What Counts as Creditable Coverage? 5 Sources Agents Themselves Get Wrong

-

May 28, 2026

We put a simple question to the Medicare Agents Hub community: Can you explain what creditable coverage means and when it applies?

Fifty-one licensed agents answered. Most got the broad definition right. But when the answers moved past the textbook and into specifics, a pattern emerged. Agents were confidently listing coverage sources as creditable or non-creditable, and a striking number of them were wrong.

Not vaguely wrong. Specifically, demonstrably wrong on sources they advise clients about every day: VA benefits, COBRA, retiree plans, Marketplace coverage, TRICARE, and FEHB.

This isn't a gotcha piece. It's a training resource built from what agents actually said, in their own words, to show where the field is splitting on questions that have clear CMS answers.

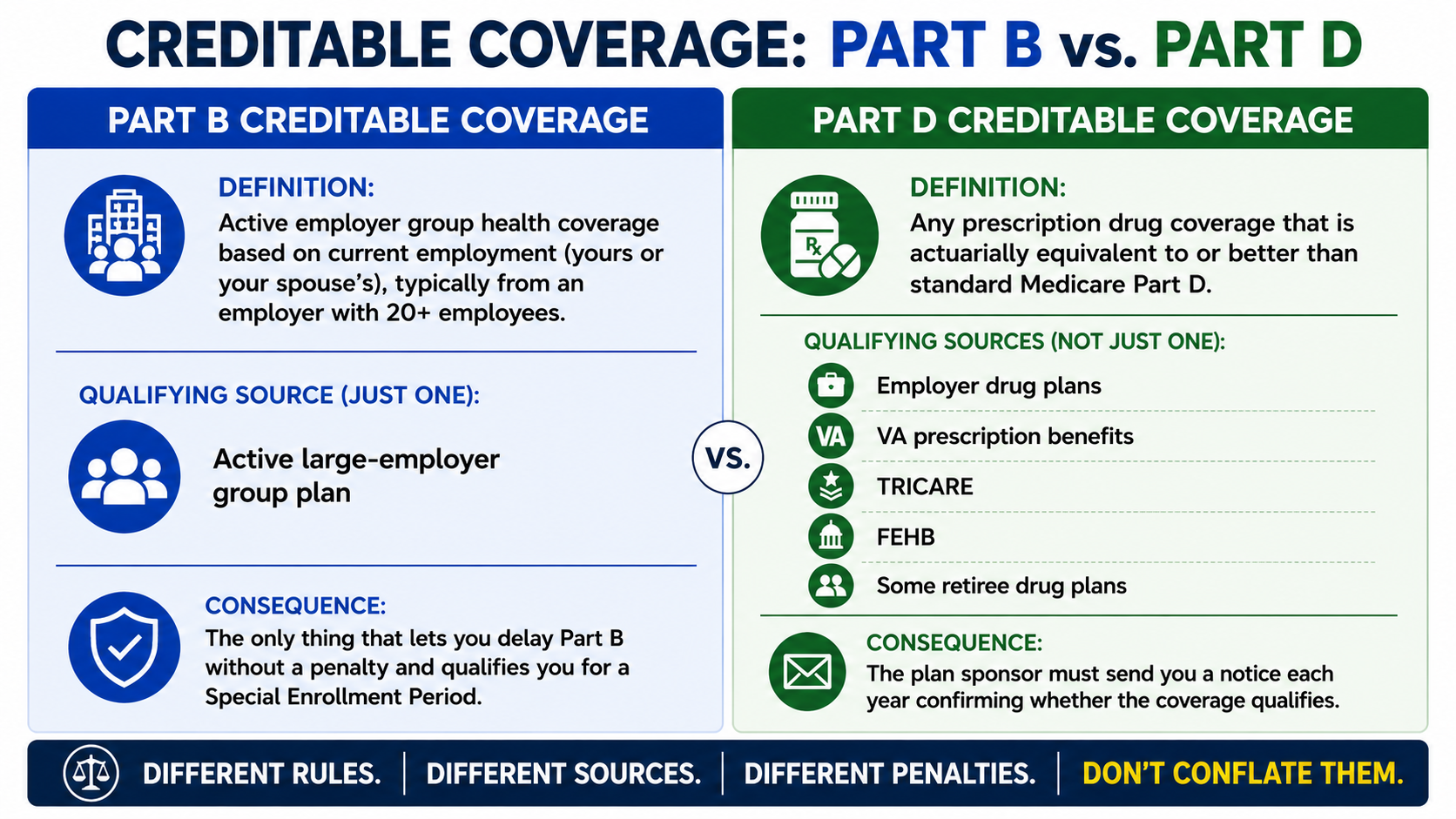

The Distinction That Separates Pros From Everyone Else

Before getting to the five disputed sources, there's a foundational problem running through most of the 51 answers: agents treat "creditable coverage" as one thing. It isn't.

