Concierge Medicine on Medicare: What the Membership Fee Actually Buys You and the Three Setups That Backfire

-

April 20, 2026

Concierge medicine is growing fastest among retirees, and for good reason. Longer appointments, same-day access, your doctor's direct phone number. For seniors tired of the 12-minute office visit, the appeal is obvious. But pair a concierge practice with the wrong Medicare setup and that $2,000-to-$5,000 annual membership fee can quietly become a second insurance premium that buys you almost nothing you didn't already have.

We asked licensed Medicare agents across the country how concierge medicine interacts with Medicare. Their answers were sharp, specific, and occasionally contradictory, which is the point. The right concierge arrangement depends on which of three practice models your doctor runs, whether you carry Original Medicare or Medicare Advantage, and whether you've read the fine print on what that membership fee actually covers.

Does Medicare Cover Concierge Medicine?

Medicare does not cover the concierge membership fee. However, Medicare may still cover Medicare-approved medical services if the concierge doctor accepts Medicare and bills Medicare for those services. The membership fee pays for enhanced access (longer visits, same-day scheduling, direct phone line), not for clinical care. Whether you actually benefit from combining the two depends on the type of concierge practice, your Medicare coverage setup, and how often you use primary care.

How Concierge Medicine and Medicare Occupy Separate Lanes

The most common misconception agents encounter is the belief that a concierge membership replaces or modifies your Medicare coverage. It doesn't. Your Medicare coverage still handles hospitalizations, specialist visits, lab work, imaging, and every other Part A and Part B covered service, but how those claims are processed depends on whether you have Original Medicare or Medicare Advantage. The concierge membership fee is a completely separate, out-of-pocket arrangement between you and your primary care physician.

That membership fee pays for things Medicare was never designed to cover: unhurried appointments, same-day or next-day scheduling, 24/7 direct communication with your doctor, and a smaller patient panel so your physician isn't juggling 2,500 patients at once. Medicare doesn't reimburse any portion of the fee, and no Medigap plan or Medicare Advantage plan covers it either.

The critical question isn't whether you can have both. You can. The question is whether your concierge doctor still participates in Medicare, because that single detail changes everything about your out-of-pocket exposure.

I'm considering concierge medicine but already have Medicare. How would these work together?

Great question! Concierge medicine and Medicare can actually work together quite well, and you're not alone in wondering how they complement each other.Here's the basic idea: Medicare remains your primary insurance and continues to cover hospitalizations, specialist visits, lab work, and other medical services just as it always has. Concierge medicine — sometimes called a direct primary care (DPC) practice — is a separate membership arrangement you have directly with your primary care physician. You typically pay a monthly or annual fee in exchange for enhanced access and services, such as same-day appointments, longer office visits, 24/7 direct access to your doctor, and more personalized, unhurried care.

The key thing to understand is that concierge doctors generally do not bill Medicare for the primary care services covered under your membership fee. However, if your concierge doctor refers you to a specialist, orders labs, or arranges a hospital stay, Medicare can still be billed for those services as usual.

So in practice, you'd be paying the concierge membership fee out of pocket (typically $100–$300/month depending on the practice), while Medicare continues to handle the bigger-picture coverage.

If you already have a Medicare Supplement (Medigap) or Medicare Advantage plan, it's worth reviewing how those interact as well — some plans may have network restrictions that are worth considering.

Three Types of Concierge Practices and What Each Means for Your Coverage

Agents consistently describe three distinct models, and each interacts with Medicare differently. Knowing which model your doctor runs is the first step before writing any check.

The Doctor Still Accepts Medicare Assignment

This is the setup that works cleanest. The physician charges a membership fee for enhanced access (the longer visits, the direct phone line, the same-day scheduling) but continues to bill Medicare for covered medical services. When you see the doctor for a problem, Medicare pays its share. If you have a Medigap supplement, it picks up the remaining cost-sharing. The membership fee covers the access, not the medicine.

Agents who work with affluent retirees report this as the most common model. The doctor limits their patient panel to 200 or 300 people, charges an annual fee in the $1,500-to-$3,000 range, and still files claims with Medicare for every covered office visit, lab order, and referral. The senior pays the membership fee out of pocket and uses Medicare for the clinical care exactly as before.

The Doctor Has Opted Out of Medicare Entirely

This is where the math changes dramatically. A physician who has formally opted out of Medicare has filed paperwork with CMS agreeing not to bill Medicare for any services for at least two years. Under Medicare rules, when you see an opted-out provider, you sign a private contract acknowledging that Medicare will not pay for any services that doctor provides, and neither will your Medigap plan or Medicare Advantage plan.

