Why Medicare Agents Are Split on Healthcare Price Transparency

-

May 18, 2026

We pulled responses from hundreds of licensed Medicare agents across our Q&A community on a straightforward question: How has the push for healthcare price transparency affected your work?

The answers split almost down the middle. Roughly half said it changed absolutely nothing. The other half described a fundamental shift in how clients show up to meetings, what they ask about, and what they expect an agent to know.

Both sides have a point. But the gap between them tells a story about where this industry is headed and which agents are positioned for the clients of the next five years.

- Healthcare price transparency has not changed Medicare pricing mechanics, but it has changed what some clients know before meeting with an agent.

- Agents who treat pricing data as a client education tool can use Medicare.gov's Procedure Price Lookup, EOB reviews, and plan-specific cost comparisons to build trust and explain out-of-pocket exposure more clearly.

- The split among agents isn't about who's right. It's about whether your practice is set up to use transparency data as a tool or absorb it as a disruption.

The "Nothing Changed" Camp: Why Half of Agents Shrugged

A significant chunk of agents gave some version of the same answer: price transparency is irrelevant to Medicare because CMS already sets the rates.

One Colorado-based agent put it plainly:

Honestly, I haven’t seen much impact in the medicare space. CMS has always had an approved pricing list and most (but not all) of the time the price the client pays is determined by the copay defined in their plan. Having said that I am all for transparency and would love to see healthcare at all levels move to a more standard pricing model.

Others echoed the sentiment. A South Carolina agent argued transparency reform belongs in the ACA market, not Medicare. Several more said they hadn't noticed any change at all in client behavior or their own workflow.

The logic holds on the surface. Medicare Part A and Part B have published fee schedules. Medicare Advantage plans define copays, coinsurance, and maximum out-of-pocket limits in their Summary of Benefits. There isn't the same Wild West pricing problem that plagues the commercial insurance market.

So why would transparency rules change anything?

Some agents in this camp took a slightly different angle: they've always been transparent about costs, so the regulatory push didn't create anything new for their practice. For agents who already walk clients through cost-sharing details before anyone asks, the new rules feel redundant. Their argument isn't that transparency doesn't matter. It's that they were already doing it.

I have always discussed prices with the customer in advance so they thoroughly understand the cost and the coverage they will be getting. Because of the way I do business, I rarely have a cancellation of the policy that I'm offering to my customers.

The "Everything Changed" Camp: A Different Client Is Walking Through the Door

The other half of agents told a completely different story. They described clients who arrive to meetings armed with data they didn't have three years ago, cross-referencing hospital pricing with their Explanation of Benefits and challenging discrepancies their agents need to explain.

The push for healthcare price transparency has transformed the way I work as a Medicare agent. Clients are no longer just asking which plan covers their prescriptions—they’re asking how negotiated rates compare across providers and what their true out-of-pocket costs will be. It’s made my role more consultative and educational, which I welcome.

One unexpected outcome? Some clients have become incredibly savvy—almost like amateur billing analysts. They’re cross-referencing hospital pricing data with their Explanation of Benefits and even challenging discrepancies. It’s a shift I didn’t anticipate, but it’s empowering. People are finally feeling like they have a seat at the table when it comes to their healthcare decisions.

Other agents pointed to specific tools driving this shift. The Procedure Price Lookup on Medicare.gov lets clients search by procedure code and see what Medicare pays at different facility types. Agents in Michigan and North Dakota reported that while this data gives clients enough information to feel informed, it often leaves them confused about what they'd actually pay under their specific plan. That confusion, several agents noted, is deepening the agent relationship rather than replacing it. Clients say they looked up the prices online but still need someone to translate what those numbers mean for their doctors, medications, and budget.

A Massachusetts agent noticed a subtler behavioral shift: some clients now feel allegiance to their existing coverage specifically because they've seen transparency data showing how much a procedure was covered, not realizing that another option might work even better.

