Agent Appeals War Stories: Five Cases Where Brokers Reversed Denials Their Clients Were Told Were Final

-

June 8, 2026

The first denial is almost never the last word. Most clients don't know that. Most new agents don't either.

Health-plan denials, billing disputes, and Medicare coverage problems are rarely as final as they sound. The agents who learn to push back become irreplaceable to their clients. What follows are five real cases from licensed agents on Medicare Agents Hub, each involving a denial that looked final until someone decided to fight it. Agent names are included as published on Medicare Agents Hub; client details are summarized to focus on the appeal lessons.

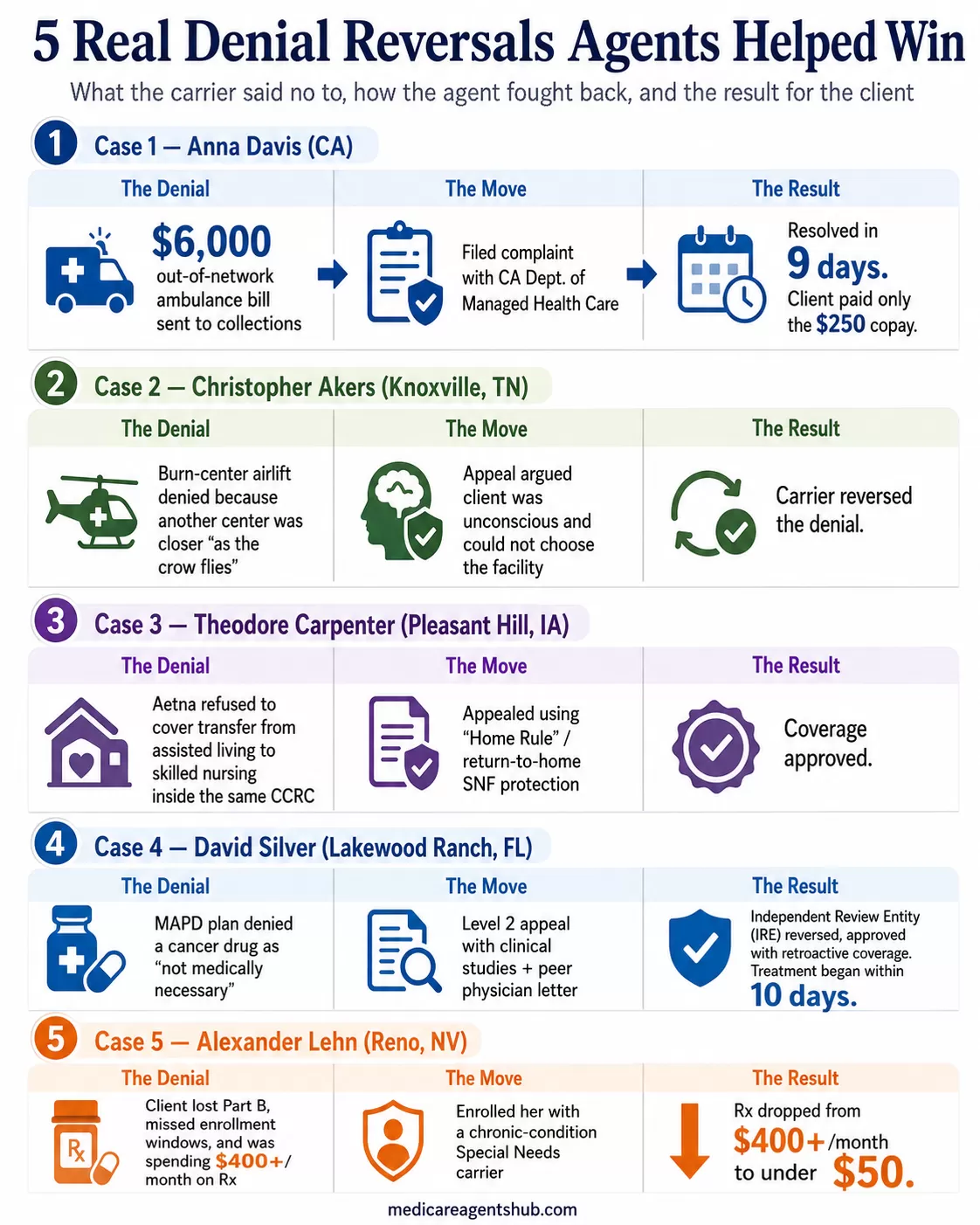

Case 1: The $6,000 Ambulance Bill That Went to Zero

Anna Davis, a CIC-RSSA licensed agent in California, had a former client come to her with a problem that had nothing to do with Medicare. The client had been on a Covered California plan when he needed emergency ambulance transport. The carrier denied the claim, saying the ambulance provider was out of network. Under his policy, the client owed a $250 copay. The ambulance company wanted the full amount: more than $6,000.

By the time the client reached Anna, the bill had gone to collections. He was getting threatening calls. He was also Portuguese-speaking with a speech impediment, which meant every phone call to the carrier required him to come into Anna's office so she could handle the communication.