This is not agent opinion. It is federal Medicare policy. A private contract with an opted-out provider means every dollar of care from that doctor comes out of your pocket, on top of the membership fee. Several agents report seeing seniors surprised by this after the fact, having assumed their supplement would at least cover part of the bill.

Direct Primary Care (the Hybrid Model)

Direct primary care (DPC) practices charge a flat monthly or annual fee that covers most or all primary care services directly. Unlike traditional concierge practices, DPC doctors typically do not bill any insurance at all, including Medicare. The monthly fee (often $75 to $200) covers office visits, basic labs, sometimes minor procedures, and communication access.

The distinction matters because some seniors confuse concierge medicine and DPC. One agent pointed out that when people say "concierge medicine," they sometimes actually mean direct primary care, and the billing relationship is fundamentally different. In a DPC arrangement, Medicare isn't being billed because the services are bundled into the flat fee. You still need Medicare for everything outside that practice: hospital stays, specialist care, imaging, prescriptions, and emergency services.

I'm considering concierge medicine but already have Medicare. How would these work together?

Concierge medicine is separate from Medicare. You pay a membership fee for better access—longer visits, same-day appointments, direct communication—and Medicare does not cover that fee.Here’s how concierge works with Medicare:

Original Medicare (especially with a supplement):

This is where concierge usually works best. If the doctor accepts Medicare, they bill Medicare for covered services, and your supplement applies as normal.

Most of my clients who use concierge care are on Original Medicare with a High Deductible Plan G—it keeps premiums lower while still giving strong protection for bigger expenses.

Medicare Advantage plans:

This can be more difficult. These plans use networks, and many concierge doctors are out-of-network or don’t participate. That means you could be paying the membership fee and out-of-pocket for care.

If the doctor opts out of Medicare:

Medicare won’t pay at all—you’re fully private pay.

Bottom line:

Concierge care can complement Medicare, but it usually works much better with Original Medicare (often paired with a High Deductible Plan G) than with Medicare Advantage.

Call our office if you still have questions or concerns about Medicare.

Why Medigap Almost Always Pairs Better Than Medicare Advantage

This is where agents split most visibly along the lines of what they primarily sell, but the consensus tilts heavily in one direction. Agents who work with concierge-using clients overwhelmingly recommend Original Medicare paired with a Medigap supplement over Medicare Advantage.

The reasoning is structural, not ideological. Medigap has no provider network. If the concierge doctor accepts Medicare assignment, they can bill Medicare directly regardless of which Medigap plan you carry. There's no referral requirement, no prior authorization for specialist visits your concierge doctor orders, and no question about whether the doctor is "in network."

Medicare Advantage plans, by contrast, use provider networks. An HMO-style plan typically requires all care to go through in-network providers. If your concierge doctor isn't in the plan's network, you face two problems: the plan won't cover services from that doctor, and you're paying a membership fee on top of getting no plan-level coverage for those visits. One agent noted that some concierge doctors have started working with PPO-style Medicare Advantage plans, which offer out-of-network coverage at higher cost-sharing. But agents broadly describe this as the exception, not the rule.

Several agents specifically recommend High Deductible Plan G as the pairing that keeps premiums lower while still providing strong protection for bigger expenses outside the concierge practice. The logic: you're already paying the concierge fee for primary care access, so choosing a higher-deductible supplement reduces your total monthly outlay without sacrificing coverage for the hospital stays, surgeries, and specialist care that Medicare and your supplement handle.

I'm considering concierge medicine but already have Medicare. How would these work together?

Here’s the clearest way to think about it: concierge medicine and Medicare can work together, but they operate in completely separate lanes. Medicare continues to cover Medicare‑approved services, while the concierge membership fee is always 100% out‑of‑pocket. The key is understanding what your concierge doctor bills to Medicare versus what your membership fee actually buys you.The Three Setups That Quietly Backfire