Why the Split Isn't Random

Look at the two camps closely and a pattern emerges. The agents who reported zero impact tend to frame their role around plan selection: finding the right Medicare Advantage plan or Medigap policy, matching formularies to drug lists, and closing the enrollment. That's a valid and necessary job.

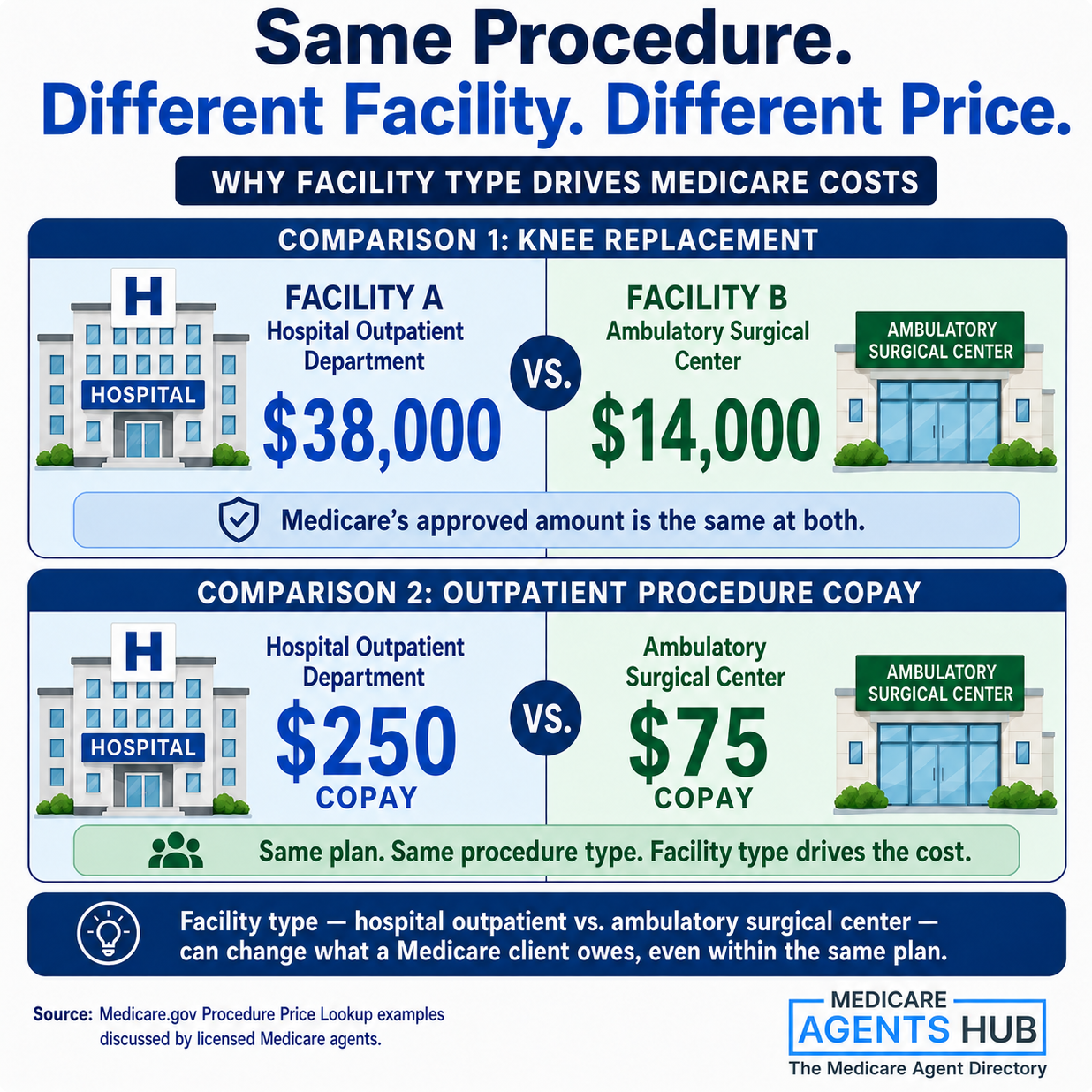

The agents who reported a transformation tend to frame their role around ongoing cost navigation. They're walking clients through EOBs, explaining why the same knee replacement costs $14,000 at one facility and $38,000 at another (even though Medicare's approved amount is the same), and helping seniors understand what their actual share will be under different plan structures.

