How to Coach Clients Through the 'Will Medicare Cover My Acupuncture / Chiropractor / Marijuana / Concierge Doctor?' Question

-

June 21, 2026

The most common question that walks into a Medicare agent's office isn't about premiums or enrollment periods. It's some version of "will my plan pay for this?" And more often than not, "this" is acupuncture, chiropractic care, medical marijuana, a concierge doctor membership, or a supplement regimen their neighbor swears by.

Agents who handle these questions well build trust in 90 seconds. Agents who fumble them lose the sale and the referral within a week. The pattern is consistent: the question is rarely about coverage. It's about whether the senior can trust this agent with the rest of their healthcare planning.

Why This Question Is Really a Trust Test

A senior asking about acupuncture coverage is doing something specific: testing whether the agent will give a straight answer, hedge with "check your plan," or oversell. Agents who dig into what clients actually need before recommending a plan recognize this pattern immediately. The alternative-treatment question is the client's way of gauging competence before trusting you with bigger decisions.

The agents who consistently win these conversations share a trait: they give the exact rule first, then explain the exceptions. No hedging, no "it depends" as a first response, no redirecting to member services. The specifics are what signal expertise.

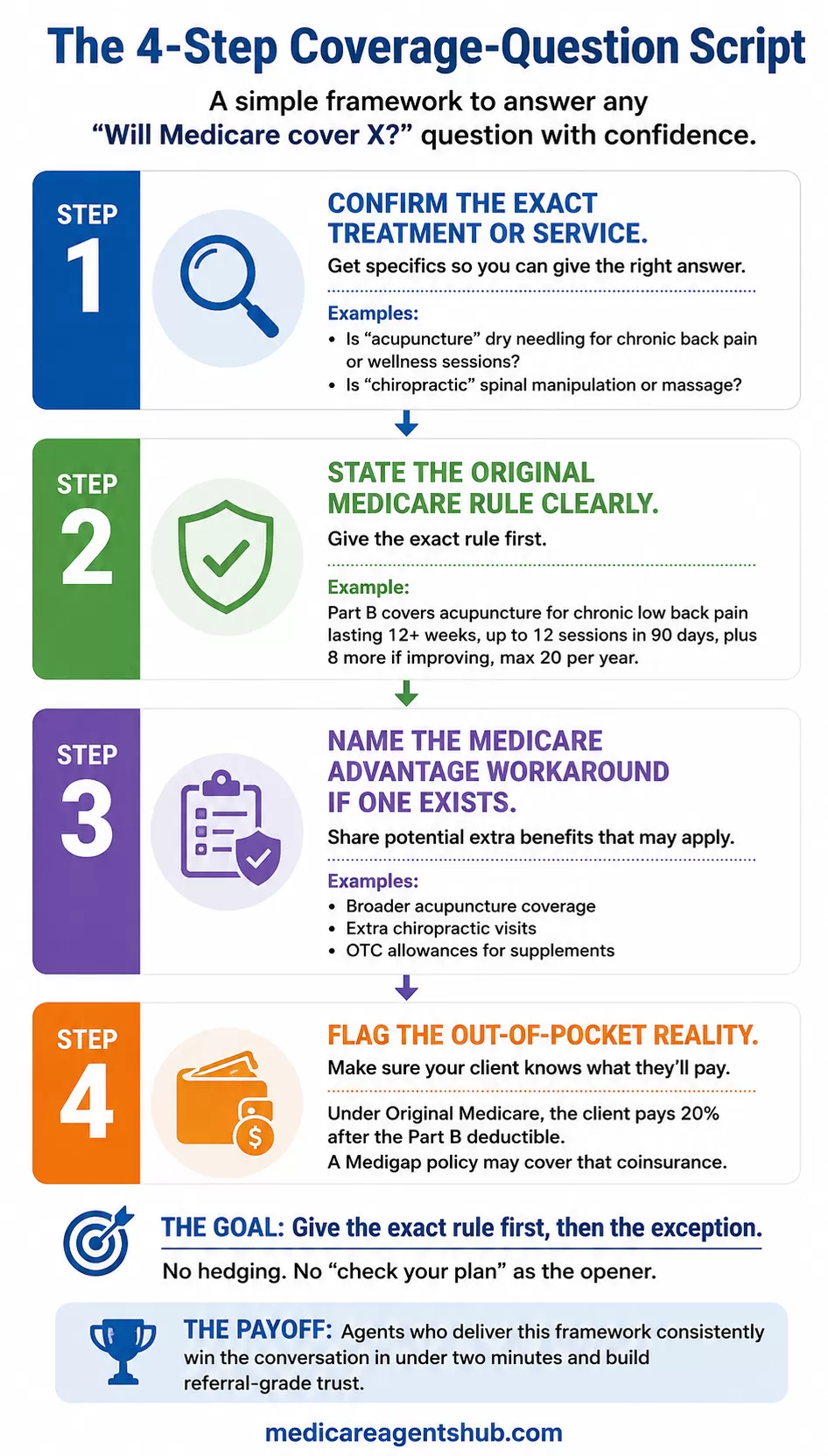

The Four-Step Script That Works Every Time

Across hundreds of answers, the strongest responses follow the same structure, whether the question is about acupuncture, chiropractic care, or anything else. Agents who understand this framework can handle any "will Medicare cover X" question without scrambling.

- Step 1: Confirm the exact treatment or service. "Acupuncture" could mean dry needling for chronic back pain or wellness sessions for stress. "Chiropractic" could mean spinal manipulation or massage therapy. The specifics matter because Medicare draws sharp lines between what it covers and what it doesn't.

- Step 2: State the Original Medicare rule clearly. Not "it depends on your plan." The actual rule. Medicare Part B covers acupuncture for chronic low back pain lasting 12 weeks or longer, up to 12 sessions in 90 days with 8 more if you're improving, for a maximum of 20 per year. That's the kind of answer that makes a client lean forward.

