The Mid-Year Doctor Drop Playbook: How Top Agents Handle the 'My Doctor Just Went Out of Network' Call Without an SEP

-

July 14, 2026

Every Medicare agent knows the call. A client rings in April or July, panicked because their Medicare Advantage plan just dropped their cardiologist, primary care doctor, or the entire physician group they have used for fifteen years. There is no plan change to reverse, no obvious Special Enrollment Period to trigger, and the next window to switch is months away. This article distills how experienced agents actually triage that call, based on 179 answers licensed Medicare agents wrote in response to three related consumer questions on Medicare Agents Hub about mid-year network changes and enrollment options after OEP closes.

Why Mid-Year Network Changes Are Legal (and What to Say First)

Before you can advise the client, you have to reset their expectations about what a Medicare Advantage network actually is. Agents describe the same core reality over and over: MA plans are built on contracts between the carrier and the provider, those contracts have expiration dates, and either side can walk away. Sometimes it is the provider refusing a rate cut. Sometimes it is a large medical group renegotiating leverage. Sometimes it is the carrier trimming the network to hit a margin target. What the CMS rulebook does require is at least 30 days of advance written notice to affected members before a provider termination takes effect, and in the case of primary care physicians and specialists a longer runway is common.

The talk-track that works: acknowledge how unfair it feels, explain that this is a structural feature of managed care rather than a bug, and pivot to what can be done. Do not open with the SEP conversation. Ninety percent of the time there is no SEP, and leading with that fact detonates the call. Lead with verification.

My Medicare Advantage plan listed my doctor, but now they say he's out of network. How is that even allowed?

Unfortunately, you can conflicting information about network providers. We always recommend verifying that your provider(s) are in network through one of the following pathways:- Contact a local, Trusted, Medicare Agent;

- Verify through the carrier website;

- Contacting the member services of the selected plan prior to enrolling;

- Asks your provider if they plan to remain in network for the year or if they anticipate any changes on plans they will accept in the future;

- or contact support at Medicare.gov.

As an agent, I verify providers are in network through a minimum of 2 sources. If conflicting information is discovered (and it happens...a lot this year), we take additional steps to verify and confirm in network prior to advising a client to enroll and risks losing their trusted providers.