| "Nothing Changed" Agents | "Everything Changed" Agents | |

|---|---|---|

| Primary role | Plan selection and enrollment | Ongoing cost navigation and education |

| Client prep level | Clients usually come in with fewer pricing questions | Clients arrive with pricing research |

| Transparency data | Not relevant to plan mechanics | Used as a meeting tool and trust builder |

| Conversation length | Unchanged | Longer, more detailed |

| Retention strategy | Annual check-ins at enrollment | Year-round cost guidance |

That second group isn't doing a different job. They're doing a broader version of the same job. And the price transparency rules are handing them new tools to do it with.

Some agents land right in the middle of this divide. They haven't overhauled their practice, but they've noticed that conversations take longer and require more detail than they used to.

I’ve always been transparent with my clients so it really hasn’t affected me just makes me go into a lot more detail details. This sometimes can be more confusing to clients, but I usually try to simplify it at a basic level.

The CMS Procedure Price Lookup: An Underused Client Meeting Tool

Several agents in the pro-transparency camp referenced the Procedure Price Lookup tool on Medicare.gov as something they now pull up during client meetings. The tool lets you search by procedure code and see what Medicare pays at different facility types, what the patient owes under Original Medicare, and how that compares across ambulatory surgical centers vs. hospital outpatient departments.

For agents who work the Medigap side, this is a trust-building move. You can show a client exactly what Part B covers for a given procedure, then walk through how Plan G or Plan N fills the gap. The math becomes concrete instead of abstract.

This has required providers and hospitals to be more transparent about disclosing their prices so beneficiaries can make informed decisions with informed consent.

When you go the medicare.gov site and lookup the Procedure Price Lookup you can find out with the procedure code, exactly what medicare will pay for both ambulatory and outpatients centers. you will see how much the patient pays with Original Medicare without any supplement (medigap) policy.

For agents working Medicare Advantage, it's equally useful. When a client asks why their copay at Hospital A was $250 but a similar procedure at an outpatient center would have been $75, you can point to the pricing data and explain how facility type drives cost, even within the same plan. That kind of explanation builds the trust that converts prospects into long-term clients.

One important note for Medicare Advantage clients: agents should still verify plan-specific copays, network rules, and prior authorization requirements directly with the plan. The Procedure Price Lookup is most useful as a Medicare payment reference point, not a final estimate of what an MA member will actually owe.

The CMS tools aren't limited to procedure lookups. The Medicare Plan Finder on Medicare.gov lets clients (and agents) compare total annual costs across plans based on specific prescriptions, providers, and usage patterns. Agents who already use this during enrollment can extend the same approach to facility pricing conversations. One Minnesota-based agent recommended connecting clients with the official Plan Finder and a local independent agent together, combining the data with personalized guidance.

The New Client Profile: The EOB Cross-Referencer

Multiple agents described a client type that barely existed five years ago: the senior who shows up with printouts. They've pulled hospital pricing files. They've compared their EOB line items against what the hospital publicly listed. They have questions about discrepancies, and they want their agent to explain them.

This can feel like an interrogation if you aren't ready for it. But agents who lean into it describe these clients as their most loyal. Several described the shift as empowering for clients. The data gives seniors a sense of agency in their healthcare decisions, even when they still need help interpreting what the numbers actually mean for their plan.

The risk, as a few agents pointed out, is when this data creates false confidence. A client who sees that Hospital A's list price is lower than Hospital B's might assume Hospital A is the better deal, not understanding that their MA plan's negotiated rate at Hospital B could result in a lower copay. The agents who specialize in chronic conditions see this most often: diabetic clients comparing insulin costs across pharmacies using pricing data that doesn't reflect their plan's formulary tier.

This is where the agent relationship becomes irreplaceable. Raw pricing data without plan-specific context is noise. An agent who can translate that noise into a clear cost picture is doing something a website can't.