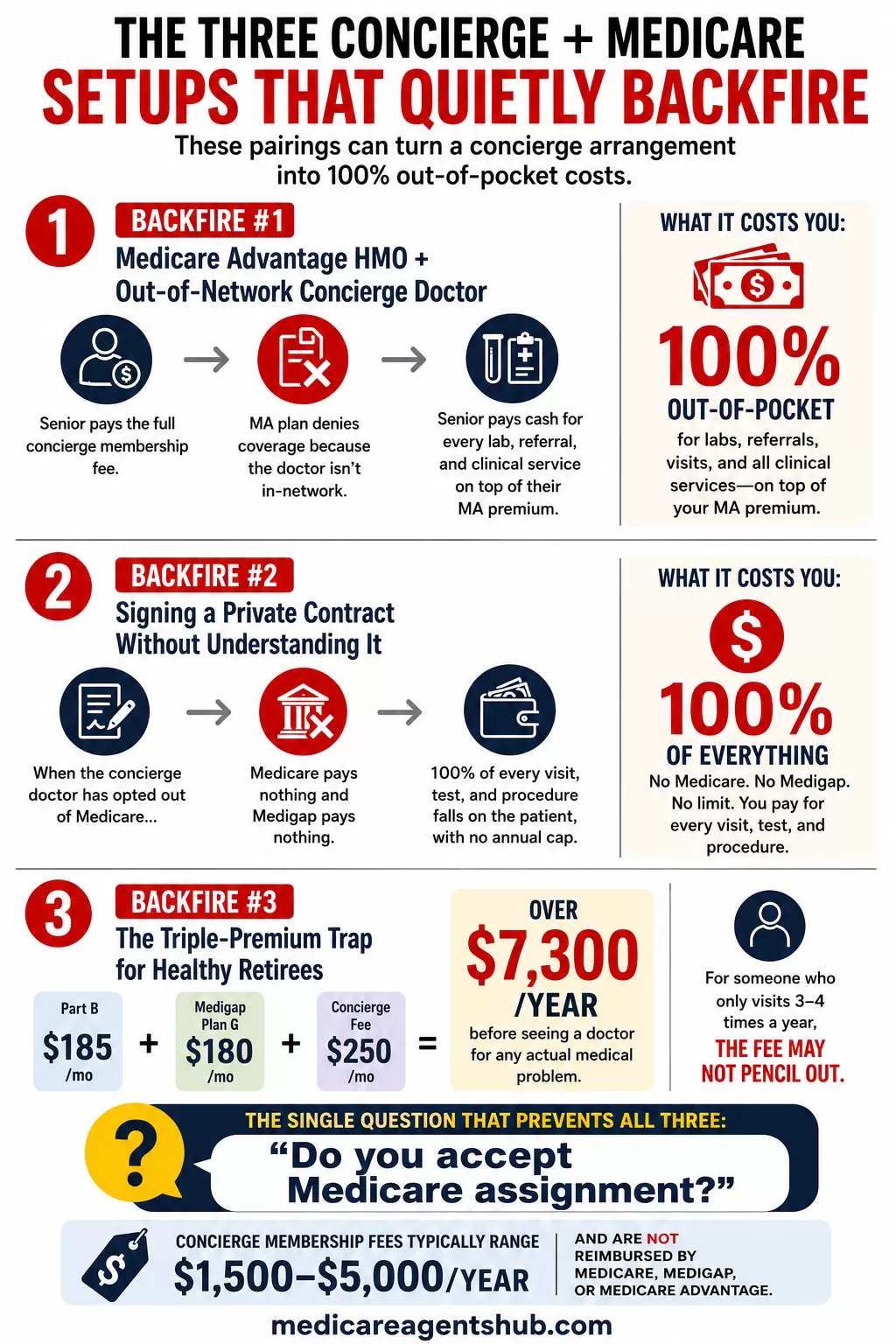

Not every concierge-plus-Medicare combination makes financial sense. Agents describe three specific pairings that sound reasonable on paper but routinely cost seniors more than they expected.

Backfire 1: Medicare Advantage HMO Plus an Out-of-Network Concierge Doctor

This is the most common mistake agents flag. A senior on an MA HMO joins a concierge practice without confirming the doctor participates in their plan's network. The result: they pay the full membership fee for enhanced access, but when the doctor orders labs, writes referrals, or provides clinical care, the MA plan denies coverage because the provider is out of network. The senior ends up paying the membership fee and paying cash for every clinical service, while also paying their MA plan premium for coverage they can't use at that practice.

The fix, according to agents, is either switching to Original Medicare with a supplement before joining a concierge practice, or confirming in writing that the concierge doctor is in-network for your specific MA plan. PPO-style Medicare Advantage plans offer more flexibility here, but the out-of-network cost-sharing can still be steep.

Backfire 2: Signing a Private Contract Without Understanding It

When a concierge doctor has opted out of Medicare, federal rules require the patient to sign a private contract before receiving care. That contract states, in plain language, that Medicare will not pay for services from this provider and that the patient waives the right to have Medicare billed. Some seniors sign this during intake paperwork without fully understanding what they've agreed to.