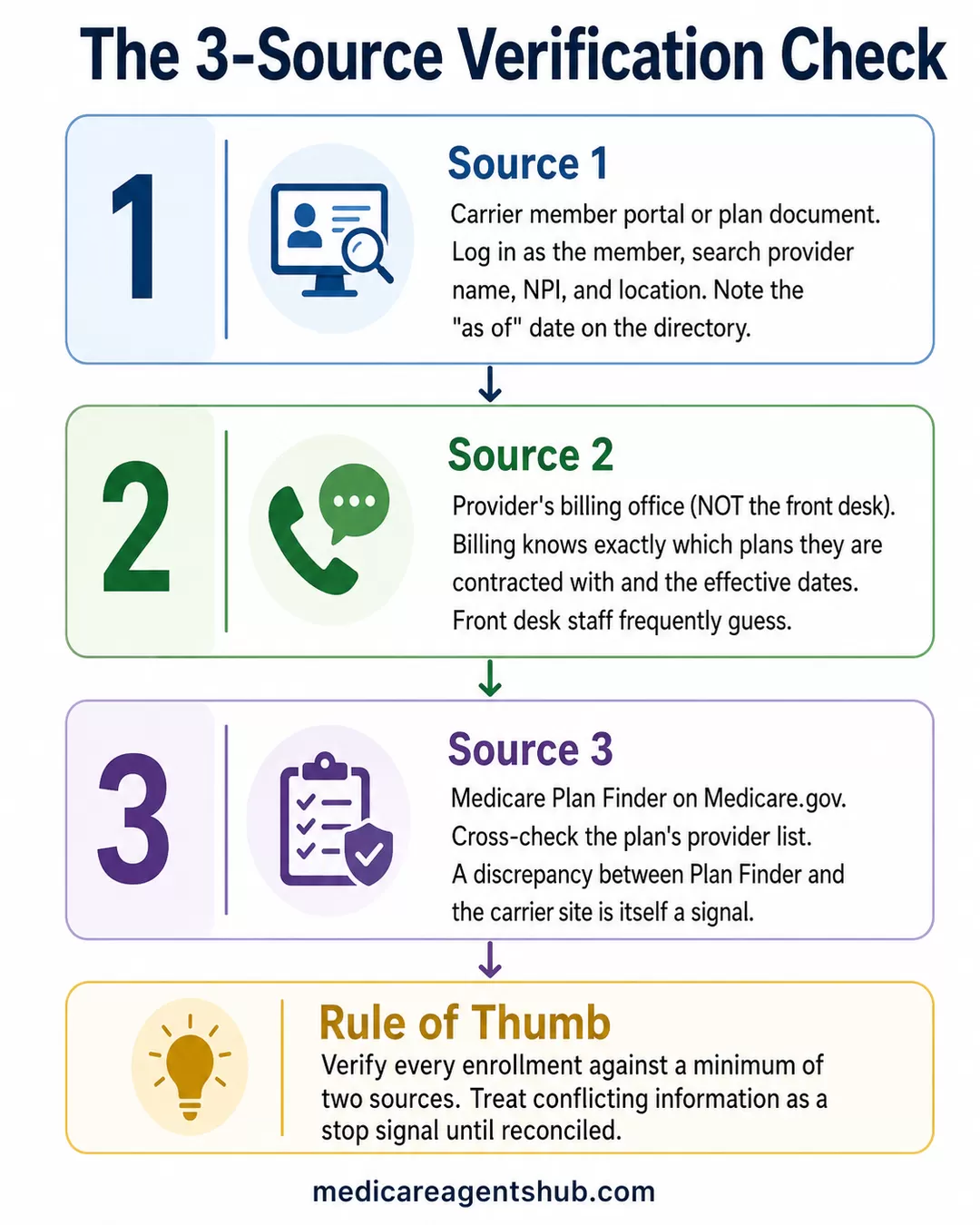

Step One: The Three-Source Verification Check

A meaningful percentage of "my doctor is out of network" calls turn out to be resolvable at this stage without a plan change at all. Directories are wrong constantly. Provider billing offices misread the fine print on their own contracts. Carrier member service reps read from stale screens. Before you accept the premise of the client's crisis, verify from three independent sources:

- The carrier's member portal or the plan document itself. Log in as the member (or coach them through it) and search the provider name, NPI, and location. Note the "as of" date on the directory.

- The provider's billing office, not the front desk. Front desk staff frequently guess. Billing knows exactly which plans they are contracted with and what the effective dates are.

- Medicare Plan Finder. Cross-check the plan's provider list on Medicare.gov. If Plan Finder is out of sync with the carrier site, that discrepancy itself matters — more on that below.

Agents commonly report they verify every enrollment against a minimum of two sources at the point of sale, and treat conflicting information as a stop signal until it is reconciled. That same discipline is what a good mid-year triage looks like.

Reading the 60- to 120-Day Termination Notice

If the network change is real, ask the client whether the plan sent them a letter. Most did. Under CMS rules, carriers must send affected members written notice of a specialist termination at least 30 days in advance, and for a primary care physician or a large group termination the practical notice window is typically 60 to 120 days. That letter is the single most useful document in the file, because it establishes:

- The exact effective date of the termination

- Whether the termination was for cause (fraud, quality) or without cause (contract dispute, non-renewal)

- Any continuity-of-care rights the plan is offering — often a 90-day bridge for members mid-treatment

- Whether the plan is proactively assigning a replacement PCP the member did not ask for

Two operational moves from experienced agents. First, ask every new client during enrollment to forward you any letter from their plan for the entire year, sight unseen. That single habit turns you into the first person to see a network termination in your book instead of the fifteenth. Second, when a large group leaves a plan in your market, log it. If a plan is failing its members in a systemic way, you will see the pattern in your notes weeks before it hits the trade press.

When It Is a Contract Dispute (and the Answer Is "Wait")

Not every network termination sticks. Provider groups and carriers routinely use termination notices as leverage in rate negotiations, and a meaningful share of announced terminations get reversed before the effective date or within weeks after. Coaching a client through that limbo is its own skill:

- Do not rush a plan change. Switching to a new plan mid-year (if an SEP even exists) forfeits any negotiated resolution.

- Track the public posture of both parties. Local news, hospital system press releases, and the carrier's own member communications will telegraph whether talks are alive or dead.

- Get the client on the provider's mailing list. Large systems email patients directly when a deal is signed.

- Set a decision date. If nothing has changed by X, we execute Plan B. Ambiguity is what wears clients out.

Agents who have been through several of these cycles are usually the ones telling the client to breathe. The reflex to "do something now" is exactly what backs a client into a worse plan.

The SEP Question: What Actually Qualifies

The unpleasant truth is that a mid-year provider network change on its own is not a categorical SEP under CMS rules. The workable exceptions are narrow but worth knowing cold:

- Plan-level SEPs. If the carrier itself is exiting a service area or terminating its Medicare contract (not just dropping one provider), members get an SEP. This is what triggered the recent Clear Spring Health exit.

