buying airtime, running call centers, and then selling the harvested contact information to brokerages that may have no idea what was promised.

One agent described the specific mechanism these operations use to get around the law.

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

YES! There should be. These TPMO, Third Party Marketing Organizations, have figured out how to get around the laws already in place. The calls come from overseas using fake or non-working phone numbers and the beneficiary is required to attest that the transfer to the agent is an incoming call. This is how the agents are getting around the illegal cold calls but the laws were expanded to the TPMO as well. But you can't catch them if you don't have a working return phone number or a full name. Some even require you to attest that they can share your information so you get more calls. Permission to contact according to the law must be given in writing, not verbal. COLD CALLS ARE ILLEGAL, so never talk to these people. Simply hang up and never, ever give them your information. I had 4 people last month have their plans flipped and they all told me they told the agent they did not want to change anything, BUT they had already given all of their information. The only way to stop this illegal harassment is to make it illegal for agents to sell over the phone, change the laws back. Contact your Congress members and request this.The attestation workaround is a recurring theme in the responses. Multiple agents described the same tactic: offshore call centers using fake numbers, requiring seniors to "confirm" the call was incoming, technically satisfying the permission-to-contact requirement while violating its intent.

A broker who has been in the trenches for 16 years captured the collateral damage: new regulations designed to stop telemarketers end up killing legitimate business relationships with local agents who meet clients face to face. The rules that were supposed to protect seniors from call centers are instead adding friction for the agents who already do it right.

The Regulation Debate: Stricter Rules or Stricter Enforcement?

Side A: Tighter Regulation Needed

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

Hell yes, there should be stricter regulations.Most of the advertising done by Third Party Marketing Organizations in regards to Medicare Advantage are at best misleading and often flat out lies. Claims that "EVERY SENIOR GETS A FOOD CARD, GROCERY CARD or FLEX CARD" or "EVERY SENIOR GETS DENTAL IMPLANTS" just aren't true, and the agencies buying the leads generated from this false advertising know this. It's classic "BAIT and SWITCH," and it should be illegal.

The bait-and-switch accusation around food cards, grocery allowances, and flex cards came up repeatedly. Agents pointed to specific promotions that overshadow the core purpose of Medicare, causing confusion for beneficiaries who chase "extra money" rather than choosing coverage that supports their health needs.

Others cited the celebrity TV endorsement era. One veteran agent recalled how commercials featuring Joe Namath, William Devane, and Jimmie Walker misinformed the public and caused people to switch plans when they already had the same plan with another company. CMS eventually forced the commercials to be redone, but the damage was done.

Several agents called for limiting telephonic sales drastically. One reported that most of her clients get 10+ Medicare-related calls per day. Another went further: telemarketing should be outlawed entirely for people 65 and older.

Side B: Regulations Are Already Strict

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

CMS is very strict on how Agents and Agencies can market and sell. Agents are not allowed to cold call, door knock, or use unsolicited texting. Agents must have permission to contact before calling a prospect. Agents must document with a Scope of Appointment what products are to be discussed prior to meeting with a prospective client. All sales calls are to be recorded. Agents must use CMS approved disclaimers and receive prior approval from the companies when marketing specific plan benefits.Agents in this camp say the existing rules are comprehensive. The issue is enforcement, not gaps in the rulebook. One put it plainly: there are so many restrictions now that it is incredibly difficult for those of us following all the rules. The people who aren't doing right aren't following the rules anyway, so stricter rules just make it harder for the rule followers.

An agent who has been through the compliance gauntlet year after year captured the frustration perfectly.

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

Heavens yes!!! I'm of the age and I get 10 or more calls a day. They are robo calls so it is hard to stop them. We as agents are not allowed to call potential clients out of the blue. They have to give us permission to call. So how do these companies on robo calls get away with it. It is drummed into our heads when we take our yearly exam that we can' t do it, yet here are my 10 - 15 calls per day.That's the paradox: agents who take the yearly certification exam are told repeatedly that cold calls are prohibited, while their own phones ring 10 to 15 times a day with exactly those calls. The rules exist. The enforcement doesn't.

Side C: Target the Bad Actors, Not the Industry

This was the most common position. Local agents consistently argued that their face-to-face business model already protects clients, and that CMS regulations designed around call center abuses end up punishing agents who physically see clients and build long-term relationships.

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

This is a heavily debated topic. I personally believe that most smaller, local agents do a good job. Some larger call center-type agencies push the line on compliance. Then CMS (Center for Medicare and Medicaid Services) comes out with generic rules for all agent vs just addressing those entities that need addressing. I am all for making it easier and safer for the customer.That's the core frustration: generic rules applied to all agents when the problems are concentrated in a specific segment. Multiple agents called for eliminating offshore call centers entirely and regulating national outbound operations more heavily, while leaving local face-to-face agents alone.

One agent offered a characteristically blunt assessment of how CMS handles enforcement.

Should there be stricter regulations on Medicare Advantage marketing and sales practices?

There are very strict rules about unsolicited contact with a Medicare Beneficiary. The problem is lack of enforcement. If you get one of those calls, tell them it sounds good, but why would want to deal with a criminal? The centers for Medicare and Medicaid (CMS) does not police these plans,but rather allows the MAPD plans to police themselves. Kind of like the fox guarding the Chicken Coop!The fox-and-henhouse metaphor resonated across dozens of responses. When the entities being regulated are also responsible for policing themselves, the incentive structure guarantees gaps.