Creditable coverage means something different for Part B than it does for Part D. The rules are different, the qualifying sources are different, and the penalties are different. Conflating the two is where most of the confusion starts.

Part B Creditable Coverage

For Part B, creditable coverage means active employer group health coverage based on current employment (yours or your spouse's), typically from an employer with 20 or more employees. This is the only thing that lets you delay Part B without a penalty and qualifies you for a Special Enrollment Period when you leave.

That's a narrow definition. One source. Current employer coverage from a large enough employer. Full stop.

Part D Creditable Coverage

For Part D, creditable coverage is broader: any prescription drug coverage that is actuarially equivalent to or better than standard Medicare Part D. This includes employer drug plans, VA prescription benefits, TRICARE, FEHB, some retiree drug plans, and others. The plan sponsor is required to send you a notice each year telling you whether the coverage qualifies.

Only one agent out of 51 laid this out cleanly with both sides separated:

Can you explain what "creditable coverage" means and when it applies?

Absolutely—this term causes a lot of confusion, and it means different things depending on the situation. Let’s make it clean and practical.⸻

What “Creditable Coverage” means (plain English)

Creditable coverage is health or drug coverage that Medicare considers “good enough” so you’re not penalized when you enroll later.

It mainly applies in two specific Medicare contexts:

1. Medicare Part B (medical)

2. Medicare Part D (prescription drugs)

Outside of those, the word gets misused a lot.

⸻

1. Creditable Coverage for Medicare Part B

This applies when you delay Part B.

Creditable coverage for Part B =

• Active employer group health coverage

• From current employment (yours or your spouse’s)

• Usually from an employer with 20+ employees

Why it matters

If you have this kind of coverage:

• You can delay Part B without penalty

• You qualify for a Special Enrollment Period (SEP) later

What does NOT count for Part B

❌ COBRA

❌ Retiree coverage

❌ Marketplace (ACA) plans

❌ VA coverage (for Part B purposes)

❌ Medigap or Medicare Advantage

Only current, active employer coverage counts here.

⸻

2. Creditable Coverage for Medicare Part D

This is the most common use of the term.

Creditable drug coverage means:

• Prescription coverage that is at least as good as a standard Medicare Part D plan

Examples that often count

✅ Employer or union drug plans

✅ VA prescription benefits

✅ TRICARE

✅ Some retiree plans

Each year, the plan must send a Creditable Coverage Notice telling you whether it qualifies.

Why it matters

If you go:

• 63 days or more without creditable drug coverage after Medicare eligibility,

• You can get a lifetime Part D penalty

⸻

3. What “creditable coverage” does NOT mean

This is the key misunderstanding:

🚫 Creditable coverage does NOT automatically:

• Give you Guaranteed Issue rights for Medigap

• Replace Medicare

• Mean you can enroll anytime

That answer is the standard every agent should be working from. If you can't explain the Part B vs. Part D distinction to a client in under 30 seconds, the five sections below will show you why that matters.

Source #1: VA Benefits

This is the single most confused source in the thread. Agents gave three different answers about VA coverage, all stated with equal confidence.

What agents said

One agent listed VA benefits as non-creditable alongside COBRA and retiree insurance:

"Examples of Non-Creditable Coverage for Medicare would be: COBRA, Retiree Insurance, VA Benefits, ChampVA, Tricare, Federal Employee Health Benefits (FEHB)."

Another flatly stated VA doesn't count:

Can you explain what "creditable coverage" means and when it applies?

Creditable coverage means your group health insurance is at least as good as Medicare. To qualify, you must be actively working for an employer with 20 or more employees.This matters if you delay enrolling in Medicare beyond your initial eligibility at age 65, often because you’re still working and covered by your employer’s plan.

Coverage that does NOT count as creditable includes:

• COBRA

• VA benefits

• Health sharing ministries

Meanwhile, a third agent went the opposite direction, claiming VA coverage exempts you from both Part B and Part D penalties:

"If you are a VA or Native American. You are exempt from Part B fines and Part D fines when you have credible coverage."

What CMS actually says

All three of those answers are wrong.

- VA prescription drug coverage IS creditable for Part D. Veterans who receive their medications through the VA can delay Part D enrollment without a penalty.

- VA healthcare is NOT creditable for Part B. VA coverage does not trigger a Special Enrollment Period, does not prevent the Part B late enrollment penalty, and does not satisfy the "current employer coverage" requirement.