- 5-Star SEP (Dec 8 – Nov 30). If a 5-star MA or Part D plan is available in the member's county, they can switch to it once during this window regardless of provider issues.

- OEP (Jan 1 – Mar 31). For members already in a Medicare Advantage plan, this is the reliable window to switch to another MA plan or drop back to Original Medicare. Coach them to use it if the network problem is not resolved by year-end.

- Case-by-case exceptional circumstance SEP. Medicare.gov instructs beneficiaries to call 1-800-MEDICARE when they believe misleading provider directory information caused their enrollment. This is discretionary and inconsistently granted, but it is real. It is worth the client's phone call in situations where the directory was demonstrably wrong at the point of enrollment.

The Plan Finder SEP that CMS introduced for 2026 has been widely misread. It applies specifically to enrollments based on incorrect information from the Medicare.gov Plan Finder — not from the carrier's own website or a broker portal. If the plan's website was wrong, the exceptional-circumstance path is the correct escalation, not the Plan Finder SEP.

My Medicare Advantage plan listed my doctor, but now they say he's out of network. How is that even allowed?

Unfortunately, yes, this can be allowed.With Medicare Advantage plans, the doctor network is based on contracts between the insurance company and the doctor, medical group, or facility. Those contracts can change during the year. A doctor can leave the network, a medical group can stop participating, or the plan may update its network based on contract changes.

That is why a doctor may show as in-network when you enroll, but later show as out of network.

That does not mean it feels right, especially if you chose the plan specifically because that doctor was listed. But Medicare Advantage plans are not required to keep every doctor in the network for the full year.

The key question is what happened:

Was the doctor truly in-network when you enrolled?

Did the doctor or medical group leave the plan mid-year?

Or was the provider directory incorrect when you reviewed the plan?

The next step is to call both the insurance company and the doctor’s billing office and ask for the effective date of the network change. If the doctor was listed incorrectly, or if the network change creates a major access issue, then we can review whether there are any options available.

Important distinction: if the mistake came from the insurance company’s own provider directory, the special 2026 Plan Finder SEP may not apply. CMS says that particular SEP is only for people who relied on incorrect information from Plan Finder, not from a plan website. But the plan website error may still support a case-by-case SEP request through Medicare if the information was misleading or incorrect. Medicare.gov specifically says to call 1-800-MEDICARE if you think you have an exceptional circumstance.

Guaranteed Issue and the Medigap Off-Ramp

For clients who are ready to abandon Medicare Advantage entirely and go back to Original Medicare plus a supplement, the calculus changes. In most states, moving from MA to Medigap outside the initial six-month Medigap Open Enrollment window means medical underwriting — and unhealthy clients get declined or rated. That is why so many mid-year network calls end with the client stuck.

But Guaranteed Issue rights survive past the Medigap Open Enrollment Period in specific qualifying situations that every agent should have memorized. Loss of employer or union coverage. A Medicare Advantage plan leaving the service area. Moving out of a plan's service area. A plan losing its Medicare contract. The Medicare Advantage trial right within the first 12 months. Loss of Medicaid. And several states — New York, Connecticut, Massachusetts, Maine, and a handful of others — have their own broader Medigap protections that make year-round switching realistic. If the client is in a GI-friendly state, that changes the plan entirely.

Is Guaranteed Issue available after the Medicare Open Enrollment period ends?

Yes — Guaranteed Issue rights do exist after the Medicare Open Enrollment Period, but they only apply in very specific situations.Here’s how it works:

🧾 What Guaranteed Issue Means

Guaranteed Issue means that certain Medigap (supplement) plans must be offered to you without medical underwriting, even after the general enrollment periods have passed.

📅 When You Can Have Guaranteed Issue After Open Enrollment

You may have Guaranteed Issue rights outside of the initial Medigap Open Enrollment Period if one of these situations applies:

✅ Your current coverage is ending involuntarily

For example:

• Your employer group retiree plan is ending

• Your COBRA ends

• You lose Medicaid

• Your plan stops providing Medicare benefits

✅ You’re in a Medicare Advantage plan and it is ending service in your area

If your MA plan leaves Medicare or stops giving you coverage in your county, you get a special right to join certain Medigap plans without health questions.

✅ You move out of your plan’s service area

And your Medicare Advantage or Medigap plan doesn’t follow you.

❌ When Guaranteed Issue Does NOT Apply

Guaranteed Issue rights do not mean you can pick a Medigap plan at any time after open enrollment — only when one of the qualifying events above happens. If none of those apply, you may have to wait for a Medigap Open Enrollment Period or potentially be subject to medical underwriting.

📌 Key Takeaway

Yes — Guaranteed Issue can be available after open enrollment, but only if a qualifying event triggers it. It is not automatically available every year.

