Medicare in 2025: Must-Know Changes and Challenges for New and Current Enrollees

-

Last Updated July 22, 2026

Written by Douglas Carney

Medicare Broker Licensed in FL, GA, NC, OK & TX

In 2025, Medicare is undergoing transformative changes that are sparking conversations among those aging into the program and current enrollees alike. From groundbreaking cost-saving measures to concerns about privatization, these shifts are reshaping how beneficiaries plan for healthcare. As someone passionate about helping others navigate Medicare, I’ve compiled the top trending topics you need to know, drawing from recent updates and discussions, with insights tailored for both new and existing enrollees.

1. The Game-Changing $2,000 Cap on Part D Drug Costs

Starting January 1, 2025, the Inflation Reduction Act introduces a $2,000 annual out-of-pocket cap on prescription drug costs for Medicare Part D plans, including those bundled with Medicare Advantage. This reform eliminates the infamous "donut hole," where beneficiaries once faced steep costs. An estimated 3.2 million enrollees could save an average of $1,500, with some, especially those on pricey medications like cancer drugs, saving up to $3,000 or more.

For You: If you’re aging into Medicare, this cap makes Part D plans more predictable, especially if you manage chronic conditions requiring costly drugs. Current enrollees with high drug expenses should review their plans during open enrollment (October 15–December 7, 2024) to ensure their medications are covered under the cap, as it only applies to drugs on a plan’s formulary.

However, watch out: insurers may raise premiums or tweak formularies to offset these costs, so compare plans carefully.

For Medicare Part D, why would someone pick a plan with a high total cost?

A senior might pick a higher-cost Medicare Part D plan for better coverage of costly or specialty medications, lower copays or coinsurance, access to preferred pharmacies, or a wider drug formulary that includes all their needed prescriptions, ultimately saving on out-of-pocket costs for frequent or expensive drugs.2. Smoothing Costs with the Medicare Prescription Payment Plan

A new voluntary Medicare Prescription Payment Plan, launching January 1, 2025, lets Part D enrollees spread out-of-pocket drug costs over the year. This is a lifeline for those hit with high early-year expenses or short-term costly prescriptions.

For You: New enrollees can budget more effectively, avoiding the shock of large upfront costs. If you’re already on Medicare, this plan could ease the burden of variable drug expenses, though it doesn’t lower total costs—just distributes them. Be aware that opting in may feel complex, and awareness of this option is still growing.

3. Medicare Advantage: Fewer Plans, Shifting Networks

In 2025, Medicare Advantage (MA) plans are shrinking, with an average of 34 plans per county (down from 43 in 2024). Some health systems, like Essentia Health and Sanford Health, are dropping MA plans such as Humana and UnitedHealthcare due to prior authorization hurdles and high denial rates. Plus, some MA plans are cutting supplemental benefits—like gym memberships or over-the-counter medication allowances—to manage costs from the Part D cap and reduced government payments.

For You: If you’re new to Medicare, choosing between Original Medicare and MA is trickier with fewer plans and changing provider networks. Current MA enrollees, especially the 1.4 million in terminated plans, should check their Annual Notice of Change (ANOC) to confirm in-network doctors, hospitals, and benefits like dental or vision. Don’t get caught off guard—review your options now.

So with all these 2025 Medicare changes, should I be switching plans or staying put?

As a Medicare-specialized health insurance broker, I’m here to guide you through the 2025 Medicare changes and help you decide whether to switch plans or stay put with confidence. With the new $2,000 Part D drug cost cap, shrinking Medicare Advantage (MA) plan options, and rising Part B premiums ($185/month).If your current MA or Part D plan still covers your doctors, drugs, and budget—great, stay put! But if your plan’s network, benefits (like dental or vision), or costs are changing, or you’re in one of the 1.4 million terminated MA plans. I always recommend an annual policy review to ensure you’re all set. As you age so does your coverage needs.