Anna and her client spent hours on the phone being transferred from department to department trying to file a grievance. The carrier stalled. So Anna went looking for another path. She found California's Department of Managed Health Care (DMHC), filed a formal complaint, attached the bilingual intake notes, and the bill was resolved in nine days. The client never heard from the collection agency again.

I had a client who was on a Covered California plan with a certain carrier. When he aged into Medicare, I helped him enroll in a Medicare plan. Two years after being on Medicare, he received a $6,000+ ambulance bill from the time he was still on the Covered California plan. The carrier had denied the claim, stating that the ambulance provider was out of network—even though it was an emergency situation.

In reality, he was only responsible for a $250 copayment per his Covered California policy. But the ambulance company was demanding he pay the full amount—over $6,000—and had turned the bill over to collections.

By the time he contacted me, he was being harassed by a collection agency. He was facing additional charges, late fees, interest, and constant threatening phone calls. We called the carrier and were transferred from one department to another for hours, just trying to file a grievance and get them to pay what they were supposed to cover.

The man was Portuguese and had a speech impediment, so he had to come to my office every time we needed to call or fill out forms. He didn’t speak much English, so we handled the communication and paperwork for him.

After doing some digging online, I found the Department of Managed Health Care Services—and they were lifesavers. We filed a complaint with them, and magically, within a few days, the bill was paid. The client never heard from the collection agency again.

The takeaway for newer agents: when you hit a wall with the carrier, find the regulator and understand the complaint pathway. In many cases, a documented complaint to the right oversight body can create movement that repeated carrier phone calls do not. Every state has a department that oversees managed care, and knowing where to file is half the battle. Anna's case also highlights a reality that many producers overlook: working effectively with clients who face language barriers often means being physically present, not just available by phone.

Case 2: The Burn Center Denial Overturned on "As the Crow Flies"

Christopher Akers, a licensed agent in Knoxville, Tennessee, had a client who was burned in a farm accident and airlifted to a burn center. The carrier denied the claim because another burn center was closer "as the crow flies."

That phrase became the appeal's centerpiece. Akers filed an appeal arguing that the client was unconscious at the time of transport, that neither the client nor any family member signed off on the facility choice, and that straight-line distance is not a meaningful standard for emergency air transport.

Had a client get burned on their farm and was flew out to a burn center. The carrier did not want to pay because another burn center was closer 'as the crow flies'. We filed an appeal with the carrier, stating that they were unable to make the decision as to where to be flown to because they were unconscious, and they nor any family member had signed off on it.

The carrier reversed the denial. The argument that won wasn't medical. It was procedural: the client had no ability to choose a facility, and the carrier's distance metric didn't account for actual travel conditions or the emergency protocols that governed the flight crew's decision.

For agents working in rural areas, this case is worth remembering. Network adequacy challenges are more common when clients live far from major medical centers, and carriers sometimes lean on geographic shortcuts that don't reflect reality on the ground.

Case 3: The CCRC "Home Rule" That Nobody Knew Applied

Theodore Carpenter, a licensed agent in Pleasant Hill, Iowa, fought this battle for his own parents. They had moved into a Continuing Care Retirement Community (CCRC), and when his father broke his hip and needed to transfer from the assisted living division to the skilled nursing division within the same facility, the carrier (Aetna) claimed he was out of network and refused to cover it.

Carpenter appealed using a concept called "Home Rule," arguing that his father had established residency in the CCRC's assisted living unit and had no choice but to move to the skilled nursing wing within the same community. The transfer wasn't voluntary. It was medically necessary and happened within the same facility where the patient already lived. In Medicare Advantage rules, this concept is closely related to the "return to home skilled nursing facility" protection, which can apply when the enrollee resides in a CCRC and needs posthospital skilled nursing care within that community.

My parents moved into a CCRC (Continuing Care Retirement Community), and Aetna claimed they were out of network, so they were not going to cover it. I appealed it, stating that there's a term called "Home Rule," which means they had begun living in the assisted living division, and my dad had no choice but to move to the skilled nursing division when he broke his hip. They finally agreed, and we got it paid for.

This case matters for any agent with clients in CCRCs. The continuity-of-care argument is powerful when a patient transitions between levels of care within the same community, but many agents (and many carrier reps) have never encountered the Home Rule concept. Knowing it exists is the difference between accepting the denial and winning the appeal.

Case 4: The Cancer Drug Reversal at the Independent Review Entity

David Silver, a licensed agent in Lakewood Ranch, Florida, had a client on a Medicare Advantage Prescription Drug (MAPD) plan whose oncologist prescribed a critical cancer drug. The carrier denied coverage, calling it "not medically necessary."

Silver filed a Level 1 appeal with the client's medical records. Denied again. He escalated to a Level 2 appeal, this time building a stronger package: clinical studies supporting the drug's use for the client's specific condition, a peer physician letter, and a personal statement from the client describing the impact of going without treatment.

