The Two Million: Inside the Quiet Medicare Advantage Disenrollment Wave Agents Don't Talk About on TV

-

April 7, 2026

Two Million Displaced and Counting

In 2025, roughly two million seniors were involuntarily removed from their Medicare Advantage plans. Carriers pulled unprofitable products from entire counties, dropped PPO options in favor of leaner HMOs, and slashed benefits to stay solvent. It happened quietly. No press conferences, no primetime coverage. Just letters in mailboxes and confused phone calls to agents.

For Medicare agents, this is not just a plan-disruption story. It is a retention, compliance, and book-of-business issue.

One experienced agent on Medicare Agents Hub said they have stopped selling Advantage plans altogether. Year after year, hospital systems pull out and carriers drop clients from their plans. In 2025 alone, two million seniors were displaced. That agent now steers every client toward Medigap Plan G and a standalone Part D.

This is not an isolated opinion. Other agents have described the same pattern repeating across multiple years, with hospital systems nationwide withdrawing from Medicare Advantage plans in both 2024 and 2025.

The numbers tell a story the industry has been slow to acknowledge. And the structural forces behind this wave, including MA plan exits and ongoing Medicare Advantage network changes, are not slowing down.

Why are people leaving Medicare Advantage plans?

People leave Medicare Advantage plans for a few recurring reasons:They want broader provider choice. Many Medicare Advantage plans use provider networks, and people may switch if their doctors or hospitals are out of network or if they travel and want fewer network limits.

They run into prior authorization or coverage denials. Some members leave after delays or hassles getting approvals for services, rehab, imaging, or certain drugs.

Costs become less predictable than expected. Even with low or $0 premiums, members can face copays/coinsurance that add up, higher costs for frequent care, and hitting the plan’s annual out-of-pocket maximum.

Their plan changes from year to year. Networks, drug formularies, premiums, and cost-sharing can change annually, and a “good” plan one year may fit poorly the next.

They prefer Original Medicare’s structure. Some people switch because they want fewer plan rules, easier use of out-of-area providers, or the option to pair Original Medicare with a Medigap policy (when available/affordable).

They feel they enrolled based on confusing marketing. Some beneficiaries later realize key limitations (like networks or prior authorization) were not fully understood at sign-up.

One important caution is that switching from Medicare Advantage to Original Medicare does not always guarantee you can buy a Medigap plan without medical underwriting, depending on your state and timing.

CMS Finalized a Higher 2027 MA Increase, But Pressure Remains

CMS initially proposed a near-flat 0.09% average payment increase for Medicare Advantage carriers in the 2027 Advance Notice. That number sent shockwaves through the industry. On April 6, 2026, CMS finalized a 2.48% average increase for 2027, a meaningful bump from the initial proposal.

Even with the higher final rate, agents who closely track the payment landscape are not breathing easy. Healthcare inflation still runs well above 2.48%, and the gap between what carriers receive and what providers demand continues to widen. The math is better than the Advance Notice suggested, but it still does not fully close the gap.

For context, the typical responses to payment pressure are predictable and already underway in many markets.

- Network contraction: Carriers drop providers or entire medical groups to reduce claims exposure

- Benefit reduction: OTC allowances, dental, and transportation benefits get trimmed or eliminated

- Market exit: Carriers pull plans from unprofitable counties or states entirely

- Plan type shifts: PPOs get replaced by more restrictive (and cheaper to administer) HMOs

Agents familiar with the dynamics have confirmed the typical reasons behind Medicare Advantage plan termination: carriers pulling out of a county or even a state, replacing PPO options with HMO-only offerings, and reducing plan benefits to protect profitability. The finalized 2.48% increase may slow the pace of these changes, but it does not reverse the trend.