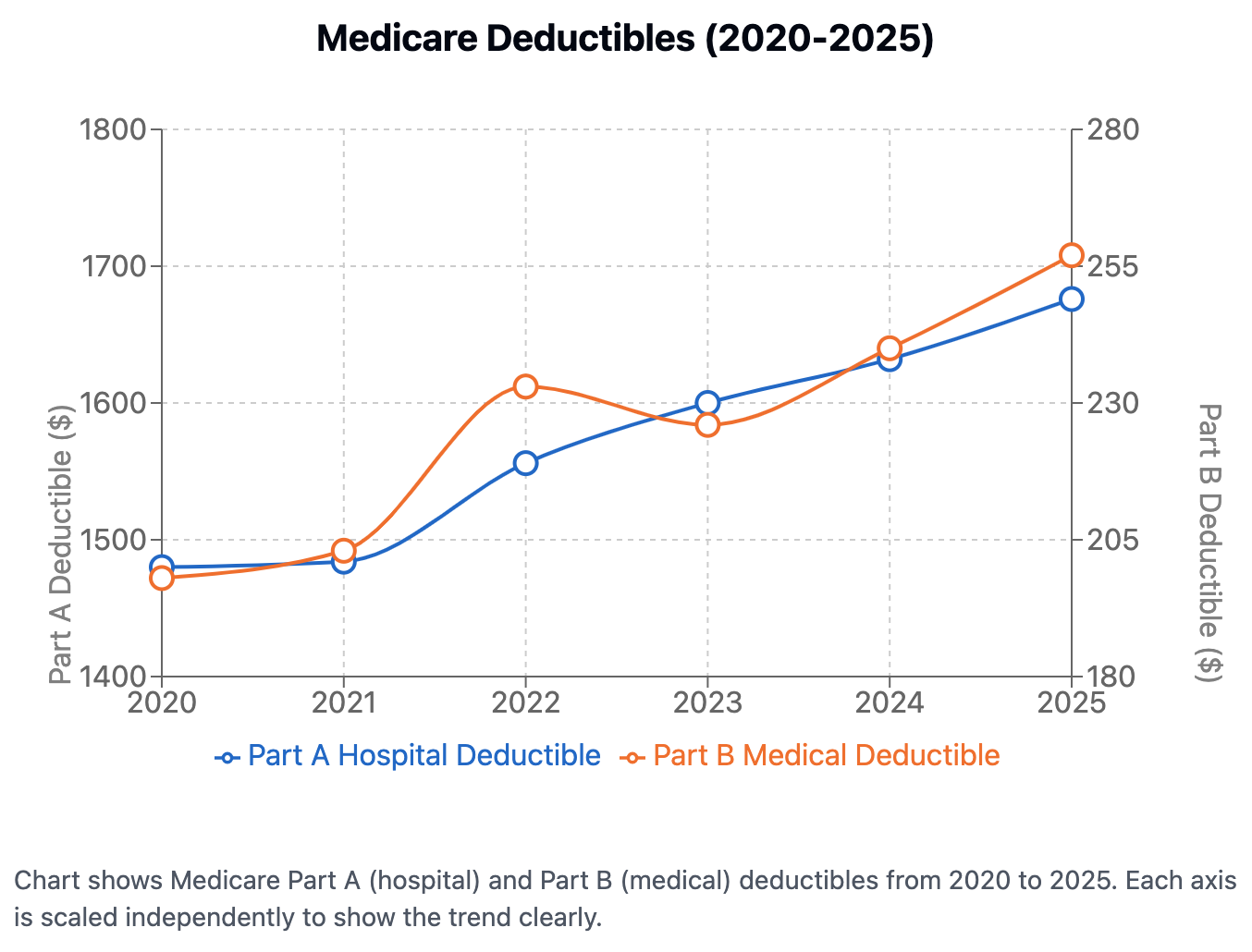

4. Rising Premiums and Cost-Sharing for Parts A, B, and D

Medicare costs are climbing in 2025. Part B premiums are up to $185/month (a $10.30 increase), with deductibles rising to $257 (up $17). Part A hospital deductibles are $1,676 (up $44), and Part D deductibles can hit $590 (up from $545). High earners (above $106,000/year) face steeper income-related adjustments (IRMAA), impacting about 8% of beneficiaries.

