Clear Spring Health’s Medicare Advantage Exit: SEP Questions, PDP Fallback Risks, and Broker Takeaways

-

May 9, 2026

Clear Spring Health MA Exit

Clear Spring Health’s mid-year Medicare Advantage exit has created an unusually compressed transition window for affected members and the brokers who serve them with coverage ending May 31, 2026, and gives agents until July 31, to use the Special Enrollment Period, leaving agents a short window to help clients move into new coverage. The problem: many brokers are still trying to confirm the correct SEP mechanics, submission codes, and fallback PDP implications.

Editor's note: This article is based on a publicly shared broker notice and subsequent discussion among Medicare industry professionals. Agents should verify client-specific deadlines, SEP instructions, and submission rules through the official carrier notice, CMS/Medicare.gov guidance, and their enrollment platforms before taking action.

The following industry reactions are commentary, not official enrollment guidance.

The news surfaced when Sam Melamed, CEO of NCD, shared details from what he described as an urgent broker notice on LinkedIn. According to Melamed, Clear Spring Health is "shutting down their Medicare Advantage plans immediately," with members being terminated at the end of May.

"They are not leaving their members with much time to find a new alternative," Melamed wrote.

The broker notice reportedly stated that coverage for clients enrolled with effective dates between June 1 and August 1, 2026 will not go into effect. Brokers were instructed to begin transitioning current members to new coverage with a June 1 effective date, with a SEP window running June 1 through July 31. Members who don't choose a new plan will revert to Original Medicare and be auto-enrolled in a Humana Basic Rx PDP at $0 premium.

Melamed said he believed Clear Spring Health was still taking enrollments in Colorado, Georgia, and Illinois after exiting other markets in 2025. While enrollment was relatively small, he estimated "definitely thousands of beneficiaries will be affected."

The post quickly became a broader industry conversation about member disruption, SEP mechanics, carrier economics, and whether more regional MA plans face similar pressure.

The Compressed Timeline

MA carriers almost never exit mid-year. Marie Rosenberg pointed out in the thread that "MA carriers almost always exit at calendar year-end, not mid-year." She speculated the move likely pointed to "a voluntary contract termination approved by CMS, financial/regulatory issues, or extremely low enrollment making continuation unworkable."

For agents, the compressed timeline creates an immediate service challenge: identify affected clients, interpret the carrier notice, explain the SEP, compare replacement options, and prevent clients from falling into coverage that doesn't fit their needs. All within weeks.

Broker takeaway: This is not just a carrier exit story. It is a client-retention, prescription-access, and service-continuity issue.

SEP Mechanics: Agents Still Need Clear Submission Guidance

Justin Brock, CEO of Brock Partners, asked directly: "What SEP can agents use for these mid-year plans?" He suggested it "seems like loss of creditable coverage," while Tyler Johnson, a healthcare sales and distribution executive, responded: "SEP-Contract Termination."

Brock then asked whether agents would write it in OTH. Johnson replied, "I guess so. I don't see it specified in any platforms."

That exchange captures a real operational problem. The carrier notice says members have a SEP from June 1 through July 31, but agents still need to confirm the correct election period code, platform instructions, carrier-specific guidance, and documentation requirements before submitting applications. When experienced industry professionals are publicly asking each other how to handle the enrollment, it suggests the operational guidance has not yet been clear enough for the field.

The Fallback PDP Isn't a Safety Net

On paper, auto-enrollment into a $0 premium Humana Basic Rx PDP sounds like a reasonable default. In practice, several commenters warned that the fallback could create problems for members who don't act.

One commenter wrote that "the real issue isn't the fallback itself" but that "most people won't shop during SEP." He warned that thousands could end up in a PDP that doesn't match their formulary or network needs, and that "gaps in medication access don't surface until someone's at the pharmacy counter in July, prescription denied."

A $0 premium doesn't mean appropriate coverage. It may not cover a member's prescriptions, may place drugs on unfavorable tiers, may exclude a preferred pharmacy, or may create unexpected access problems. The risk isn't losing a Medicare Advantage plan. The risk is assuming the default is good enough without reviewing prescriptions, pharmacies, providers, and total out-of-pocket exposure.

This is where proactive agent outreach after plan disruptions can make a real difference.

Broader MA Market Pressure

The conversation expanded beyond Clear Spring Health into the state of the Medicare Advantage market itself.

Daniel Hardle, President of Agent Boost Marketing, said Clear Spring Health was "following in the footsteps of Sonder, Atrio... and others" and predicted "a few more small local and regional MA plans doing the same before the end of this year." He pointed to "higher MLRs, higher risk, different rate environment and headwinds that didn't exist 3 years ago."

Jennifer Melreit, National Director of Agency Relationships at Advocu, framed it as a systemic issue: "Concerning to see reductions in options and carriers leaving. Speaks to the overall pressures on the industry." She argued all stakeholders need to play a role, from CMS properly funding the program to carriers offering economically viable plans to brokers providing quality post-enrollment support.