- Step 3: Name the Medicare Advantage workaround if one exists. Many MA plans offer broader acupuncture coverage, additional chiropractic visits, or OTC allowances that can apply to supplements. This is where agents add value beyond what a Google search provides.

- Step 4: Flag the out-of-pocket reality. Under Original Medicare, the client pays 20% after the Part B deductible. With a Medigap policy, that coinsurance may be covered. With an MA plan, there's typically a copay. Giving the cost picture upfront prevents the callback complaint two months later.

Skip any step and the client knows you're winging it. Hit all four and you've just demonstrated more knowledge than most agents they've talked to.

Acupuncture: The Question You'll Get Weekly

Acupuncture questions come up constantly because Part B does cover it, but only under narrow conditions that most seniors don't understand. The agents who handle this well have the specifics memorized.

Medicare Part B covers acupuncture only for chronic lower back pain that has lasted 12 weeks or longer, with no known systemic cause (not related to cancer, surgery, pregnancy, or infection). Coverage includes up to 12 sessions in 90 days, with an additional 8 sessions if the patient is showing improvement, for a maximum of 20 treatments per year. This includes dry needling performed as part of acupuncture treatment. The acupuncture must be provided by a qualified practitioner (MD, DO, NP, PA, or someone under their supervision), and after the Part B deductible, the patient pays 20% coinsurance.

My doctor wants me to try acupuncture for my back pain. Will Medicare cover any of this?

Yes — but only in a very specific situation, and this is where people get tripped up.Original Medicare (Part B) only covers acupuncture for chronic low back pain, and it has to meet all of these criteria:

• The pain has lasted 12 weeks or longer

• It’s not associated with surgery, pregnancy, infection, or cancer

• The acupuncture is provided by a qualified practitioner (MD, DO, NP, PA, or an auxiliary provider under their supervision)

If you qualify, Medicare will cover:

• Up to 12 sessions in 90 days

• An additional 8 sessions if you’re improving - 20 visits max per year

What Medicare does not cover:

• Acupuncture for neck pain, migraines, arthritis, sciatica, or general pain

• “Wellness” or maintenance acupuncture

• Most stand-alone acupuncture clinics unless they meet Medicare’s provider rules

Also important: Medicare Advantage plans may offer broader acupuncture benefits, sometimes covering more conditions or visits than Original Medicare.