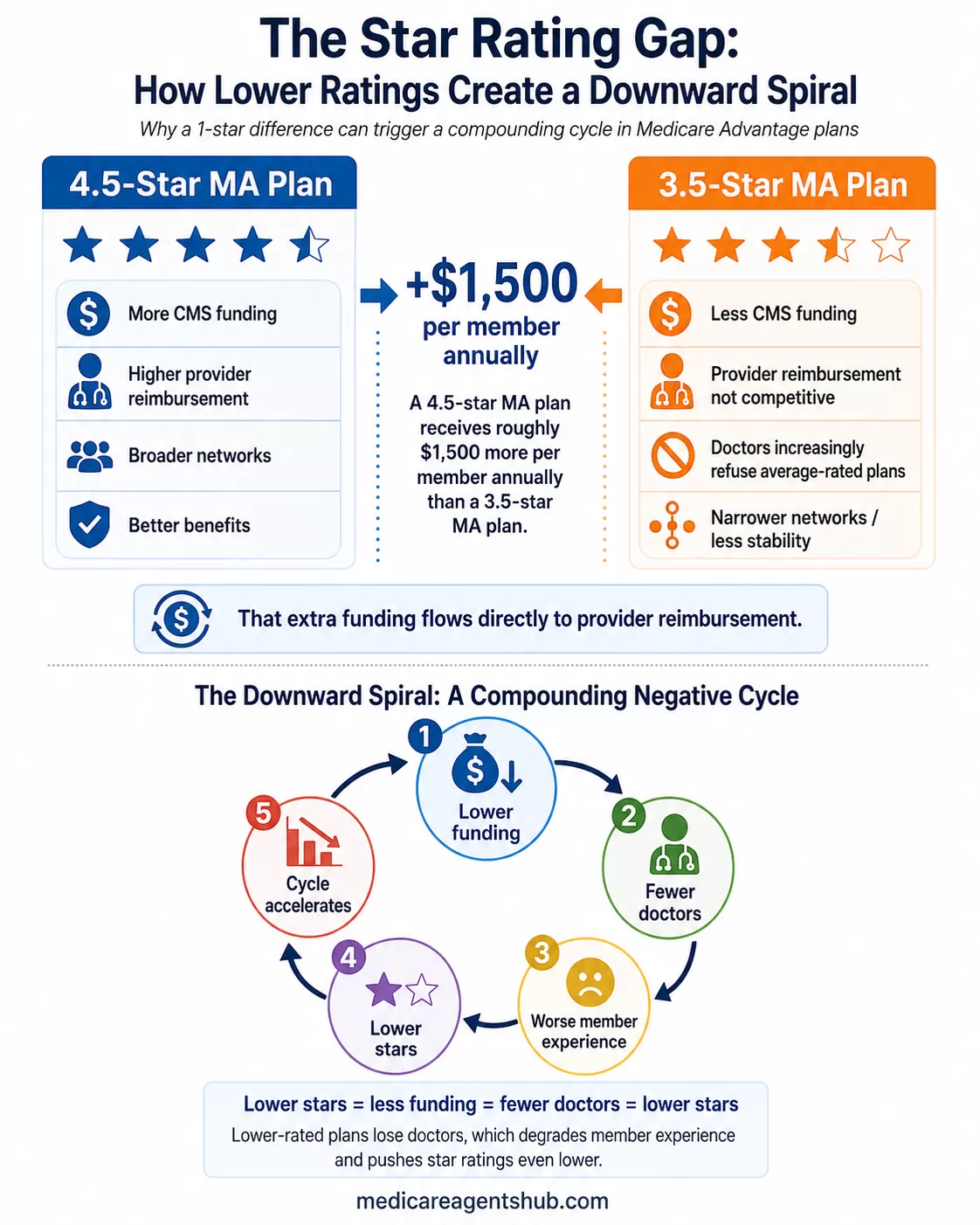

The Star Rating Gap: $1,500 Per Patient

Not all plans are feeling the squeeze equally. CMS pays higher-rated plans significantly more, and that gap has real consequences for provider networks.

Agents tracking the payment structure point to a stark reality: plans rated 4 stars or higher receive substantially more from CMS, and that money flows directly to provider reimbursement. A 4.5-star plan can receive roughly $1,500 more per member annually for healthcare management than a 3.5-star plan. That difference translates directly into what carriers can pay doctors.