A veteran who relies solely on VA healthcare past age 65 and later decides to enroll in Part B will pay the 10%-per-year penalty for every full 12-month period they could have enrolled but didn't. The VA benefit is free, so many veterans don't feel the urgency, but the penalty is permanent if they ever leave the VA system.

Source #2: COBRA

COBRA is the most dangerous source on this list because agents who get it wrong are giving clients advice that leads directly to a lifetime penalty.

What agents said

One agent shared what happens when clients assume COBRA protects them:

Can you explain what "creditable coverage" means and when it applies?

He's right that COBRA doesn't protect you from Part B penalties. But the blanket statement "COBRA is not creditable coverage" is too broad, and other agents in the thread made the same overgeneralization.

What CMS actually says

- COBRA is NOT creditable for Part B. It does not count as "coverage based on current employment." It does not trigger a Special Enrollment Period. It does not prevent the Part B late enrollment penalty. The 8-month SEP window starts when your employment ends or your employer coverage ends, whichever comes first. COBRA doesn't pause that clock.

- COBRA prescription drug coverage CAN be creditable for Part D, if the drug benefit meets the actuarial equivalence standard. Many COBRA plans do. The plan administrator is required to send a notice.

The L564 trap

Here's where COBRA catches agents off guard. When a client leaves employer coverage and enrolls in Medicare, Social Security uses Form CMS-L564 (Request for Employment Information) to verify they had creditable coverage based on current employment. The employer fills this out.

COBRA continuation does not satisfy the L564. If a client stayed on COBRA for 18 months after leaving their job and then tries to enroll in Part B, the L564 will show their employment ended 18 months ago. Their SEP started then, not when COBRA expired. If they're past the 8-month window, they're looking at a permanent Part B penalty.

The correct advice for any client aging into Medicare while on COBRA: enroll in Part B immediately. Don't wait for COBRA to expire. The SEP clock is already running.

Source #3: Retiree Coverage

Retiree health plans sit in the same gray zone as COBRA, and agents split on them for the same reason: they're real insurance that feels like it should count.

What agents said

One agent listed retiree insurance as explicitly non-creditable. Another said employer and "certain retiree plans" count as creditable for Part D. Both are partially right.

What CMS actually says

- Retiree coverage is NOT creditable for Part B. By definition, retiree coverage is not based on current employment. It doesn't qualify you for a Part B SEP and doesn't prevent the Part B penalty.

- Retiree prescription drug coverage CAN be creditable for Part D. Many retiree drug plans meet the actuarial equivalence standard. The plan sponsor is required to send the annual creditable coverage notice. If it qualifies, the retiree can delay Part D without penalty.

The critical question for any client with retiree coverage: Did your former employer send you a creditable coverage notice for your drug benefit? If yes, Part D can wait. If no, or if the notice says "non-creditable," that client needs a Part D plan and the 63-day clock is ticking.

Source #4: Marketplace (ACA) Plans

This one should be straightforward, but one agent in the thread got it exactly backwards.

What agents said

"Creditable coverage is basically any healthcare plan you get through the Affordable Care Act marketplace or through an employer."

That answer puts ACA marketplace coverage on the same level as employer coverage. It's wrong on both counts.

What CMS actually says

- Marketplace plans are NOT creditable for Part B. They are individual plans, not employer group coverage based on current employment.

- Marketplace plans are NOT creditable for Part D. ACA plans are not designed to coordinate with Medicare and do not meet the Part D actuarial equivalence standard.

- Marketplace subsidies end when you become Medicare-eligible. Continuing a Marketplace plan after Medicare eligibility is almost always a financial mistake. You lose the premium tax credit, you're paying full price for a plan that doesn't prevent Medicare penalties, and you're accumulating penalty months with every passing quarter.

This is one of the highest-stakes errors an agent can make. A client who stays on a Marketplace plan past 65 because their agent called it "creditable" will face both Part B and Part D late enrollment penalties when they eventually switch, and those penalties are permanent.

Source #5: TRICARE and FEHB

One agent listed both TRICARE and FEHB as non-creditable in the same sentence as COBRA and VA. That answer was wrong on every source except COBRA (for Part B).

What agents said

"Examples of Non-Creditable Coverage for Medicare would be: COBRA, Retiree Insurance, VA Benefits, ChampVA, Tricare, Federal Employee Health Benefits (FEHB)."

What CMS actually says

TRICARE for Life:

- TRICARE for Life requires Medicare Part A and Part B enrollment. It's not a question of whether TRICARE is creditable; it's a prerequisite.

- TRICARE prescription drug coverage IS creditable for Part D. Military retirees with TRICARE do not need a separate Part D plan and will not face penalties.

Federal Employee Health Benefits (FEHB):

- FEHB is one of the most generous coverage situations in Medicare. Federal retirees can keep FEHB alongside Medicare, and FEHB works as secondary coverage to Medicare.