The case went to the Independent Review Entity (IRE), the external body that reviews Medicare Advantage appeals after the plan's internal process is exhausted. The IRE reversed the denial and approved the drug with retroactive coverage. The client began treatment within 10 days and saw improvement.

A client on a MAPD plan was denied coverage for a critical cancer drug her oncologist prescribed, labeled “not medically necessary.” We filed a Level 1 appeal with medical records—it was denied. We escalated to a Level 2 appeal, adding clinical studies, a peer physician letter, and a personal statement from the client. The Independent Review Entity reversed the denial, approving the drug with retroactive coverage. She began treatment within 10 days and saw improvement. This case underscored the power of persistence and strong documentation in the appeals process.

Silver's case is a textbook example of why agents should never stop at Level 1. Many appeals become stronger at Level 2, especially when the file includes physician support, clinical evidence, and a clear written record. Outside reviewers examine the evidence without the plan's financial interest in the outcome, and in Silver's case the clinical studies and peer physician letter were what made the difference. When a Medicare plan fails a client, the documentation you bring to the appeal table matters more than the argument you make on the phone.

Case 5: The Part B Reinstatement Nobody at SSA Flagged

Alexander Lehn, a licensed agent in Reno, Nevada, had a client whose situation had compounded over years of bad luck and worse guidance. She had lost her Part B coverage because she was out of work and hospitalized. Nobody helped her set up Social Security payments to maintain her premiums, so coverage lapsed. She moved states, got healthy enough to restart the process, and by the time she had her new Medicare card with an updated Part B effective date, she had missed her enrollment windows.

Medicare told her she would have to wait until the following year. Meanwhile, she was spending over $400 a month on prescription drugs with no coverage and had been in and out of the hospital, racking up bills she couldn't pay.

Lehn found a path that nobody at the Social Security Administration office had flagged. Using a loophole tied to the client's chronic health conditions, he got her enrolled with a carrier that specializes in managing care for those conditions. Her prescription costs dropped from over $400 a month to under $50.

I had a client who lost her part B because she was out of work and in the hospital. No one tried to help her get her social security set up to maintain the premiums so she lost all coverage. She ended up moving states to where I live and got healthy enough to fight through the process of getting her social security set up and reinstating her part B. The process took so long but that by the time she got her new Medicare card with an updated Part B affective date, she missed her new enrollment windows and Medicare denied her enrollment. At this point she was spending over $400 per month on prescription drugs with no coverage and had been in and out of the Hospital, incurring significant financial burdens. I found a loophole due to her chronic health conditions and got her coverage with a carrier that specializes in managing care for her conditions. Medicare told us that she would have to wait until next year, but they were wrong and she now has the coverage and care she needs along with her prescription cost being lowered to less than $50/mo. That was a win.

This case is different from the others because the "appeal" wasn't against a carrier denial. It was against the system itself. The client was told by Medicare that she had to wait, and a less persistent agent would have accepted that answer. Lehn didn't. He looked for an alternative path, found one, and his client went from financial crisis to stable coverage.

The Shared Playbook: What All Five Cases Had in Common

These five cases span different states, different carriers, and different types of denials. But every one of them shares three things.

Documentation Before Emotion

Every successful appeal started with paperwork, not phone calls. Medical records, billing statements, policy language, clinical studies, regulatory filings. The agents who win appeals are the ones who build a paper trail before they pick up the phone. Anna Davis attached bilingual intake notes. David Silver included peer physician letters and clinical research. Christopher Akers challenged the carrier's distance methodology with actual data. None of these appeals were won by being louder. They were won by being more prepared.

Regulator Escalation When the Carrier Stalls

Anna Davis went to California's DMHC. David Silver went to the IRE. The pattern is the same: when the carrier's internal process produces the wrong answer, you take the case to someone the carrier actually has to listen to. Every state has a Department of Insurance or managed care oversight body. Medicare has the IRE for Advantage plan appeals. These aren't last resorts. They're tools, and the agents in these stories treated them that way.

Persistence Past the First No

Not one of these cases was resolved on the first attempt. Anna Davis spent hours on hold before finding the DMHC. Silver's Level 1 appeal was denied before Level 2 succeeded. Lehn's client had been told by Medicare itself to wait a year. The agents who do this work well have internalized something that newer producers need to hear: the first "no" is the beginning of the process, not the end of it.

Why This Work Matters (Even When It's Unpaid)

Some agents argue that appeals work isn't broker work. The member should handle it, or a patient advocate should step in. That's a defensible position right up until you look at the business case for doing it anyway.

Anna Davis's client will never leave her. David Silver's client will refer every friend with a cancer diagnosis. Alexander Lehn's client went from spending $400 a month to $50 and has a story she tells everyone who will listen. Appeals work is unpaid in the short term and one of the strongest differentiators a broker can build over a career.

The agents who fight denials don't do it because it's in the job description. They do it because it's the reason they got into the business. And the clients on the other end of those fights remember.