This creates a compounding effect. Higher-rated plans can afford to maintain broader networks and better benefits. Lower-rated plans lose doctors, which degrades the member experience, which pushes star ratings even lower. The cycle accelerates.

From the provider side, the incentives are clear. Doctors who accept lower-rated plans get reimbursed less and deal with more administrative friction. Several agents have noted that providers are increasingly unwilling to accept average-rated plans because the reimbursement simply is not competitive.

How do Medicare Advantage star ratings affect the quality of care I can expect?

Probably not as much as people expect.Medicare Advantage star ratings aren’t like Google reviews. They’re not based on free-form feedback from members or a simple measure of how happy people are with their care. Instead, they’re built from a long list of government-defined metrics — things like preventive care compliance, administrative processes, and certain health outcomes.

Those metrics also change over time. We’ve seen the emphasis shift from one administration to the next, which means star ratings can reflect policy priorities as much as real-world care delivery.

There’s also a big financial angle. Insurance carriers have strong incentives to hit whatever benchmarks the government sets, because higher star ratings mean bonus payments. That motivates compliance — but compliance doesn’t always equal better doctor visits.

All that said, star ratings aren’t meaningless. A plan with very low ratings is usually a red flag, and a true 5-star plan is probably doing a lot of things right. Where it gets fuzzy is the large middle ground. For most people, a 3½- or 4-star rating doesn’t tell you much about the quality of care you’ll personally receive.

That’s because your care experience still depends far more on the doctors, hospitals, and provider network than on the insurance company behind the plan. Star ratings can be a useful data point — but they shouldn’t be the deciding factor.

For agents, the practical takeaway is worth noting: steering clients toward higher-rated plans is not just about member satisfaction anymore. It is increasingly about network stability and continuity of care. If you are curious about what the broader growth of Medicare Advantage means for your practice, the star rating gap should be a central part of that analysis.

When Doctors Walk Away: The Network Exit Problem

The payment squeeze does not stay abstract for long. It shows up in provider directories. Doctors and hospital systems are leaving MA networks at a pace that multiple agents described as unprecedented.

In the Pacific Northwest, major health systems like Multicare and Providence have stopped accepting PPO plans in markets like Spokane. When systems that large exit, the ripple effects hit every agent with clients in that market.

The administrative burden compounds the problem. Agents report that many providers are dropping MA plans not just because of pay, but because of the prior authorization requirements and slow payment timelines that strain a practice's cash flow. For some providers, the combination of lower reimbursement and heavier paperwork simply is not worth it.

The reimbursement picture is stark. In many cases, doctors treating MA patients receive roughly 90% of what Original Medicare would pay for the same services. Combined with prior authorization requirements and slower payment timelines, some providers are simply opting out.

For clients currently on MA plans, mid-year network exits create real disruption. Providers are contracted with plans on varying timelines, and when a contract ends mid-year, a PPO member may face out-of-network copays while an HMO member could be forced to switch specialists entirely.

Why do doctors not like Medicare Advantage plans?

Here is why your doctor might have a "love-hate" (mostly hate) relationship with them:1. The "Prior Authorization" Paperwork

This is the number one complaint. In Original Medicare, if a doctor says you need an MRI or a specific surgery, you generally just get it.

The MA Reality: Private insurers often require "prior authorization" for services. This means your doctor’s staff must spend hours submitting paperwork to prove the service is necessary.

The Friction: In 2026, even with new laws requiring faster decisions (7 days for routine, 72 hours for urgent), doctors still find this an administrative nightmare that delays your care and increases their overhead costs.

2. Higher Denial Rates

Doctors get frustrated when they prescribe a treatment plan only to have an insurance company’s algorithm or remote medical reviewer deny it.

The Conflict: Studies consistently show that MA plans deny a higher percentage of claims than Original Medicare. When a claim is denied, the doctor either doesn't get paid or has to engage in a lengthy, unpaid appeals process to fight for your treatment.

3. "Narrow" Networks

Medicare Advantage plans save money by limiting you to a specific "network" of doctors.