Part of that translation is teaching clients when and how to verify costs before a procedure, not after the surprise bill shows up.

What's the best way to avoid surprise bills for lab tests under Medicare Advantage?

Always check before you have anything done, This way there will not be surprises. You always have a right to get a price quote.The same principle applies to understanding what Original Medicare actually covers vs. what feels like it should be covered. When a client is frustrated that specialist visits still carry significant out-of-pocket costs, the transparency-minded agent can walk through the math in real time.

I've been paying into Medicare for years, and I'm not sure why my specialist visits still cost me so much. What am I missing here?

What usually surprises people is that Original Medicare isn’t designed to cover everything—it’s more of a cost-sharing setup.Under Part B, you generally pay:

• The annual deductible

• Then 20% coinsurance for specialist visits, tests, and procedures

• And there’s no cap on what you could spend out of pocket

So if your specialist bills $300, you’re on the hook for about $60 every visit—and that adds up quickly.

What most people are “missing” is that Medicare was built to be paired with either:

• A Medigap (supplement) to cover that 20%, or

• A Medicare Advantage plan that replaces the 20% with set copays and includes a max out-of-pocket

If you only have Original Medicare by itself, what you’re experiencing is exactly how it’s structured to work.

What the "No Impact" Agents Might Be Missing

The agents who reported zero impact aren't wrong about the mechanics. CMS does set approved amounts. Plan cost-sharing is defined in the Summary of Benefits. Price transparency rules didn't change how Medicare pays for things.

But they may be underestimating how these rules changed what clients know before they sit down with you. A Tennessee agent who fell somewhere in the middle captured this well: "I really have not found this has affected my work as a Medicare Agent. I do believe the Medicare Advantage plans have adjusted and set copays for procedures and tests based on hospitals charging more than standalone facilities."

That last sentence is the tell. The cost variation between facility types is exactly the kind of thing transparency rules made visible. Even agents who say it hasn't affected their practice are acknowledging that it's affecting the plans themselves.

Clients are reading about facility pricing differences in news articles, seeing them on hospital websites, and asking about them during enrollment meetings. The question isn't whether price transparency affects Medicare. It's whether your practice is set up to use it as a tool or whether it hits you as a surprise during AEP.

One place this blind spot shows up: the client who picked the lowest-premium plan and is now confused by the out-of-pocket costs. Transparency data gives these clients enough information to feel savvy, but not enough to understand the premium-vs-copay tradeoff without an agent walking them through it. Several agents noted that low-premium plans often carry higher copays, coinsurance, and deductibles, and that clients who see doctors regularly or take prescriptions may save more with a higher-premium plan that has lower cost-sharing. The agents who maintain relationships year-round catch these mismatches before they become billing surprises.

A Practical Playbook for Agents Who Want to Lean In

If you're in the "hasn't affected me" camp and want to explore what the other side is doing, here's what the pro-transparency agents described as their workflow:

Before the Meeting

- Pull up the client's local hospitals on the CMS Procedure Price Lookup and note the price differences for common procedures (joint replacements, cardiac stents, colonoscopies)

- Check whether the client's current plan treats hospital outpatient and ambulatory surgical center copays differently

- Review the client's recent EOBs if they'll share them, specifically looking for facility charges vs. professional charges

During the Meeting

- Use the pricing data to explain why a plan might be better, not just that it's better. "Your copay is lower at outpatient centers because Medicare pays less there" is more persuasive than "this plan has a $75 copay."

- When a client brings their own pricing research, validate it first, then add context. Don't dismiss what they found.

- For Medigap clients, walk through a real procedure's Medicare-approved amount and show how their supplement covers the gap. Concrete math beats abstract promises.

The agents who do this well can break down total annual costs in a way that makes the plan decision feel obvious. For a client with a chronic condition like diabetes, that means mapping out Part B premiums, plan premiums, prescription copays, and the catastrophic coverage threshold so the client sees the full annual picture rather than reacting to individual bills.