Bottom line:

If this is chronic low back pain, there’s a good chance some of it is covered. If it’s for anything else, you should assume Medicare won’t pay unless you’re on a Medicare Advantage plan with extra benefits.

The critical point agents emphasize: Medicare will not cover acupuncture for neck pain, migraines, arthritis, sciatica, or general wellness. That's where the conversation shifts to Medicare Advantage plans, which may offer broader coverage for additional conditions. As one agent in Ohio noted, some MA plans cover acupuncture for migraines, neck pain, and arthritis beyond what Original Medicare allows. The agents who know which plans in their county offer expanded acupuncture benefits are the ones who convert these conversations into enrollments.

Does Medicare Advantage cover acupuncture or alternative therapies in some plans?

Yes, some Medicare Advantage plans cover acupuncture. They can do it in various forms. It can be that they provide for the acupuncture alone including routine visits. The plan may require a provider authorization. In some cases, they will combine it with chiropractic services. And in others, they can even put monies on debit (flex) cards to allow for use at an acupuncture office.Chiropractic: Know the Exact Wording

Chiropractic coverage trips up agents because the answer sounds simple but the details are very specific. The exact wording matters: coverage is limited to manual manipulation to correct a subluxation of the spine. Every plan phrases it slightly differently, but they all include this core terminology. Agents who can recite it from memory signal expertise immediately.

That's the whole Part B benefit. Manual spinal manipulation to correct a vertebral subluxation, and nothing else. Not X-rays. Not massage therapy. Not maintenance adjustments. Not heat therapy. Not exams ordered by the chiropractor. When agents rattle off this list of what's excluded, it demonstrates the kind of precision that builds confidence.

Does Medicare cover chiropractic appointments?

Yes, Medicare (Part B) covers chiropractic care, but only for spinal manipulation (adjustment) to correct a subluxation (misaligned bone in your spine), not for general back pain, exams, X-rays, or maintenance therapy. You pay 20% coinsurance after your deductible, and the chiropractor must be enrolled with Medicare; other services (massage, acupuncture, extremities) and tests are usually not covered, though Medicare Advantage plans might offer moreThe maintenance cutoff is where most clients get confused. Medicare covers chiropractic when there's a specific spinal issue expected to improve, not for long-term upkeep. Once the patient is past the acute phase and visits are mainly about staying comfortable, preventing flare-ups, or routine maintenance, Medicare stops paying. The distinction between "fixing a problem" and "ongoing wellness" is the single most important thing to communicate clearly.

The MA plan angle matters here too. Many Medicare Advantage plans offer 12 to 24 chiropractic visits per year for routine care, not just subluxation. But agents report that converting this into an enrollment conversation requires a specific step: confirming the client's chiropractor is in-network with the plan. Multiple agents flagged that many chiropractors don't accept Medicare at all, so recommending a plan based on chiropractic benefits without checking the provider directory is a mistake that costs credibility.

My dad’s back pain is getting worse. Can Medicare cover ongoing chiropractic care, or is it just short-term treatment?

Medicare only covers chiropractic adjustments when they’re treating a specific spinal problem that’s expected to improve. Medicare Part B only covers manual adjustments when it’s medically necessary. The patient typically pays 20% after the Part B deductible. Services like routine maintenance adjustments, X-rays ordered by the chiropractor, massage, and other therapies are not covered under Original Medicare. Once it becomes routine maintenance, Medicare stops paying.Some Medicare Advantage plans offer additional chiropractic benefits, often including a set number of visits per year with a copay.

The Marijuana Question: Federal vs. State in 30 Seconds

This is the question where agents most often lose composure, and it shouldn't be. The answer is straightforward, and the best agents deliver it with empathy rather than a flat "no."

Medicare does not cover medical marijuana for any condition, regardless of state legality. Medicare is a federal program, and marijuana remains classified as a Schedule I controlled substance under federal law. That's the core answer, and it should come out first. Even with ongoing reclassification discussions at the federal level and some MA plans offering hemp-derived products through SSBCI benefits, plant-based medical marijuana itself remains uncovered by Medicare.

Does Medicare cover medical marijuana if it's prescribed for chronic pain or cancer?