The Doctor's Perspective: This makes referrals difficult. If your primary care doctor wants to send you to the best specialist in the city, but that specialist isn't in your plan's network, the doctor has to hunt for a "second-best" option that is covered. This limits their ability to provide what they consider the highest quality of care.

4. Reimbursement Lag & Lower Pay

In 2026, the gap between what Medicare pays doctors and what it costs to run a practice has widened.

The Money Trail: While the government increased payments to MA insurance companies by about 4.3% for 2026, many doctors saw their actual reimbursement rates stay flat or even decrease.

The Result: Some hospitals are "dropping" certain MA plans entirely because the administrative cost.

The practical implication for agents: network stability should be part of every plan recommendation conversation, not an afterthought. If you are helping clients navigate these disruptions, you may also want to review the guidance in what to do when Medicare plans fail your client.

How Agents Are Repositioning

The disenrollment wave is not just a consumer problem. It is reshaping how agents build their practices. Several distinct strategies are emerging from the field.

The Supplement Pivot

Some agents have moved away from MA entirely. For these agents, the instability in MA networks has made Medigap the more defensible recommendation, especially for clients with established provider relationships. Their advice is straightforward: purchase a supplement Plan G and a standalone Part D, and sidestep the annual churn altogether.

Others frame it even more bluntly. When cost is not a barrier, traditional Medicare with a supplement wins hands down. Advantage plans carry too many drawbacks: networks that are harder to navigate than they should be, plan changes every year, and constant uncertainty about provider access. For agents weighing Medicare Advantage vs Medigap for their clients, the calculus has shifted noticeably.

What's your go-to strategy for helping someone decide between Medicare Advantage and Medigap?

Don’t choose based on the premium—choose based on how you want to access care.Medicare Advantage often looks attractive because of low or $0 premiums, but it typically comes with networks, referrals, and prior authorizations. Original Medicare with a supplement costs more monthly, but gives you maximum flexibility—no networks, fewer restrictions, and predictable out-of-pocket costs.

So the real question is:

Do you want freedom to see any doctor nationwide without referrals? → Lean Original Medicare + Medigap

Or are you comfortable with a managed network to save on monthly premiums? → Medicare Advantage

If someone makes the decision purely on premium, they often regret it when they actually need care.

The Star Rating Strategy

Other agents are staying in the MA space but being far more selective. The recommendation from agents tracking the payment landscape: get your clients into a high-rated plan or move them to a supplement. Carriers are already reducing benefits, and agents expect larger cuts next year across OTC allowances, dental, and other benefit types.

This aligns with the broader financial reality. High-star plans have more payment headroom and can maintain stronger networks. Agents who pay attention to star ratings and help clients understand their ANOC each fall are better positioned to catch plan degradation before it becomes a crisis.

The Network Verification Discipline

Across the board, agents are emphasizing more rigorous network checks. The new reality, as veteran agents describe it, is that medical providers come and go from networks constantly, and vigilance is no longer optional.

This is not just AEP due diligence anymore. With providers able to exit networks mid-year, agents are checking directories more frequently and building relationships with provider offices to get early signals about contract disputes.

The Compounding Effect: What Comes Next

The forces driving this wave are structural, not cyclical. Here is how the compounding works:

1. CMS pays carriers less (or barely more) in real terms

2. Carriers pay providers less or impose more administrative controls

3. Providers exit networks or refuse to accept new MA patients

4. Networks narrow, member experience declines

5. Star ratings drop, reducing future CMS payments

6. The cycle repeats, accelerating benefit cuts and market exits

Agents who have watched this play out over decades say the current pace of change is unlike anything they have seen. One 30-year veteran noted that the volume of plan changes heading into 2026, including hospitals and doctors leaving networks, major carriers pulling plans from markets, and out-of-pocket maximums jumping by double digits, is unprecedented in their career.

The policy dimension matters too. Agents point to the Inflation Reduction Act as a key driver behind the 2025 and 2026 disruptions. The IRA's restructuring of Part D benefits shifted costs to carriers, adding another squeeze on top of the flat CMS rate increases, and those provisions extend through at least 2027.