After the Meeting

- If a client is choosing between plans and cost is the deciding factor, build a simple comparison using 2-3 procedures they're likely to need. Use actual CMS pricing data, not plan marketing materials.

- Send a follow-up that references the specific numbers you discussed. This is the kind of detail-oriented follow-up that separates agents who close from agents who lose track.

- For clients who want to keep digging, point them to resources on uncovering coverage gaps they may not have considered.

Our Q&A community has dozens of agents sharing their real-world approaches to price transparency, client objections, and cost breakdowns. Browse their answers, add your own perspective, or connect with agents in your state through Medicare Agents Hub.

Where This Is Headed

CMS continues to expand transparency requirements. CMS has continued to expand and enforce hospital price transparency requirements, including publishing enforcement updates, civil monetary penalty information, and hospital compliance resources. As more facilities publish machine-readable pricing files, the data gets better and more clients will encounter it.

The agents who are already comfortable with this data have a head start. The ones who aren't don't need to overhaul their practice overnight. But the client who walks in with an EOB in one hand and a hospital pricing printout in the other is becoming more common, not less.

For agents thinking longer-term, the cost conversation doesn't end at enrollment. Clients whose health is expected to change over the next decade need a plan structure that accounts for that, and the agents who can walk through those projections using real numbers are the ones clients stick with.

How do I budget for Medicare costs if I expect my health to decline in the next decade?

Wow, good question. If you are expecting to have health problems, I would suggest going with a Medicare Supplement plan. It will give you a structured payment every month that you can budget. However, the downfall is that as health coverage gets more expensive, your monthly payment to a Medicare supplement will also increase. On average it will increase about 10-15% a year. So, budget an increase in your healthcare costs by about 15% a year and you should be fairly close.The broader transparency conversation in this industry extends well beyond hospital pricing. Commissions, plan incentives, and carrier relationships are all getting more scrutiny from clients who expect openness. The agents thriving in that environment are the ones who decided transparency wasn't a threat to their value. It was proof of it.

If you're an agent who's found a way to turn pricing data into a competitive advantage, or if you think the transparency push is all noise, we want to hear from you. Claim your profile on Medicare Agents Hub and join the agents shaping how this industry talks about transparency.

Frequently Asked Questions

How does healthcare price transparency affect Medicare specifically?

Price transparency rules require hospitals to publish their pricing data, but they don't change how Medicare sets payment rates. CMS still determines approved amounts for Part A and Part B services. The impact on Medicare agents is indirect: clients now arrive to meetings with more pricing awareness, asking sharper questions about out-of-pocket costs, facility price differences, and how their specific plan handles cost-sharing.

What is the CMS Procedure Price Lookup tool?

The Procedure Price Lookup on Medicare.gov lets you search by procedure code and compare what Medicare pays at different facility types, including ambulatory surgical centers and hospital outpatient departments. It also shows what the patient owes under Original Medicare. Agents use it during client meetings to make cost conversations concrete rather than abstract.

Should Medicare agents change their practice because of price transparency?

Not necessarily. Agents whose clients don't ask about pricing data may not need to change anything immediately. But agents who want to uncover hidden client needs are finding that transparency tools give them new ways to demonstrate value, especially during plan comparisons and EOB reviews. The shift is gradual, but the trend is toward more informed clients who expect more detailed cost conversations.

Why do some agents say price transparency hasn't affected Medicare?

These agents are technically correct that CMS-set rates and plan-defined cost-sharing haven't changed because of transparency rules. Their perspective tends to focus on plan selection and enrollment, where the mechanics are the same as before. The agents who report a bigger impact tend to work more on ongoing cost navigation, EOB interpretation, and facility-level price comparisons.

How can agents use pricing data to build client trust?

Pull up the Procedure Price Lookup during meetings to show clients exactly what Medicare covers for a given procedure and how their supplement or Advantage plan fills the gap. When clients bring their own research, validate what they found before adding context. Follow up after meetings with specific numbers you discussed. Agents who make the math visible and verifiable build the kind of trust that leads to long-term retention.