Where GI is not on the table, the honest conversation is that the client has three real options: pay cash to keep seeing the doctor for the rest of the plan year, find an in-network replacement provider, or accept underwriting risk to move to Medigap. Framing all three neutrally protects the relationship. The client's frustration is with the plan, not with you.

Is Guaranteed Issue available after the Medicare Open Enrollment period ends?

A lot of people think that once their Medicare Supplement Open Enrollment Period ends, they’ve missed their chance forever to get a Medigap plan without health questions. Thankfully, that’s not always true.The reality is that guaranteed issue rights can still become available later on in certain situations. For example, if you lose employer coverage, move out of your Medicare Advantage plan’s service area, your plan terminates, or you qualify for a Medicare Advantage trial right, you may still be able to enroll in a Medicare Supplement plan without medical underwriting.

Some states, like New York, even offer additional consumer protections that make switching Medigap plans easier year-round.

The important thing to understand is that Medicare rules are not always one-size-fits-all. Your rights can depend on timing, your state, and how your previous coverage ended.

That’s why I always tell people not to assume they’re stuck. I’ve seen many situations where someone thought they had no options left, only to find out they actually qualified for guaranteed issue protections. Sometimes it just takes having the right person look at the situation carefully and explain things in plain English.

State Variation Is Not a Rounding Error

The same fact pattern produces very different outcomes depending on where the client lives. Medicare Advantage service areas are county-level, so a plan that dropped a provider in one county may still be viable for a client three miles away in the next county. Medigap plans are standardized federally but priced and regulated at the state level, and a handful of states (Wisconsin, Massachusetts, and Minnesota) do not follow the standardized model at all. Part D formularies vary by carrier and region. When you triage a mid-year network call, the client's zip code determines what tools you actually have.

Are Medicare plans and requirements different for every state?

Medicare itself is regulated at the national level (CMS), so Medicare’s premiums, timelines, compliance rules, costs, requirements, enrollment periods, premiums, deductibles, rules & regulations are standardized nationwide.Medicare Supplements (Plan F, Plan G, Plan N & others) are also standardized nationwide, but a few states have rejected the standardized model and created their own unique model of Medicare Supplement that has its own set of coverages.

Medicare Prescription Drug Plans (Part D) and Medicare Advantage Plans, while being heavily regulated by CMS to follow strict guidelines, are service-area specific, and vary across the insurance companies who are contracted with Medicare.

The “service areas” are counties, and then differentiated again per state. Each insurance company must align with Medicare rules, but is allowed to provide additional benefits and services above the Medicare model.

Part D coverage is a Medicare requirement (with a penalty for going without it), but is provided by insurance companies, not Medicare itself.

Medicare plans change once per year January 1, and are available for agents and beneficiaries to see every October 1, with enrollments allowed into the following year’s plans October 15 - December 7.

In reviewing your Medicare coverage options and education, you can consult the Medicare & You Guidebook that is mailed to all Medicare beneficiaries, available on Medicare.gov. It’s also important to become aligned with an agent or broker who has been certified by CMS and contracted to represent plans *compliantly* with Medicare’s rules and regulations. Make sure they know their stuff!

The Prevention Layer: Setting the Book Up So This Hurts Less

The best playbook is not the one you run after the call comes in — it is the one that reduces the volume of calls in the first place. Agents who report smoother off-seasons tend to share several habits:

- Provider verification at enrollment is mandatory, not optional. Two-source minimum. Note it in the file with dates and screenshots.

- Annual reviews are actually annual. A pre-AEP check-in catches most of what would otherwise become a mid-year fire drill. Agents who work the OEP window well report that most of their OEP switches were triggered by network or formulary changes flagged in the ANOC.

- Know your creditable coverage sources cold. When a client loses employer coverage or COBRA mid-year, that is your window for a clean GI-eligible move back to Original Medicare and Medigap. Agents get this wrong regularly, and the mistake costs clients coverage.

- Track terminations across your book. If three clients call about the same medical group in the same week, you have a market event, not three isolated incidents. Get ahead of the next 15 calls.

The Call, Reframed

A mid-year doctor drop feels catastrophic to the client because it is the first time the abstract concept of a "network" has bitten them. The agent's job is not to promise a rescue that CMS does not offer. It is to run the verification, read the notice, distinguish a real termination from a negotiation, protect them from a panic switch, and stage them for the correct window — OEP, 5-star, an exceptional-circumstance escalation, or a GI-triggered Medigap move — with clean paperwork ready to go. The clients who feel best served after these calls are not the ones whose agents magically produced an SEP. They are the ones whose agents had a plan.