Melreit also had a direct message for carriers: "Kindly do not put out a plan if you do not want members on the plan and if you can not pay a commission."

That frustration reflects a broader concern: members and brokers are left to manage the disruption when carrier strategy changes, plan economics break down, or products are withdrawn.

Star Ratings and Financial Viability

Graham Smith commented he was "honestly surprised they lasted this long" after CMS terminated the company's PDP plans for low star ratings, which he said had been the majority of their revenue.

John Norce raised a related financial point: it's "hard to make a profit on payments based on 2.5 stars." The extra payment associated with a 4-star plan can make a significant difference when margins are already tight. Norce also wondered whether CMS may have been moving toward terminating the plan for poor performance, potentially triggering the mid-year action.

For agents, this becomes relevant at recommendation time. A plan's star rating, financial health, prior market exits, and operational track record are all signals worth weighing when evaluating which Medicare Advantage plans to recommend.

Was This Predictable?

Not everyone was surprised. Chris Prang, who identifies as The Medicare Analyst, replied that it "should not have come as a surprise" and said "the writing was on the wall for years."

That highlights a tension in the industry. Agents may notice patterns: declining plan quality, market exits, low ratings, operational problems. Members don't see those warning signs. They enrolled in a plan and expected it to last the year.

That gap is one reason agent guidance matters beyond the initial sale. Carrier stability, service history, network reliability, and plan performance can all become part of the recommendation conversation.

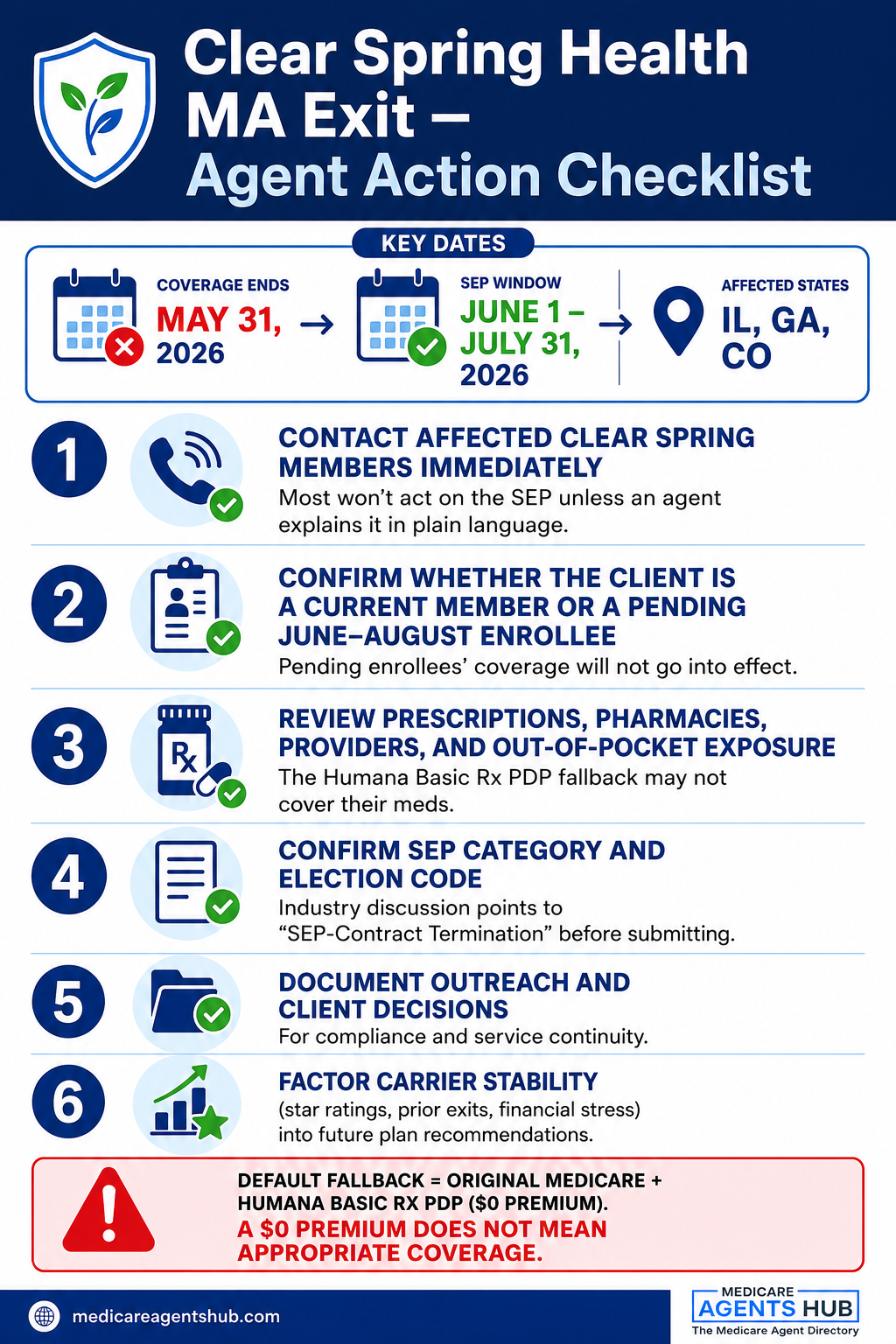

Agent Action Checklist

If you have clients on Clear Spring Health, here's what to do now:

- Contact affected Clear Spring members immediately. Don't wait for members to understand the notice on their own. Most won't act during the SEP window unless someone tells them what's happening in plain language.