For You: If you’re aging into Medicare, factor these costs into retirement planning, especially if you don’t qualify for premium-free Part A (requiring 40 quarters of work). Current enrollees on fixed incomes may feel the pinch, though the 2.5% Social Security COLA for 2025 offsets the Part B hike for most. High-income retirees should review IRMAA thresholds to manage expenses.

5. Expanded Benefits and Support Programs

Medicare is broadening its reach in 2025, covering more mental health services, cardiovascular risk assessments, and dental care for specific treatments. The Guiding an Improved Dementia Experience (GUIDE) program is quadrupling, offering caregiver support, 24/7 helplines, and respite care. Caregiver training and hospice respite care are also newly covered. The Extra Help program for low-income beneficiaries is easier to access, covering most drug costs for those below 150% of the federal poverty level.

For You: New enrollees with chronic conditions or caregiving duties can benefit from these enhancements, especially in MA plans with supplemental coverage. Current beneficiaries should explore Extra Help (e.g., $4.90 for generics, $12.15 for brand-name drugs) and GUIDE for dementia care, though low awareness may mean you need to dig for details.

6. Privatization Fears: The Project 2025 Debate

Project 2025, a Heritage Foundation policy agenda, proposes making Medicare Advantage the default enrollment option, fueling fears of Medicare privatization. Critics warn this could limit provider choices, increase prior authorization denials, and add $2 trillion in wasteful spending over a decade if MA enrollment hits 75%. Social media is buzzing with concerns about higher drug prices and reduced care access.

For You: If you’re new to Medicare, weigh MA’s restrictions (like limited networks) against Original Medicare’s flexibility. Current MA enrollees might reconsider plans during open enrollment, fearing future shifts that could curb Traditional Medicare access. These proposals aren’t policy yet, but they’re worth watching.

7. The Long-Term Care Misconception

A recent poll revealed that 49% of adults aged 50–64 and 66% of those 65+ wrongly believe Medicare covers long-term nursing home care—it doesn’t. This misconception is driving calls for better education and planning.

For You: If you’re aging into Medicare, start exploring long-term care options like Medicaid or private insurance now. Current beneficiaries frustrated by this gap should look into alternatives, as social media reflects growing discontent with Medicare’s limitations.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

To help you plan for Medicare costs while preparing for potential long-term custodial care in a nursing home or assisted living. There are smart steps to take for a secure future. Medicare doesn’t cover long-term custodial care, but you can plan by exploring Medicaid, which often covers these costs for low-income individuals—check eligibility at Medicaid.gov and consider spending down assets strategically. Private long-term care insurance, purchased early, can also offset expenses, with policies tailored to your needs. Budget for Medicare Parts A, B, and D premiums and deductibles ($185/month, $257, and up to $590 in 2025, respectively), and consider a Medigap plan to cap out-of-pocket costs.A Critical Take: Opportunities and Risks

The $2,000 Part D cap and payment plan are hailed as cost-savers, but they may trigger higher premiums or reduced MA benefits as insurers adapt. The push toward MA under proposals like Project 2025 raises valid privatization concerns, though evidence on MA’s quality versus Traditional Medicare is mixed—some studies show similar outcomes, others highlight MA’s restrictive practices. The long-term care misconception underscores Medicare’s complexity and the risk of misinformation, which could leave beneficiaries unprepared.

As we navigate these changes, my advice is clear: whether you’re new to Medicare or a seasoned enrollee, stay informed, compare plans diligently during open enrollment, and don’t hesitate to seek help from Medicare.gov or a trusted advisor. For a deeper dive into what changed this year, see our breakdown of the big changes coming to Medicare in 2025, or jump ahead to everything that changed in Medicare for 2026. The landscape is shifting, but with the right knowledge, you can make choices that protect your health and wallet in 2025.

About the Author: Douglas Carney is a Medicare Broker Licensed in FL, GA, NC, OK and TX.