No, Medicare does not cover medical marijuana for chronic pain, cancer, or any other condition, regardless of state legality. Medicare will not pay for medical cannabis products, including flower, oils, or edibles.However, There are some exceptions for FDA approved cannabinoid-based drugs. Examples include Epidiolex (for specific epilepsy types), Dronabinol (Marinol) (for cancer-related nausea or AIDS-related weight loss), Syndros (dronabinol solution) and Cesamet (nabilone).

The three FDA-approved exceptions are where agents separate themselves from a Google result. Epidiolex (for specific epilepsy types), Dronabinol/Marinol (for cancer-related nausea or AIDS-related weight loss), and Cesamet/nabilone are FDA-approved cannabinoid-based medications that can be covered by Medicare Part D plans if they're on the plan's formulary. Knowing these exceptions by name turns a dead-end answer into a useful one.

The trickiest part of this conversation isn't the coverage question. It's the client's frustration. Seniors with state medical marijuana cards often feel like the system is contradicting itself. The framing that works: if a synthetic cannabinoid becomes an FDA-approved medication, it can be covered through Part B or Part D. Many of the approved options target nausea and vomiting from cancer treatment or chronic pain management. That kind of explanation acknowledges the gap between state and federal law without getting political.

The Concierge Medicine Pitch: Two Separate Lanes

Concierge medicine questions are increasing as more primary care practices adopt the model. The challenge for agents is that many seniors hear "concierge" and assume it replaces their Medicare coverage, which creates confusion and sometimes panic.

I'm considering concierge medicine but already have Medicare. How would these work together?

Here’s the clearest way to think about it: concierge medicine and Medicare can work together, but they operate in completely separate lanes. Medicare continues to cover Medicare‑approved services, while the concierge membership fee is always 100% out‑of‑pocket. The key is understanding what your concierge doctor bills to Medicare versus what your membership fee actually buys you.The key framing agents use: concierge medicine is a membership arrangement with a primary care physician, and Medicare is your insurance coverage. They operate in separate lanes. The membership fee (typically $100 to $300 per month, though some practices charge $2,000 to $5,000 annually) is always out of pocket. Medicare will never reimburse it. But Medicare continues to cover everything it normally covers: specialist visits, lab work, hospital stays, imaging, and procedures referred by the concierge doctor.

The practical distinction agents need to explain: some concierge doctors still accept Medicare and bill it for covered services while charging the membership fee separately for enhanced access. Others have opted out of Medicare entirely, meaning the patient pays the membership fee and pays full price for every visit. This is the question agents should coach clients to ask the concierge practice before signing up: "Do you still accept and bill Medicare for covered services, or are you fully opted out?"

Several agents noted that concierge medicine tends to work better with Original Medicare plus a Medigap supplement than with Medicare Advantage, because MA plans use networks and many concierge doctors are out-of-network or non-participating. Several agents recommend that clients considering concierge pair it with a High Deductible Plan G to keep premiums manageable while maintaining the broadest provider access.

Supplements, Herbs, and Homeopathy: The Flat 'No' With a Redirect

The supplements question gets the shortest answer from most agents: no, Medicare does not cover vitamins, dietary supplements, herbal remedies, homeopathic treatments, or naturopathic care. These are not FDA-approved treatments and fall outside Medicare's definition of "medically necessary."

Does Medicare cover supplements, herbs, homeopathy or other natural / alternative-medicine treatments?

Original Medicare does not cover supplements, herbs, homeopathy, or most alternative treatments.Not covered:

• Vitamins and dietary supplements

• Herbal remedies

• Homeopathic treatments

• Naturopathic care

Limited exceptions:

• Chiropractic spinal manipulation

• Acupuncture for chronic low back pain only

Part D covers FDA-approved prescription drugs, not over-the-counter or natural products.

Some Medicare Advantage plans offer small OTC allowances, but coverage is limited and varies by plan.

But the agents who work effectively with seniors managing chronic conditions don't just stop at "no." They redirect to what is available. Many Medicare Advantage plans include OTC (over-the-counter) benefit cards that can be used to purchase vitamins, supplements, and certain health products at approved retailers. The allowance varies by plan and region, but it's a real benefit that agents can point to. As agents across multiple states pointed out, many MA plans include OTC benefits that can help cover the cost of vitamins, supplements, and similar health products at approved retailers.