The backfire isn't the concierge fee itself. It's everything else. A senior who assumed their Medigap supplement would cover the 20% coinsurance on services from this doctor discovers that Medigap only pays after Medicare pays first. If Medicare isn't paying (because of the private contract), Medigap pays nothing. The entire cost of every visit, test, and procedure from that doctor falls on the patient, with no annual cap.

Agents consistently recommend asking one direct question before joining any concierge practice: "Do you accept Medicare assignment?" If the answer is no, understand that you're entering a fully private-pay relationship for that doctor's care. You still keep Medicare for every other provider, but nothing from that practice flows through your coverage.

Backfire 3: The Triple-Premium Trap for Healthy Retirees

A healthy 67-year-old paying $202.90/month for Part B, $180/month for a Medigap Plan G, and $250/month for a concierge membership is spending nearly $7,600 per year before seeing any doctor for an actual medical problem. If that retiree only visits the doctor three or four times a year for routine checkups and minor issues, agents question whether the concierge fee is delivering enough value to justify the total spend.

This isn't an argument against concierge medicine. It's an argument for running the numbers honestly. Agents who work with high-income retirees note that the concierge model tends to pencil out for seniors who see their primary care doctor frequently, manage multiple chronic conditions, or place a high value on access and convenience. For the retiree who sees a doctor twice a year for a physical and a flu shot, the membership fee may be buying a premium experience that goes largely unused.

Retirees in higher IRMAA brackets are already paying elevated Part B and Part D premiums based on income. Adding a concierge fee on top of that makes the total healthcare spend significant, and agents suggest that a thorough review of what Original Medicare and a good supplement already cover might reveal fewer gaps than expected.

What the Membership Fee Covers (and Where Medicare Takes Over)

To avoid the "double payment" trap, it helps to draw a clean line between what you're buying with the concierge fee and what Medicare already handles.

The membership fee typically covers:

- Same-day or next-day appointments

- Longer office visits (30 to 60 minutes instead of the standard 12 to 15)

- 24/7 direct access to your doctor via phone, text, or email

- A smaller patient panel (200 to 600 patients instead of 2,000+)

- Annual executive-style physicals or wellness assessments

- Coordination of care across specialists

Medicare continues to cover:

- Part A hospital stays, skilled nursing, hospice

- Part B doctor visits, outpatient care, labs, imaging, preventive screenings

- Specialist referrals and associated testing

- Durable medical equipment

- Part D prescription drug coverage

The membership fee does not cover hospital stays, surgeries, specialist visits, emergency room care, or prescriptions. Those remain squarely in Medicare's lane, which is why every agent emphasizes that concierge medicine does not replace Medicare. You need both. The question is only whether the enhanced primary care access is worth the annual fee given your health needs, visit frequency, and financial situation.

Five Questions to Ask Before Joining a Concierge Practice

Agents who've guided clients through this decision recommend asking these questions before signing anything:

- Do you accept Medicare assignment? This is the single most important question. A "yes" means Medicare still pays for covered services. A "no" means you've entered private-pay territory.

- What exactly does the membership fee include? Get a written list. Some practices bundle basic labs and minor procedures into the fee; others charge separately for everything clinical.

- If I have Medicare Advantage, are you in my plan's network? If not, confirm whether your plan offers out-of-network coverage and at what cost-sharing level.

- Will you still file claims with Medicare for covered services? Some practices that accept Medicare still expect the patient to file their own claims, which adds administrative burden.

- What happens if I need care you can't provide? Understand the referral process. Your concierge doctor should be able to refer you to specialists who accept Medicare, keeping the rest of your care within your coverage.

The Bottom Line for Families Weighing This Decision

Concierge medicine on Medicare is not inherently a good deal or a bad one. It depends almost entirely on which of the three practice models your doctor runs, whether you carry Original Medicare with a supplement or a Medicare Advantage plan, and how often you actually use primary care services.

The seniors who get the most value from concierge care tend to be on Original Medicare with a Medigap supplement, see a doctor who still accepts Medicare assignment, and visit frequently enough to justify the annual fee. The seniors who get burned are typically on Medicare Advantage HMOs with out-of-network concierge doctors, or signed private contracts without understanding that Medicare and Medigap both stop paying when the doctor has opted out.

A licensed Medicare agent can help you evaluate how a concierge arrangement fits with your current coverage, run the actual cost comparison, and flag potential conflicts before you commit to a membership. The math is different for everyone, and the right answer depends on details that only surface when you look at your specific plan, your specific doctor, and your specific health needs.

Based on 54 answers from licensed Medicare agents across 17 related questions on Medicare Agents Hub.