Why the Ad Flood Exists

Behind the regulation debate sits a more fundamental question: why does the system allow this level of marketing in the first place?

One agent offered a perspective nobody else did, cutting past the usual complaints about call centers to explain the structural incentive.

Why does Medicare allow insurance companies to bombard seniors with confusing mail and TV ads?

Because MA plans save the government money! Not you!The government has determined that a person turning 65 will “cost” them $375,000 each before they expire.

Now, the government has allowed these private companies to receive $13,000 - $15,000 a year for each individual they put on a C plan. So if the average age was 80, they would be paid $225,000 in that span. The government then saves $150,000 per person who moves to an MA plan!

Then the company doesn’t want to lose all their money, so they offer lengthy, alternative remedies, before they will consider a more expensive surgery! So all that “fluff” in the beginning, sure doesn’t pay off when it’s really needed.

If those numbers are even directionally right, the government has a $150,000-per-person financial reason to encourage MA enrollment. That creates a system where aggressive marketing isn't a bug; it's a feature that serves everyone's interest except possibly the senior's.

Another agent offered a darker read on the confusion itself.

Why does Medicare allow insurance companies to bombard seniors with confusing mail and TV ads?

Ads have to be approved by Medicare, but that really only is to make sure that they aren't outright lying.People who are confused are easier to push into making a decision to switch plans. If I can confuse you, it is easier for me to convince you that I alone have the answer.

This is why it is VITAL for you to have a person you can call, somebody you trust, who will lay out options and let you make a choice that YOU feel is best. Don't pick a plan because somebody told you to, pick a plan that you believe is right for you.

That framing, that confusion is a tool rather than an accident, is uncomfortable but consistent with how the system operates. When a senior is overwhelmed by 10 calls a day and a mailbox full of competing offers, the person who cuts through the noise has outsized influence over the decision.

The 48-Hour Rule: Protection or Theater?

CMS requires a 48-hour waiting period between when a beneficiary grants a Scope of Appointment and when the sales conversation can take place. Agents are split on whether this rule helps or just adds friction.

One agent called the SOA and 48-hour rule burdensome and unnecessary, though he supported other marketing regulations. The logic is that a local agent who meets a prospective client at a community event or through a referral shouldn't have to wait two days to have a conversation the client requested.

On the other side, agents who work with vulnerable populations see value in the cooling-off period. When someone has been pressured by a call center or confused by a TV ad, that 48-hour window gives them time to step back before committing. One agent noted that the rule is one of the few tools that actually slows down high-pressure tactics.

What "Needs Analysis First" Actually Looks Like

When agents describe doing it right, a consistent process emerges. Several agents outlined what a proper client meeting involves: reviewing the client's current medications and doctors, checking network coverage, understanding their travel habits, assessing their health situation, evaluating their budget, and then presenting both MA and Medigap options with clear pros and cons.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

If the agent is a 'captive' agent, then they are going to push the plans offered by their carrier and possibly plans that help them meet a quota or get a bigger commision.As an Independent Medicare Broker, I represent 7 carriers that offer dozens of different plans (Medicare Supplement, MA, MAPD, PDP, C-SNP and D-SNP). My job is to review the clients needs and present them options bases on those needs. My guidance is unbiased and my only interest is doing what's best for the client. Clients should never be pressured to pick one type of plan over another.

That's the model that agents across the industry say they aspire to, even when they disagree on everything else. Do the needs analysis. Present the options. Let the client choose. And if they ask about commissions, tell the truth.

One veteran agent offered practical advice for finding agents who actually operate this way.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

There are “captive agents” who work exclusively for only one insurance company. Therefore, they push the Advantage plan since it is the only one for that agent to earn a commission! Thus, what I have said before many times in this column, it is essential to be interviewed by 2-3 different agents, preferably an independent agent who may also be known as “a broker” who is affiliated with a variety of different firms and can tailor his advice to specifically YOU! Don't be afraid to ask the question as to whether she/he is a broker and have the agent name a minimum of five different national insurance firms for whom an application can be written! Remember: there is no “cookie-cutter” plan recommendation for everyone!The "interview 2-3 different agents" approach is one of the few concrete, actionable pieces of advice that came up consistently. If an agent can't name at least five national insurance firms they can write with, the recommendation you're getting may be limited by their contracts rather than guided by your needs.

Where This Leaves the Industry

The commission gap between MA and Medigap isn't going away. Neither is the tension it creates. What these agent responses reveal is that the vast majority of licensed professionals know the right way to handle it: educate, compare, and let the client decide.

The disagreements are about everything else. How much regulation is enough. Whether CMS should write broader rules or enforce existing ones harder. Whether the 48-hour rule protects seniors or just slows down legitimate business. And whether the growth of Medicare Advantage makes these questions more urgent or less.

What no one disputes: the agents who take the time to explain both options, who run a real needs analysis, and who let clients make informed decisions are the ones building books of business that last. The ones chasing the bigger commission check at the expense of client fit are the ones giving the industry a bad name.

The commission conversation isn't comfortable. But the agents willing to have it honestly are the ones worth listening to.