The redirect is what makes this answer useful rather than just correct. A client asking about turmeric supplements for joint inflammation doesn't want a lecture on FDA approval. They want to know if there's any way to offset the cost. An OTC card on the right MA plan might cover $50 to $150 per quarter in supplement purchases, and knowing that turns a dead-end into a plan recommendation.

When a Senior Gets Political: The 'Should Medicare Cover More?' Trap

Seniors sometimes shift from a coverage question into a policy question: "Shouldn't Medicare cover more of this stuff?" The answers from agents reveal a pattern worth studying: the best agents don't take the bait.

Shouldn't Medicare expand to cover more alternative treatments that actually help seniors?

That’s a question a lot of people are asking right now.Medicare’s coverage decisions are usually based on whether a treatment is considered “medically necessary” and supported by strong clinical evidence. Some alternative treatments don’t get covered because Medicare requires large-scale studies showing safety and effectiveness.

That said, Medicare has expanded certain benefits over time — for example, it now covers some acupuncture for chronic low back pain and certain preventive services that weren’t included years ago.

If there’s a specific treatment you’re wondering about, I can help you check whether Medicare covers it, whether a Medicare Advantage plan offers it as an extra benefit, or what other options might help reduce the cost.

What treatment were you thinking about?

That kind of response does three things: it explains why the limitation exists without defending it, it acknowledges that coverage does evolve, and it pivots back to what the agent can actually help with. Medicare has already been moving in this direction: acupuncture for chronic low back pain was added in 2020, and many MA plans now include fitness and wellness benefits that didn't exist five years ago. Multiple agents mentioned that changes to Original Medicare require an act of Congress, and directing the client to contact their representative is both accurate and a clean exit from the political conversation. The agents who build lasting books of business are the ones who keep these conversations focused on what they can control.

When to Admit You Don't Know

Every topic above has a clean answer. But clients don't always ask clean questions. The rare-disease specialist plus obscure biologic question, the experimental treatment their oncologist mentioned, the clinical trial their daughter read about online: these are the questions where even experienced agents hit the edge of their knowledge.

The best response, drawn from how top agents handle these situations: "Let me check the formulary and call you back today." That sentence does more for trust than faking an answer. It tells the client you take the question seriously enough to research it, and the "today" part signals urgency. Agents who promise a callback and deliver within hours report that these interactions often produce the strongest client loyalty, because the client remembers that you didn't guess.

This is also where the follow-up discipline separates good agents from great ones. The callback with a researched answer is a higher-trust moment than getting it right on the spot, because it demonstrates process and reliability rather than just memory.

Putting It Together: Building a Coverage-Question Playbook

The agents whose answers stood out across all nine questions shared a common approach. They didn't treat "does Medicare cover X" as a yes-or-no question. They treated it as a four-part conversation: the Original Medicare rule, the MA plan alternative, the cost reality, and the next step. They had the specific numbers memorized for the treatments that come up weekly (acupuncture visit limits, chiropractic subluxation language, marijuana's Schedule I status). And they knew when to stop talking and go research.

Can a Medicare broker help us find a plan that includes broader chiropractic coverage?

Yes. A Medicare broker can compare plans in your area and identify which Medicare Advantage plans offer additional chiropractic benefits beyond what Original Medicare covers. Original Medicare generally covers only spinal manipulation to correct a spinal subluxation, not routine chiropractic care.Many Medicare Advantage plans include extra visits, wellness services, or broader chiropractic coverage, but the benefits vary by plan and network. A broker can help you compare those benefits alongside your doctors, medications, and overall costs.

If you're building your own reference sheet for these questions, start with the five covered in this article. They account for the vast majority of alternative-treatment questions seniors ask. Get the specifics down cold, practice delivering the four-step framework until it's second nature, and you'll handle each one in under two minutes while building the kind of credibility that turns a coverage question into a client relationship.

Coverage details current as of June 2026. Always verify with specific plan documents or Medicare.gov, as Medicare Advantage benefits vary by plan and region.