- Confirm whether the client is a current member or a pending June through August enrollee. Pending enrollees face a different situation since their coverage will not go into effect.

- Review prescriptions, pharmacies, providers, and total out-of-pocket exposure. The Humana Basic Rx PDP fallback may not cover their medications appropriately. Check formulary, tiers, and preferred pharmacy access before assuming the default is acceptable.

- Confirm SEP and election code instructions before submitting. The thread showed even experienced professionals debating how the election should be categorized. Verify the correct SEP category, election code, effective date rules, documentation requirements, and whether each receiving carrier has issued its own submission instructions.

- Document outreach and client decisions. Track your communication with each affected member and their enrollment choices for compliance and service continuity.

- Factor carrier stability into future recommendations. Low star ratings, prior market exits, financial stress, and operational red flags deserve more weight when comparing plans for clients.

As Matt Buchan, Co-Founder and CEO at ExactBenefits.com, wrote in the thread: "Very unfortunate. Moments like this are a reminder that behind every policy is a real person depending on stability and access to care."

Members who were recently enrolled with effective dates between June 1 and August 1 face particular confusion. Their policies will not go into effect, meaning they need to start over without necessarily understanding why. Current members have a short window before being moved into fallback coverage that may not fit.

Frequently Asked Questions

When does Clear Spring Health Medicare Advantage coverage end?

Coverage ends May 31, 2026. Clear Spring Health announced it will discontinue its MAPD plans in Illinois, Georgia, and Colorado effective June 1, 2026. Members enrolled with effective dates between June 1 and August 1 will not have their coverage go into effect at all.

What happens if affected members do nothing?

Members who do not select a new plan during the SEP will revert to Original Medicare and be auto-enrolled in the Humana Basic Rx PDP at a $0 premium. While that prevents a total gap in drug coverage, the fallback plan may not cover their current medications, may place drugs on unfavorable tiers, or may exclude their preferred pharmacy.

What Special Enrollment Period applies to Clear Spring Health members?

Affected members have a Special Enrollment Period running from June 1 through July 31, 2026. Industry discussion suggests the applicable SEP category is contract termination, though agents should confirm the correct election period code and submission instructions with each receiving carrier before submitting applications.

Why might the Humana Basic Rx fallback plan not be enough?

A $0 premium does not mean appropriate coverage. The fallback PDP may not include a member's prescriptions on its formulary, may assign them to higher cost-sharing tiers, or may not include their preferred pharmacy in its network. Members who were on a Medicare Advantage plan also lose any MA-specific benefits like dental, vision, hearing, or lower out-of-pocket maximums when they revert to Original Medicare.

What happens to medications that aren't on the new plan's formulary?

According to Clear Spring Health's member FAQ, members are entitled to a 30-day transition supply of their current medications within the first 90 days if those drugs are not on the new plan's formulary or are restricted by utilization management such as prior authorization, quantity limits, or step therapy. Members who receive a transition fill will get a letter within three business days explaining it is a temporary supply and outlining next steps. Agents should make sure clients understand this is a bridge, not a permanent solution, and work with the member's prescriber on a coverage determination or formulary alternative.

Do prior authorizations from Clear Spring Health transfer to the new plan?

No. Approvals from Clear Spring Health do not automatically transfer to a new plan. For medical care already planned after May 31, 2026, the member's provider can still deliver care under Original Medicare or a new Medicare Advantage plan, but a new prior authorization may be required. Agents should flag this for any client with upcoming procedures, specialist visits, or ongoing treatment that required prior auth under Clear Spring.

Does Part D out-of-pocket spending carry over to the new plan?

Yes. In 2026, total out-of-pocket costs for Part D covered drugs are capped at $2,100 for the year. Clear Spring Health's member FAQ confirms that the amount a member has already spent year-to-date will transfer to the new plan, so they do not restart tracking toward the $2,100 limit. Monthly premiums do not count toward the cap. This is a useful detail to share with members who may be worried about losing credit for what they have already paid.

Affected members should rely on their official carrier notice, Medicare.gov, or guidance from a licensed agent to confirm their specific options and deadlines. As of publication, the details in this article are based on the broker notice described above and public industry discussion, not an official CMS announcement.

This situation is a reminder that post-enrollment support isn't optional. A member's relationship with their agent can't end when the application is submitted. When a plan exits mid-year, that relationship is what stands between a member and a coverage gap they didn't see coming.

Reviewed by a licensed Medicare insurance agent and the Medicare Agents Hub editorial team using publicly available broker discussion and industry source material. Agents should confirm final enrollment guidance through official carrier and CMS channels.