- FEHB prescription drug coverage IS creditable for Part D. Federal employees and retirees do not need a standalone Part D plan.

- For Part B, active federal employees with FEHB have creditable coverage. Federal retirees on FEHB should still enroll in Part B at 65, because FEHB pays more when Medicare is the primary payer.

Telling a federal retiree or military retiree that their coverage is "non-creditable" is not just incorrect. It could push them into unnecessary plan purchases or cause them to panic about penalties that don't apply to them.

The Annual Notice Obligation

Several agents in the thread mentioned the creditable coverage notice, but most glossed over the mechanics. Here's what agents need to know to advise clients correctly:

- Who sends it: Any entity providing prescription drug coverage to Medicare-eligible individuals. This includes employers, unions, FEHB, VA, and retiree plan sponsors.

- When: Before October 15 each year (before the start of Medicare Open Enrollment), and whenever coverage changes.

- What it says: The notice states whether the plan's drug coverage is creditable (at least as good as Part D) or non-creditable. This is the definitive answer for that plan year.

- What to tell clients: Keep every notice. If they never received one, contact the plan administrator and request it in writing. If the plan is non-creditable, they need Part D coverage and the 63-day gap clock applies.

Agents who collect the right documentation from clients upfront should be asking for this notice at intake. It's not optional information. It determines whether the client has a problem or doesn't.

The 60-Second Discovery Script

Here are five questions that will nail down a client's creditable coverage status in under a minute. Agents who ask all five before discussing plan options will avoid every mistake described above.

1. "Are you currently working, or is your spouse currently working?"

This is the Part B gate. If the answer is no, Part B creditability is off the table regardless of what other coverage they have.

2. "How many employees does that employer have?"

20 or more = creditable for Part B. Under 20 = Medicare is primary and the employer plan is secondary, even if they're still working. Different rules apply.

3. "Is that active group coverage, COBRA, or retiree coverage?"

Only active group coverage counts for Part B. If they say COBRA or retiree, shift immediately to Part D and penalty prevention.

4. "Do you have VA benefits, TRICARE, or FEHB?"

All three are creditable for Part D. None of them (except active-duty FEHB) are creditable for Part B. Knowing which they have tells you what they still need.

5. "Do you have the creditable coverage notice your plan sent you?"

If they have it and it says creditable, Part D can wait. If they don't have it or it says non-creditable, you need to act on Part D now. This is the document that settles all arguments.

Five questions. Under a minute. Every disputed source covered. Compare that to the 51 answers in the original thread, where agents spent paragraphs defining "creditable coverage" in the abstract without ever asking the questions that determine whether a specific client's coverage actually qualifies.

The Cheat Sheet

| Coverage Source | Creditable for Part B? | Creditable for Part D? | Notes |

|---|---|---|---|

| Active employer group (20+ employees) | Yes | If notice says yes | The only source that delays Part B without penalty |

| Active employer group (<20 employees) | No (Medicare is primary) | If notice says yes | Must enroll in Part B at 65 |

| COBRA | No | Possibly (check notice) | SEP clock starts at employment end, not COBRA end |

| Retiree coverage | No | Possibly (check notice) | Not based on current employment |

| Marketplace / ACA | No | No | Subsidies end at Medicare eligibility |

| VA benefits | No | Yes | No Part B SEP; penalty applies if enrolling late |

| TRICARE for Life | Requires Part B | Yes | Must have both Part A and Part B to keep TFL |

| FEHB (active employee) | Yes | Yes | Part B still recommended for maximum benefit |

| FEHB (retiree) | Should enroll in Part B | Yes | FEHB pays more with Medicare as primary |

| Hospital indemnity | No | No | Supplemental only; not a medical or drug plan |

Print this. Tape it next to your monitor. Reference it before every enrollment conversation with a client who has coverage from any source other than a straightforward large-employer group plan.

Why This Matters

Creditable coverage isn't an abstract concept. It's the mechanism that determines whether your client pays a permanent penalty or doesn't. Getting it wrong once, on one client, costs that person money every month for the rest of their life.

Fifty-one agents answered this question on Medicare Agents Hub. The ones who got it right separated Part B from Part D, named specific sources, and stated the rules for each. The ones who got it wrong treated creditable coverage as a single yes-or-no label and then applied it to the wrong sources.

The fix isn't complicated. Learn the Part B vs. Part D distinction. Memorize which sources apply to which. Ask the five discovery questions before you recommend anything. And when you're not sure, ask for the notice. That one piece of paper answers the question every time.

If you want to see how real seniors end up paying lifelong penalties, or brush up on how the Special Enrollment Period works after losing employer coverage, those resources break down the client-side consequences of the mistakes covered here.