How is Medicare Advantage expected to evolve in the future?

There's no way to predict the future, but from talking with various carrier reps and folks in the industry it's entirely likely that the bells and whistles to the plans will be going away. There is finite amount of money the carriers have to spend on plans and they are more likely to allocate that money towards the medical benefits. That could mean that the Max out of pocket, premiums, copays, etc remain steady or they will be reduced.Every area is different so it's tough to say what it will look like everywhere.

For agents building long-term books of business, understanding this trajectory is essential. The market is not returning to the days of generous MA benefits and broad networks anytime soon. If you are thinking about how to build a book of business that lasts through these shifts, the answer increasingly involves diversification across product lines.

Practical Takeaways for Agents

The disenrollment wave is not a reason to panic. It is a reason to adapt. Here is what agents on the ground are doing.

- Check star ratings before recommending any MA plan. The payment gap between a 4.5-star and 3.5-star plan is significant enough to affect network stability and benefit sustainability.

- Verify networks more frequently. Annual checks at AEP are not sufficient when providers can exit networks any month of the year.

- Know the SEP triggers. When a plan is terminated or a significant network change occurs, clients may qualify for a Special Enrollment Period after plan termination. Be ready to act quickly.

- Have the Medigap conversation early. For clients approaching 65, discussing supplement options during their initial enrollment is more important than ever. The guaranteed issue window does not last forever.

- Track CMS payment announcements. The 2027 rate notice is a leading indicator of what benefits and networks will look like in the next plan year. Read the rate notices before carriers release their ANOCs.

- Communicate proactively. Clients displaced from their plans need to hear from their agent, not the carrier's 800 number. Proactive follow-up turns a disruption into a retention opportunity.

Frequently Asked Questions

Why are Medicare Advantage plans being discontinued?

Carriers discontinue MA plans when the CMS payment rates no longer support the cost of maintaining provider networks and benefits in a given market. Rising healthcare costs, flat or modest rate increases, and the financial impact of the Inflation Reduction Act on Part D have all compressed margins. When a plan becomes unprofitable in a county or state, the carrier either restructures it (often converting PPO to HMO) or exits the market entirely.

What should agents do when a client's MA plan is terminated?

Act fast. Clients whose plans are terminated typically qualify for a Special Enrollment Period, giving them a window to enroll in a new MA plan or switch to Original Medicare with a standalone Part D plan. Contact the client before they get a letter from the carrier. Review their provider relationships, prescription needs, and budget, then present the strongest available options in their area. Proactive outreach here is one of the best retention tools an agent has.

Can clients switch to Medigap after losing an MA plan?

It depends on the state and the circumstances. Some states offer guaranteed issue rights for Medigap when an MA plan is terminated involuntarily. Federal rules provide a guaranteed issue right if the client is within their first year on an MA plan and want to return to Original Medicare. Outside of those windows, medical underwriting applies in most states, which can be a barrier for clients with health conditions. Agents should check their state's specific Medigap protections.

How do MA star ratings affect plan stability?

Star ratings directly impact how much CMS pays a plan. Plans rated 4 stars or higher receive quality bonus payments that can add $1,500 or more per member annually compared to lower-rated plans. That extra funding allows higher-rated plans to maintain broader provider networks and richer benefits. Lower-rated plans receive less, which often leads to network contraction, benefit cuts, and the downward cycle that drives plan terminations.

The Bottom Line

Two million displaced seniors is not a footnote. It is a structural shift that is redefining how Medicare Advantage operates and how agents need to approach plan recommendations.

The carriers are not villains here. They are responding rationally to a payment environment that has compressed margins to the point where broad networks and rich benefits are not sustainable for every market. Agents who understand this dynamic can serve their clients better and build more resilient practices.

The agents who will thrive through this transition are the ones already doing the work: checking star ratings, verifying networks, having honest conversations about the trade-offs that come with Medicare Advantage, and keeping Medigap in their toolkit. The wave is here. The question is whether you are positioned to help your clients ride it out.